The $20K leak in a tidy Google salary

The Situation

Daniela is a 43-year-old staff software engineer at Google in Mountain View. She and her husband both work, they have two kids in elementary school, and by every reasonable measure they were doing the right things. She maxed her 401(k) every year, contributed to the kids' 529 plans, held a healthy cash cushion in a high-yield savings account, and let her GSUs vest and accumulate. Her taxes were filed cleanly and on time by a good CPA.

What Daniela had was a setup that looked simple and responsible from the outside — and it was. Nothing was broken. But a combined household income north of $650K, sitting in California, quietly changes the math on almost every one of those decisions. She assumed that because everything was tidy, everything was optimized. Those are not the same thing.

The Gap We Found

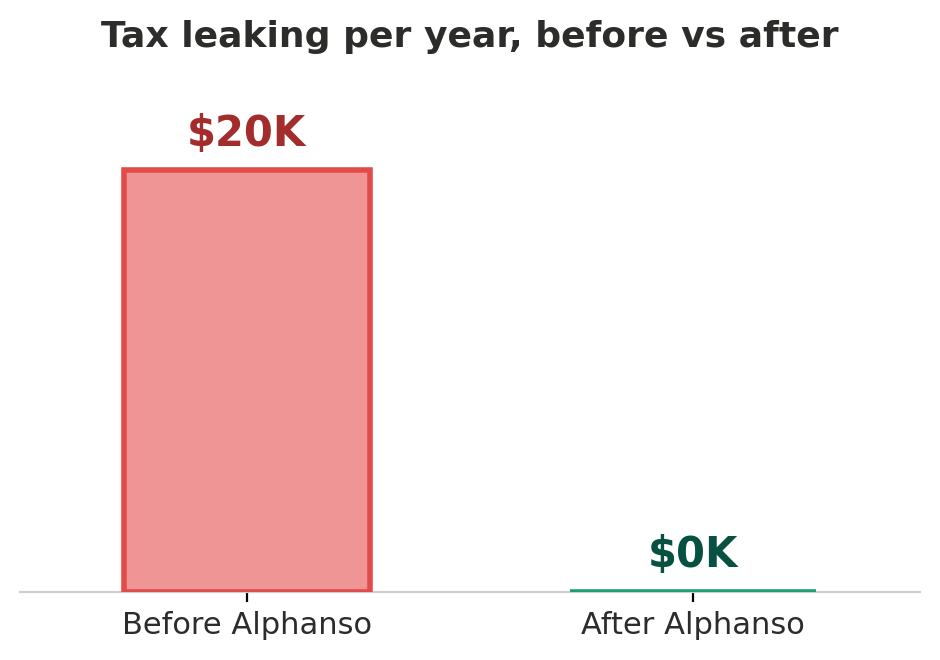

When we mapped Daniela's full picture side by side — payroll, portfolio, and tax return in one view — the leak became obvious. Her CPA filed an excellent return, but a CPA reports the past; nobody was steering decisions before the year closed. She had roughly $280K sitting in a HYSA earning interest taxed at her top federal bracket plus California's 9.3%, she was above the income limit for a Roth but had never been shown the backdoor, her taxable brokerage held index funds with no tax-loss harvesting, and her vested GSUs were being sold in whatever order her broker defaulted to. Individually, small. Together, about $20K a year walking out the door.

What We Did

First, we put her idle cash to work more efficiently. We moved the bulk of the HYSA balance she didn't need for near-term goals into a California municipal bond ladder, where the income is exempt from both federal and California tax — an effective after-tax yield materially higher than the fully-taxed HYSA interest she'd been earning.

Second, we opened the door she didn't know existed. As a high earner she's phased out of direct Roth contributions, so we set up a backdoor Roth for her and her husband — non-deductible contributions converted to Roth — giving them a new stream of tax-free growth for life. Alongside that, we replaced her plain index funds with a direct-indexing portfolio that harvests losses automatically throughout the year, generating deductions that offset gains from her GSU sales.

Third, we fixed the GSU mechanics. Going forward, our AI agents flag each vesting event in advance and identify specific lots to sell, so she diversifies out of concentrated GOOGL using the highest-cost-basis shares first — minimizing the capital gains on every sale instead of leaving it to broker default.

The Result

- Roughly $20,000 in recurring annual tax savings — without changing a single thing about how Daniela lives or works.

- A backdoor Roth for both spouses, adding a permanent tax-free growth engine they didn't know they qualified for.

- Idle cash converted from fully-taxed HYSA interest to tax-exempt municipal income at a higher after-tax yield.

- For the first time, one team looking at her payroll, portfolio, and taxes together — and steering decisions before year-end, not reporting them after.

Why This Worked

None of Daniela's advisors were doing a bad job. Her CPA filed a clean return; her broker executed her trades. The problem was that no one was looking at everything at once. Alphanso's flat-fee, fiduciary model means we're paid to see the whole picture and act on it — not to sell a product or bill on assets. When the tax return, the payroll, and the portfolio finally sit on the same desk, the $20K that was quietly leaking becomes $20K she keeps. If your setup feels simple and tidy but you've never had anyone check whether it's actually optimized, we'd love to take a look — request a callback.

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect