A Snowflake PM watched her RSUs jump 36% overnight

The Situation

Soo-Jin Park is a Level 6 Product Manager at Snowflake in San Francisco. She’s 35, married, and she and her husband — a senior engineer at a mid-stage startup — bring in a combined household income of around $520,000. Soo-Jin’s compensation is roughly $185,000 in base salary plus $240,000 in RSUs vesting quarterly. She maxes out her 401(k), contributes to her ESPP, and keeps a healthy emergency fund. By most measures, she was doing everything right.

On May 28, 2026, Snowflake reported blowout earnings — revenue up 33%, a $6 billion AWS partnership, and AI products driving record growth. The stock surged 36% in a single day. Soo-Jin’s quarterly RSU tranche, valued at roughly $60,000 on the day it vested, was suddenly worth over $82,000 on paper. She felt euphoric. Then she opened a spreadsheet and felt something else entirely: confusion.

The Gap We Found

Soo-Jin had a good CPA who filed her taxes every April. She had a brokerage account at Fidelity where her RSUs landed. What she didn’t have was anyone connecting the two. Her employer withheld 22% on each RSU vest — the standard supplemental rate. But her actual combined federal and California state tax rate was closer to 44%. On $240,000 in annual RSU income, that withholding gap added up to roughly $52,800 in taxes she’d owe at filing time — every single year. She’d been paying quarterly estimates to cover it, but the amounts were based on last year’s income and hadn’t been adjusted for the Snowflake stock surge. Nobody was watching the real-time number. And now, with shares worth 36% more than expected, the gap had grown even wider.

What We Did

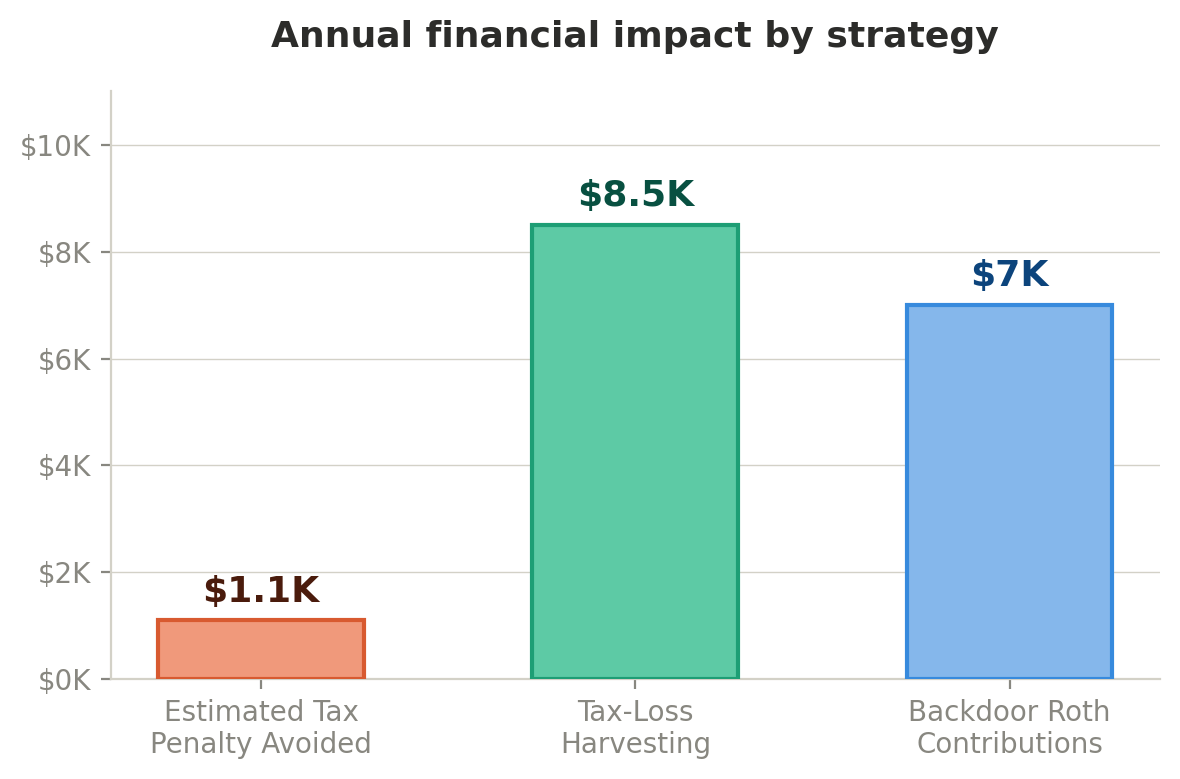

Recalculated estimated taxes in real time. Alphanso’s AI agents pulled Soo-Jin’s payroll data, modeled her updated income trajectory with the SNOW surge priced in, and calculated the exact quarterly estimated payment she needed to make by June 15 to avoid an underpayment penalty. The number came out to $14,200 for Q2 — significantly higher than the $9,800 she’d been planning to send. Without this adjustment, she’d have faced a penalty of roughly $1,100 at filing time, on top of the surprise tax bill.

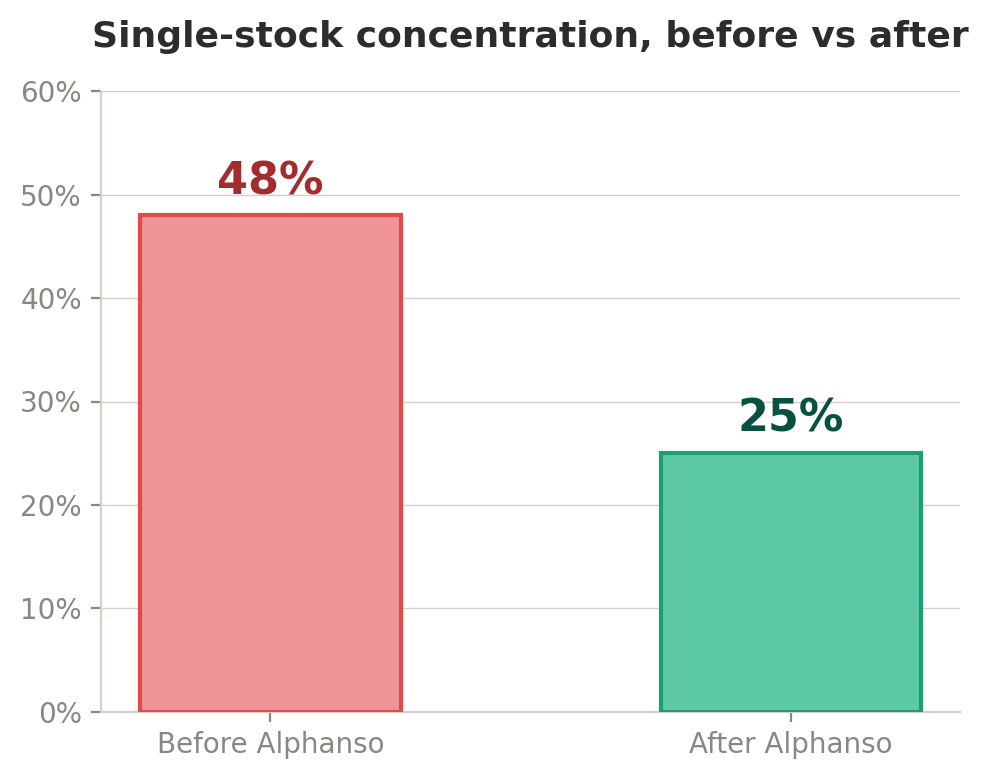

Built a structured RSU selling plan. Instead of letting Soo-Jin’s Snowflake position grow unchecked after the surge, we designed a rule-based selling strategy: sell 70% of each quarterly vest within the first week, hold 30% for potential long-term capital gains treatment if the one-year holding period made sense given her tax bracket. This reduced her single-stock concentration from 48% of liquid net worth to under 25% within two quarters. The proceeds went into a direct-indexing portfolio that generated an additional $8,500 in annual tax-loss harvesting benefits.

Set up a backdoor Roth IRA. Soo-Jin’s income put her well above the Roth IRA contribution limit. Her CPA knew this. Her brokerage knew this. But nobody had walked her through the backdoor Roth conversion — a straightforward two-step process that would give her $7,000 of tax-free growth every year for life. We set it up in one meeting and added it to her annual financial checklist.

The Result

- $14,200 Q2 estimated payment recalculated before the June 15 deadline — avoiding ~$1,100 in underpayment penalties

- Concentration reduced from 48% to under 25% in two quarters through systematic selling

- $8,500/year in tax-loss harvesting from the direct-indexing portfolio funded by diversified RSU proceeds

- Backdoor Roth IRA established — $7,000/year of tax-free growth she’d been leaving on the table

- “For the first time, I didn’t feel anxious after earnings.” — Soo-Jin told her advisor she finally had a plan that updated itself, instead of one she had to panic-build every quarter.

Why This Worked

Soo-Jin’s CPA was competent. Her Fidelity account was fine. What was missing was a single team watching all the pieces — income, taxes, portfolio concentration, retirement contributions — and adjusting the plan when something changed. The 36% Snowflake surge wasn’t a crisis. It was just a data point. But without anyone modeling the downstream effects in real time, it would have become a $15,000+ problem at tax time.

Alphanso’s flat-fee model means Soo-Jin pays $2,400 a year for integrated wealth management — investments, taxes, and planning, coordinated by one team. No AUM percentage. No incentive to gather assets. Just a fiduciary team that recalculates when the numbers change.

If your RSUs just had a big day and you’re not sure what it means for your taxes, your concentration, or your plan — let’s walk through it together.

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect