A Meta manager's 'simple' setup was quietly leaking $20K a year

The Situation

Hana, 43, is an engineering manager at Meta in the Bay Area. She and her husband, also in tech, bring in roughly $680,000 a year between salary and RSUs, and they're raising two kids in the South Bay. By every reasonable measure, Hana had her financial life together. She maxed her 401(k), let Meta sell shares to cover taxes at each vest, kept a healthy cash cushion in a high-yield savings account, and held a tidy brokerage account in low-cost index funds.

Each spring she handed everything to a well-regarded CPA, who filed an accurate return and answered her questions. When she described her finances, the word she used was “simple.” She wasn't chasing exotic strategies, and she liked it that way. So when a friend suggested she get a second look, she almost didn't bother — nothing felt broken.

The Gap We Found

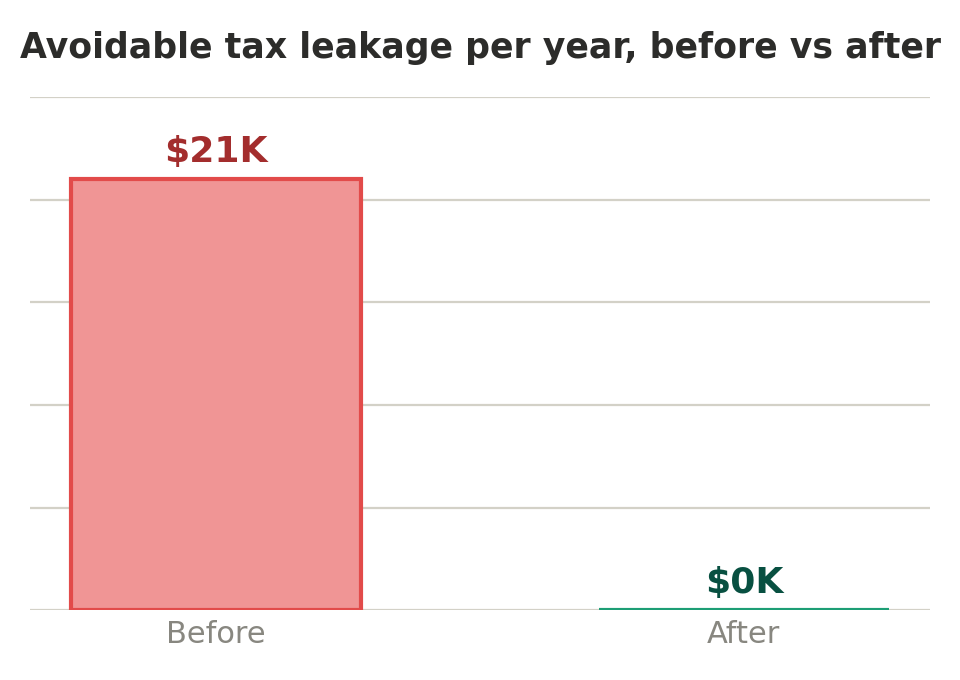

Nothing was broken — but nothing was connected, either. Hana's combined California and federal marginal rate sat near 50%, and not one piece of her setup was arranged with that number in mind. Her CPA filed accurately, but reactively, in April, after every decision had already been made. Her brokerage held plain index funds and a taxable bond fund generating fully taxable interest. Her cash sat in a savings account taxed at her top rate. And her Meta 401(k) plan included an after-tax contribution feature — the door to a mega backdoor Roth — that no one had ever pointed out to her. Each professional was doing their job inside their lane. No one was looking at the whole picture, and the whole picture was leaking about $20,000 a year.

What We Did

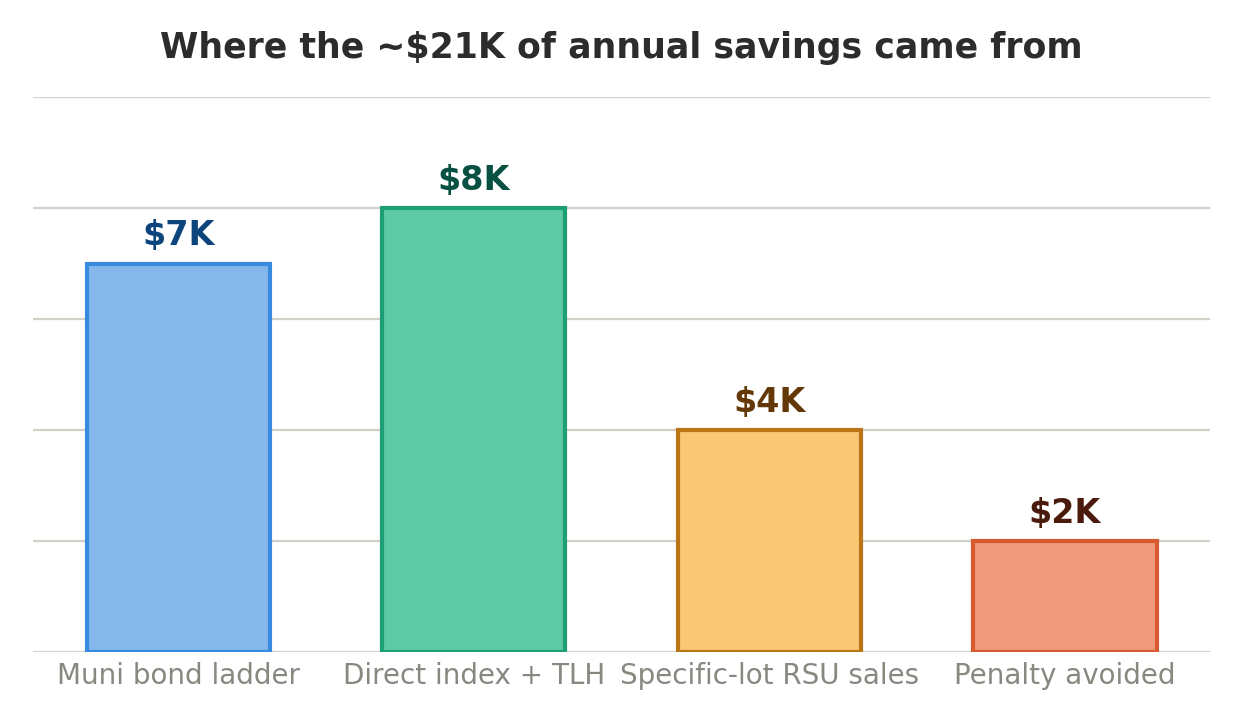

We started where the bleeding was largest. We moved her taxable index funds into a direct-indexing portfolio with automated tax-loss harvesting — it tracks the same market exposure she already wanted, but harvests losses on individual holdings throughout the year. Those losses now offset gains from her RSU sales, so diversifying no longer means handing a chunk to the IRS.

Next, we turned on the mega backdoor Roth inside her Meta 401(k), routing after-tax contributions and converting them so more than $30,000 a year now grows tax-free for life. We replaced the taxable bond fund and her excess savings cash with a California municipal bond ladder — interest that's exempt from both federal and state tax, lifting her effective after-tax yield without adding real risk. We also switched her RSU and ESPP sales to specific-lot identification, so she sells the highest-cost shares first and keeps capital gains down.

Finally, we put her vesting schedule on autopilot. Alphanso's AI agents parse her payroll, compare what's been withheld against what she'll actually owe, and flag the right quarterly estimated payment before each deadline — so a big vest never turns into an April surprise or an underpayment penalty.

The Result

- About $21,000 in tax savings in year one — and recurring every year after.

- More than $30,000 a year now flowing into a Roth that grows tax-free for life.

- A higher after-tax yield on cash and bonds, with no meaningful change in risk.

- One coordinated team — and the relief of knowing nothing is quietly slipping through the cracks.

Why This Worked

Hana's setup wasn't failing because anyone was careless. It was failing because the people advising her could only see their own slice. Alphanso's edge is integration: investments, taxes, and benefits managed as one system, by a fiduciary paid a flat fee rather than a percentage of her assets. That alignment is exactly why we go looking for the quiet $20,000 leaks — there's no incentive not to.

If your financial life feels “simple” but you've never had anyone look at all of it at once, that's usually where the savings hide. Request a callback and we'll take a look.

Disclosure

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect