How we harvested losses on a Meta engineer's RSUs to offset a giant vest

The Situation

Steve is a 35-year-old staff engineer at Meta in the Bay Area. Between his base salary and a vesting schedule that had ballooned with several years of stock refreshers, he was on track to clear north of $650,000 in total compensation for the year — most of it landing in a single, very large RSU vest in the back half of the year.

He was already doing a lot right. He maxed his 401(k), contributed to an HSA, and had a sharp CPA who filed a clean, accurate return every spring. He wasn't reckless; he was busy. What he didn't have was anyone connecting the dots between the taxable event barreling toward him in Q4 and the rest of his financial picture — the brokerage account, the older lots of META he'd been quietly accumulating, and the rocky year the market had handed him along the way.

The Gap We Found

First, we mapped the full year as one tax event instead of two disconnected ones. Our AI agents parsed his payroll and vesting data to project exactly how much of the Q4 vest would be under-withheld — Meta, like most employers, withholds RSUs at a flat 22% supplemental rate, well below his actual marginal bracket — so we knew the size of the bill before the shares vested.

Then we went looking for losses to put against it. Through tax-loss harvesting, we sold the underwater positions in his brokerage account to realize roughly $90,000 in capital losses, immediately reinvesting the proceeds into a comparable (but not identical) index position so he stayed fully invested and never tripped the wash-sale rule. Those harvested losses offset capital gains elsewhere in his portfolio and let him deduct against ordinary income, directly softening the tax owed on the vest.

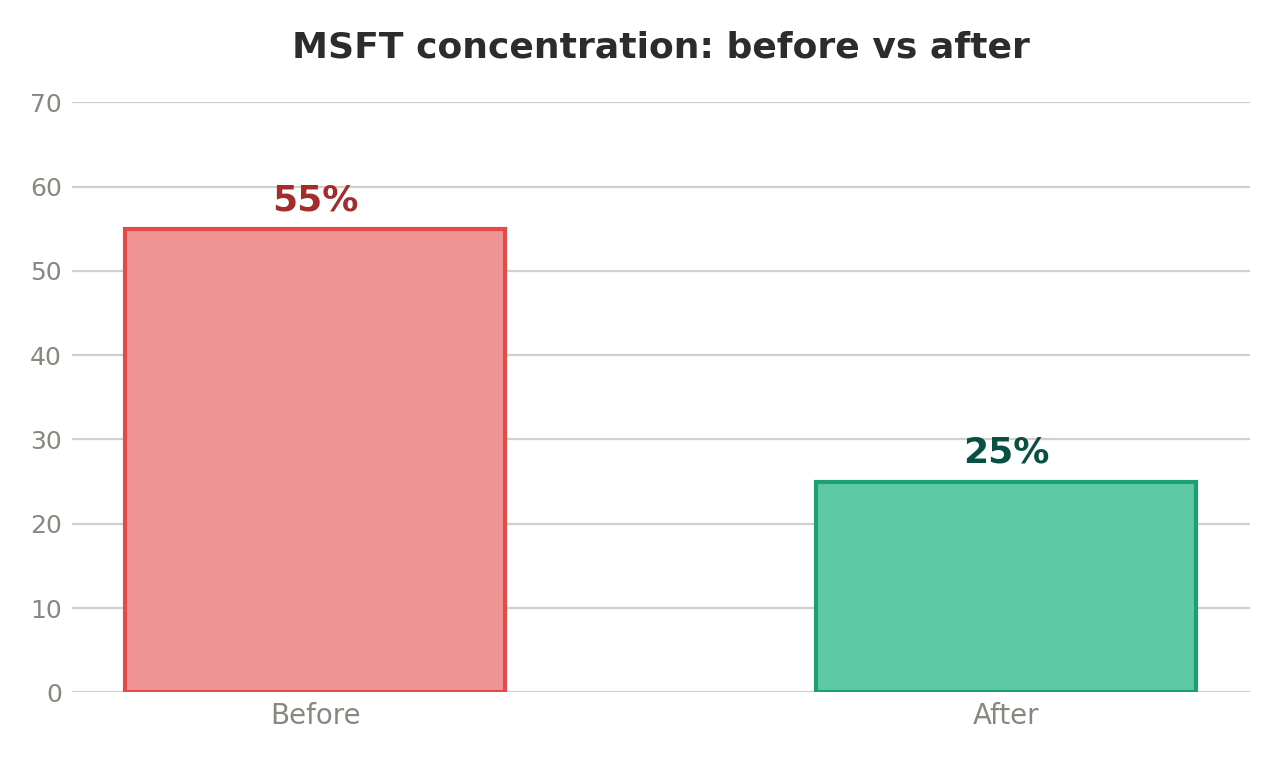

Finally, we used the harvest as the moment to fix the underlying problem: concentration. Rather than rebuilding the same single-stock exposure, we moved his into a direct-indexing portfolio — which holds the individual names of an index in a way that lets us keep harvesting small losses automatically, year after year, while methodically trimming his oversized META position into a diversified mix. The estimated-tax gap our agents had flagged was covered with a right-sized quarterly payment, sent before the deadline, so there was no underpayment penalty waiting in April.

The Result

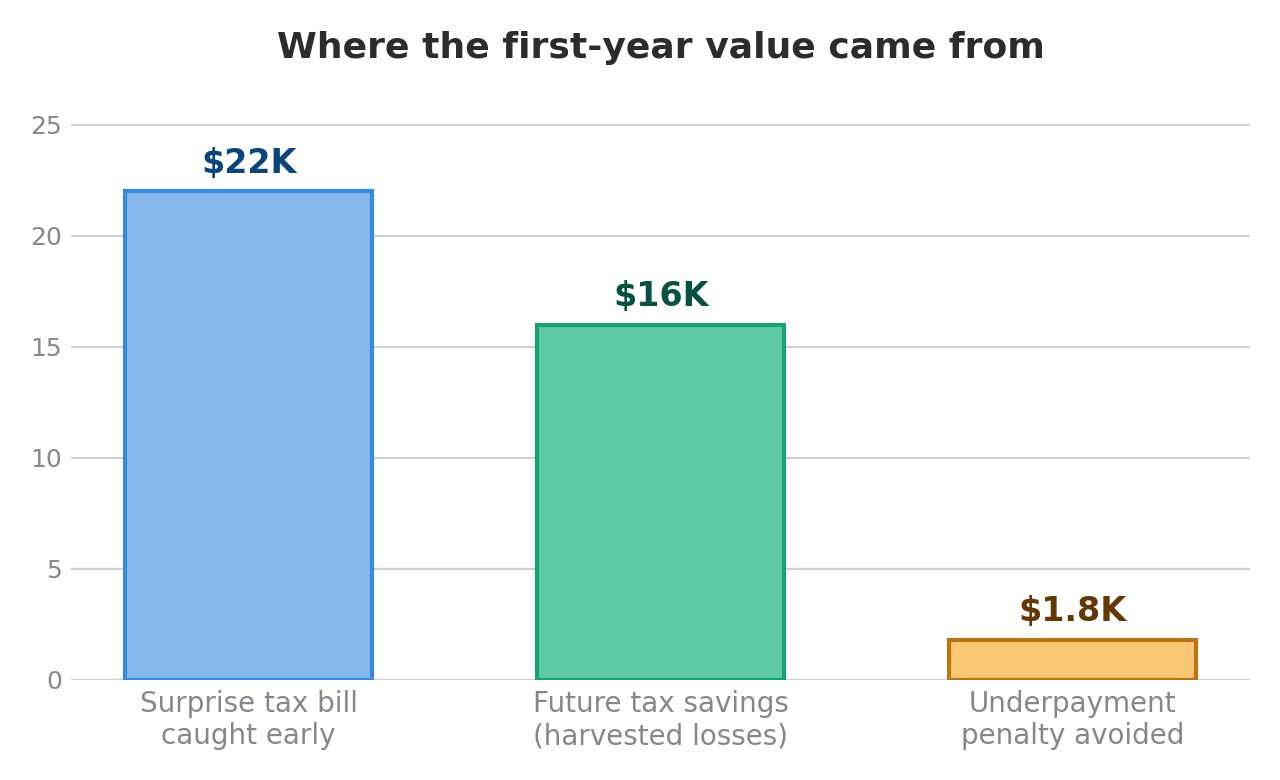

- ~$90,000 in capital losses harvested, offsetting gains and reducing the tax owed on his large RSU vest by roughly $24,000 in year one.

- Concentration cut from over 40% to under 15% of his portfolio in a single stock, without a surprise tax bill to get there.

- Avoided an estimated under-withholding penalty through a proactively calculated quarterly payment.

- A repeatable system that keeps harvesting losses automatically — so the next big vest already has offsets waiting.

Why This Worked

None of this required Steve to earn less, save more, or take on more risk. It worked because one team finally looked at the vest, the brokerage account, and the tax return at the same time — and acted on the connection between them. That's the whole idea behind Alphanso's integrated, flat-fee, fiduciary model: we're not paid on how much you have or which products you buy, so the only thing left to optimize is your actual outcome. If a large vest is coming and you're not sure whether you're leaving money on the table, request a callback — we'll walk through your situation, no pressure.

Disclosures

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

.png)

Schedule demo with our advisors

What to expect