Laid off from Microsoft after 12 years. The 60-day plan that steadied the ship.

The Situation

Yael had been at Microsoft for twelve years. She’d joined as a program manager, worked her way up to principal PM in the Redmond office, and along the way had built the kind of life that felt settled: a house, two kids in middle school, a spouse with a steady income of his own, and a stock account that had quietly grown into the largest number on her balance sheet. She was 45, and she’d never once been between jobs.

Then, in a single Tuesday morning meeting, her role was eliminated. Microsoft handed her a severance package — roughly six months of pay — accelerated a tranche of her unvested RSUs, and gave her a separation date. Yael had done a lot right. She had an emergency fund, she maxed her 401(k), and she’d never carried credit card debt. But she had never had to turn a severance check and a concentrated stock position into a plan for an uncertain stretch ahead.

The Gap We Found

The severance and the accelerated vesting landed as a large lump of income in the first half of the year — and Microsoft withheld on it at the flat 22% supplemental rate, well below Yael’s actual marginal bracket. On paper she looked flush; in reality she was quietly under-withheld by tens of thousands and headed for a surprise tax bill plus an underpayment penalty. At the same time, roughly 40% of her liquid net worth was sitting in MSFT. Nobody was looking at the layoff as a tax event, a diversification event, and a cash-flow event all at once — because no single advisor had ever seen all three.

What We Did

First, we mapped the runway. Between severance, the emergency fund, her spouse’s income, and the newly liquid shares, we laid out an 18-month cash-flow plan so the job search could be deliberate rather than panicked. We bridged health coverage by comparing COBRA against enrolling in her spouse’s employer plan — the spouse’s plan won on cost and coverage.

Next, we handled the tax spike. Alphanso’s AI agents parsed her final Microsoft payroll to calculate exactly what had already been withheld against what she’d actually owe on the severance and accelerated RSUs. That flagged the gap early, so we scheduled the right quarterly estimated payment before the deadline instead of discovering the shortfall at filing. We also identified that her lower-income second half of the year opened a modest Roth conversion window worth revisiting once her next role was clear.

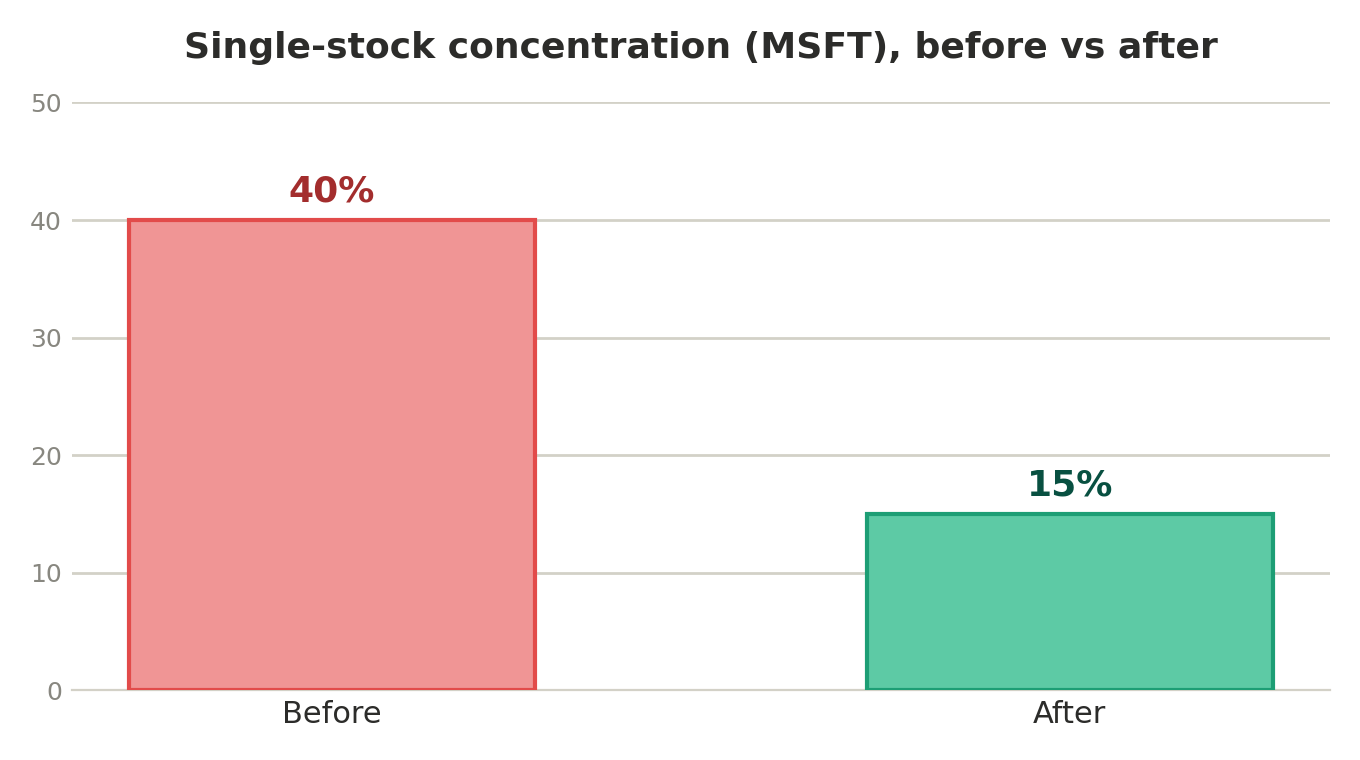

Finally, we used the transition to reduce the concentration risk she’d been carrying for years. Rather than dumping MSFT, we sold specific high-cost-basis lots to keep capital gains low, paired the sales with harvested losses elsewhere in the account, and redeployed the proceeds into a diversified direct-index portfolio. We rolled her 401(k) into an IRA to keep her options open and her fees low.

The Result

- Avoided an estimated $11,000 underpayment penalty by catching the withholding gap and scheduling the right quarterly payment proactively.

- Cut his single-stock concentration from roughly 40% of liquid net worth to under 15%, with minimal capital gains thanks to lot-by-lot selling and loss harvesting.

- Mapped an 18-month runway that let Omar take the right next job instead of the first one.

- Traded a stressful, open-ended unknown for a written plan he and his spouse could actually see.

Why This Worked

A layoff isn’t one problem — it’s a tax problem, an investment problem, and a cash-flow problem arriving on the same day. Yael’s CPA would have caught the tax issue in April; her old brokerage would never have flagged the concentration; no one was connecting the severance to the runway. Alphanso’s flat-fee, fiduciary model meant we could look at everything at once and act in her interest, not sell her a product. That integration is the whole point.

If you're facing a transition and want a plan before the next paycheck stops, we're here: https://alphanso.ai/request-a-callback

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

.png)

Schedule demo with our advisors

What to expect