An Intel engineer unwound a 487% winner without the tax bill she feared

The Situation

Linh is a 41-year-old silicon design engineer at Intel, based in Folsom, California. She has spent twelve years there, quietly accumulating RSUs through every vesting cycle and almost never selling. That discipline paid off in a way she never planned for. After a brutal stretch and then a sharp turn, including the recent Apple-silicon news, her Intel stock ran up roughly 260% year-to-date and nearly 487% over the trailing year. Her vested shares were suddenly worth about $1.4M.

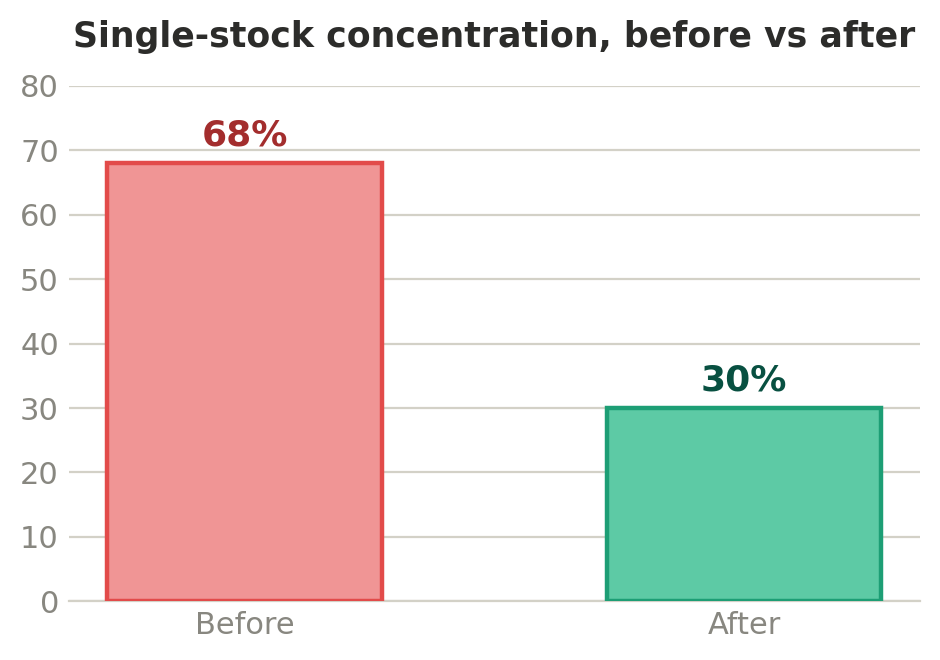

By any measure, she had done a lot right. She maxed her 401(k), funded an HSA, kept a healthy cash cushion, and had a CPA who filed clean returns every spring. The problem was not neglect. It was success she did not know how to handle. Her Intel position had grown to roughly 68% of her investable net worth, and every time she thought about trimming it, she ran the capital-gains math in her head, flinched, and did nothing.

The Gap We Found

No one was looking at the whole board. Her CPA saw last year's return, not the risk sitting in her brokerage account today. Her 401(k) was a separate world. And the one number that should have scared her was never on anyone's dashboard: that a single company stock now made up more than two-thirds of her wealth, after a 487% run that could reverse just as fast. She was so focused on the tax cost of selling that she had never priced the far larger risk of not selling. A position this concentrated is not a winning lottery ticket; it is an unhedged bet on one employer.

What We Did

First, we reframed the decision. The question was never "sell or hold." It was "how do we move from 68% to a sane 30% over time, paying the least tax legally possible along the way?" We built an 18-month staged unwind so gains landed across multiple tax years instead of detonating in one.

Then we made the tax bill smaller at every step. Using specific lot identification, we sold her highest-cost-basis shares first, the ones she had acquired near the top, so each dollar of diversification realized the smallest possible gain. We redeployed the proceeds into a direct-index portfolio, which holds hundreds of individual names and lets us harvest losses on the inevitable laggards. Those harvested losses then offset the gains from trimming Intel, so the new portfolio quietly helped pay for the diversification. This is the move a standalone CPA or a standalone broker almost never coordinates, because neither sees both sides.

Finally, the pieces only her CPA and advisor together could see. Linh gives to her alma mater every year, so instead of writing checks, we had her donate her lowest-basis Intel shares to a donor-advised fund, eliminating the embedded capital gain on those shares entirely while still giving her a deduction at full market value. And because realizing gains can quietly blow up quarterly taxes, Alphanso's AI agents tracked her estimated payments in real time, flagging exactly what to pay each quarter so a surprise underpayment penalty never showed up.

The Result

- Cut single-stock concentration from 68% to 30%, diversifying roughly $750K out of Intel and into a resilient, tax-managed portfolio.

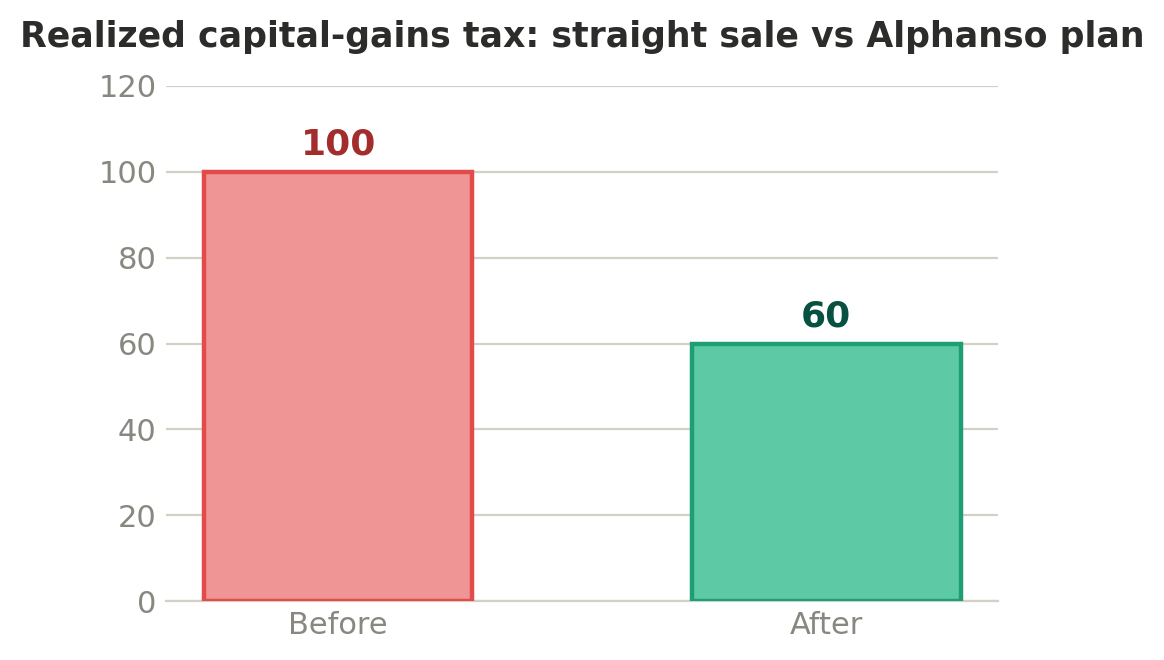

- Kept her realized capital-gains tax roughly 40% lower than a straight sale would have triggered, thanks to high-basis-lot selling, harvested losses, and multi-year staging.

- The donor-advised fund gift erased the gain on her donated shares and generated a five-figure charitable deduction, turning annual giving she would do anyway into a tax win.

- For the first time in years, she stopped losing sleep over one stock, and never got hit with an estimated-tax surprise.

Why This Worked

None of these moves were exotic. The value came from someone seeing all of it at once: the concentration risk, the cost basis on every lot, the charitable habit, and the quarterly tax mechanics, and sequencing them so each decision made the next one cheaper. That is what a flat-fee fiduciary model makes possible: we are paid to look at the whole picture, not to sell a product or bill against assets we would rather you never touch. If you are sitting on a winner you are afraid to trim, there is almost always a better path than "hold and hope." Talk to us about yours.

Disclosure

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect