How a Google PM turned GSU whiplash into early retirement at 45

The situation

Naomi is a 44-year-old senior product manager at Google in Mountain View, married with one child in middle school. Over eleven years she climbed to L6, and her compensation followed: a base salary in the low $300Ks, a bonus, and Google Stock Units (GSUs) that had grown into the largest single line on her net-worth statement. On paper she was doing everything right — maxing her 401(k), holding an emergency fund, and quietly dreaming about stepping away from full-time work by 45.

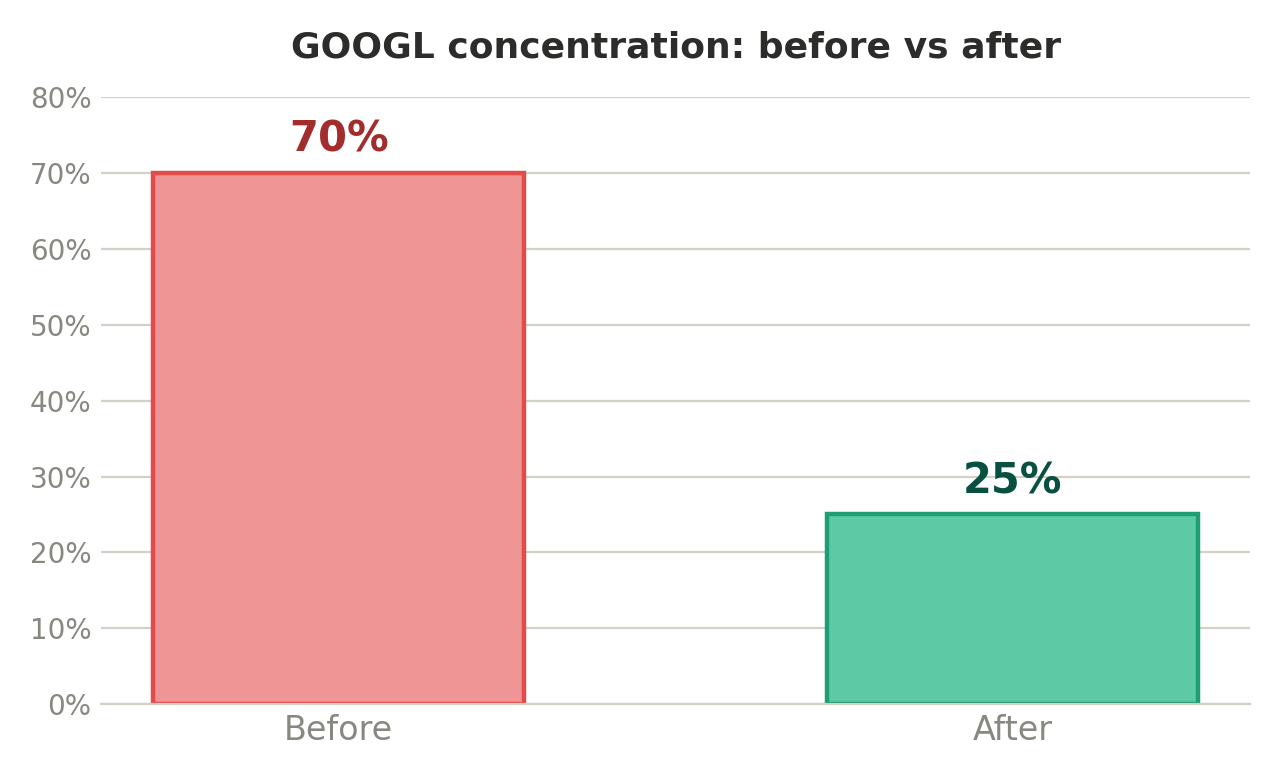

But the ride never felt smooth. GOOGL would run up, and she would feel wealthy; it would pull back, and the early-retirement math would suddenly look shaky. Nearly 70% of her liquid net worth sat in a single stock, and every vest added more. Her CPA filed clean returns, her 401(k) was in a target-date fund, and a robo-advisor held a small taxable account — but no one was connecting those pieces to the question that actually kept her up at night: could she really afford to retire early, and how would she get there without a brutal tax bill?

The gap we found

Naomi did not have a bad advisor — she had no one looking at the whole board. Her concentration risk, her vesting schedule, her tax bracket, and her early-retirement timeline were four separate conversations that never happened in the same room. The result: she was letting GSUs pile up out of loss-aversion, taking on the risk of a single stock without a plan to convert that paper wealth into a durable, diversified income stream she could actually retire on.

What we did

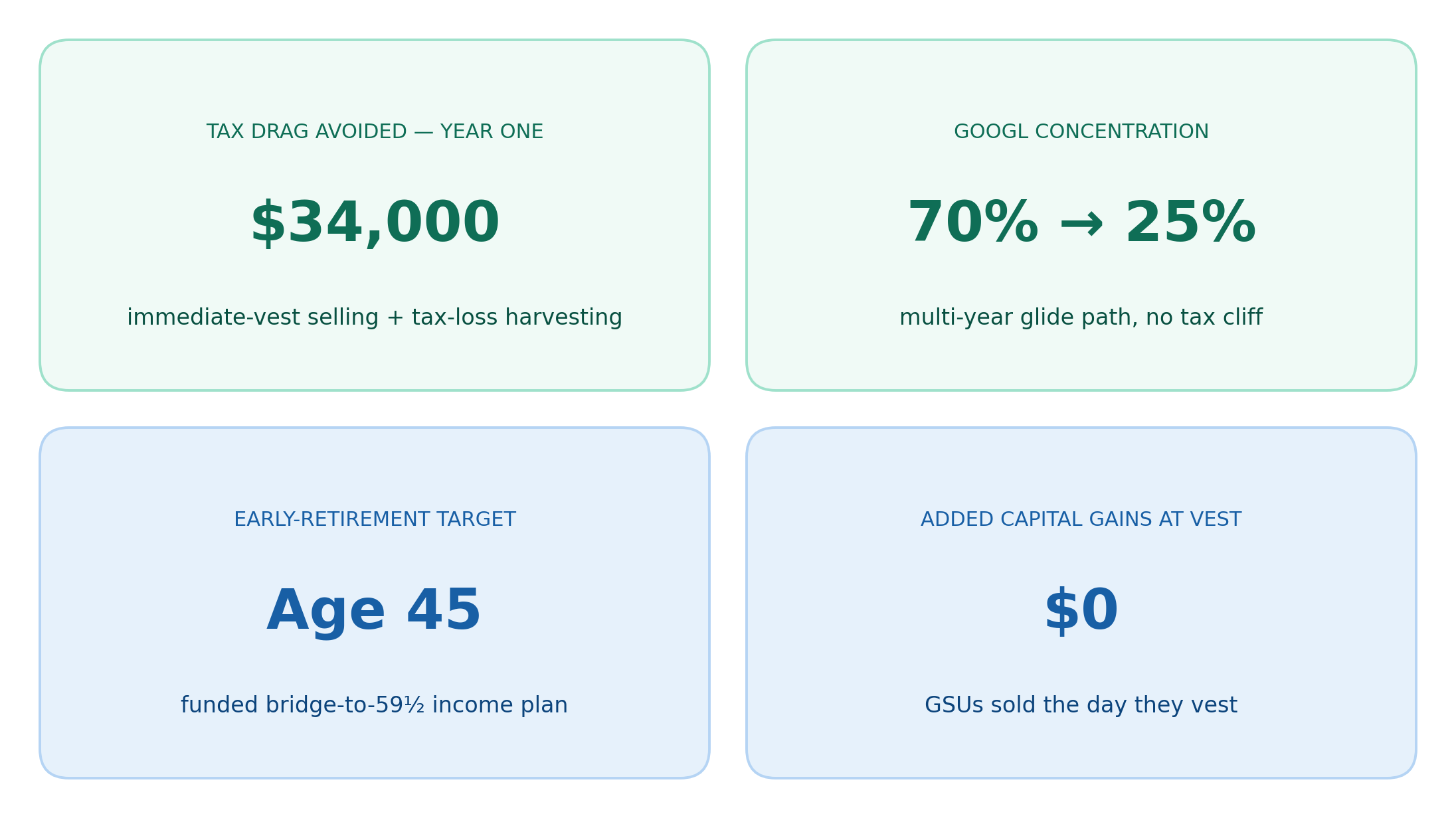

First, we turned the volatility into a discipline. We set a rule to sell GSUs immediately at each vest — because shares sold the moment they vest carry $0 in additional capital gains — and redirected the proceeds into a diversified, low-cost portfolio. That alone began dismantling the concentration risk without triggering a surprise tax event.

Second, we unwound the existing concentrated position gradually rather than all at once. Using specific-lot identification and Direct Indexing with ongoing tax-loss harvesting, we sold down the oldest, highest-basis lots first and used harvested losses to offset the gains — trimming her single-stock exposure from roughly 70% toward 25% over a multi-year glide path instead of one taxable cliff.

Third, we built the actual retirement engine. We mapped a bridge plan for the years between 45 and 59½, when 401(k) withdrawals get expensive, using her growing taxable account and a municipal bond ladder for tax-efficient income. Alphanso's AI agents track her vesting calendar and parse her payroll so estimated taxes are calculated and flagged before each quarterly deadline — no more April surprises from a big vest. We also layered in Roth conversions for any lower-income year once she scales back.

The result

- Concentration in GOOGL cut from ~70% to a target 25%, on a planned glide path — without a single large tax cliff.

- Roughly $34,000 in tax drag avoided in year one through immediate-vest selling and tax-loss harvesting.

- A funded bridge-to-59½ income plan that made “retire at 45” a dated line on a spreadsheet instead of a hope.

- Naomi stopped checking the stock price every morning — the plan, not the ticker, now runs the timeline.

Why this worked

The win never came from a single clever product. It came from putting investments, taxes, and the early-retirement timeline under one roof so decisions reinforced each other instead of working at cross-purposes. Because Alphanso is a flat-fee fiduciary — no AUM percentage, no commissions — the advice is measured by Naomi's outcome, not the size of her portfolio. That is the difference between owning a pile of company stock and owning a plan.

If your equity has outgrown your plan, we can help you build the glide path. Request a callback.

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect