He left Google for a startup mid-year. We tamed the double-vest tax year.

The Situation

Arjun — "AJ" to almost everyone — is a 35-year-old staff software engineer in the Bay Area. He spent six years at Google, climbing to a level where a meaningful chunk of his pay arrived as GSUs (Google's version of RSUs). In April, his two youngest GSU tranches vested during the year, and by early summer a fast-growing Series B startup made him an offer he couldn't pass up: a leadership role, a higher base, and a fresh equity grant. He said yes and started in July.

AJ is organized. He maxes his 401(k), keeps a CPA who files a clean return every spring, and had never owed a surprise at tax time. His wife earns a steady salary of her own, and together they were used to a life where withholding just quietly took care of itself. Nothing about his situation looked risky — which is exactly why the problem hiding inside it was so easy to miss.

The Gap We Found

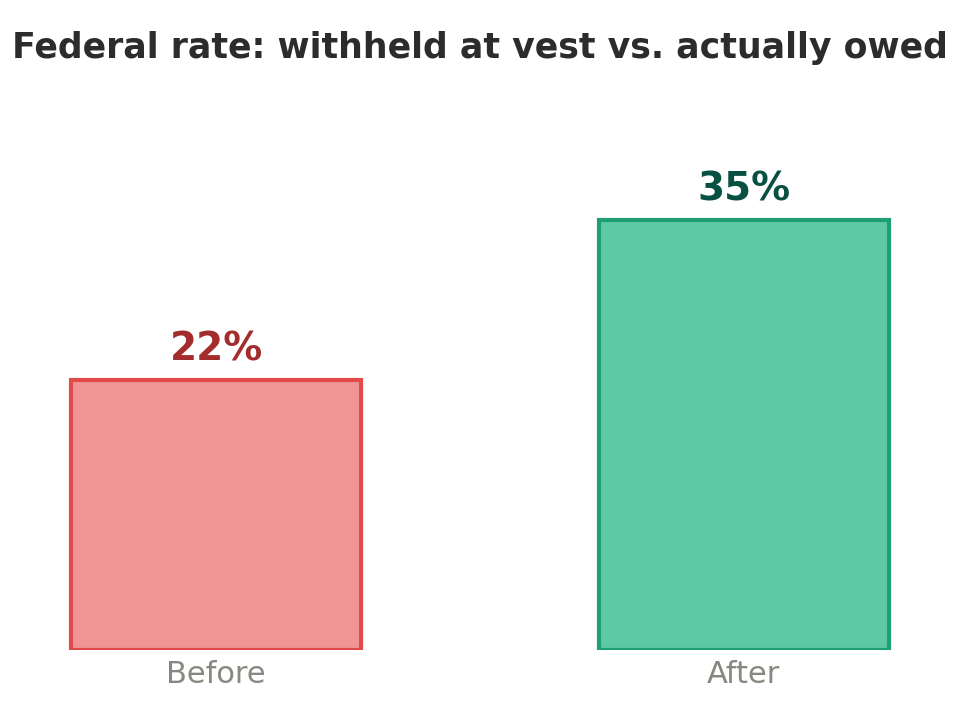

Changing jobs mid-year quietly created a "double-vest" tax trap. Google had withheld on his GSU vesting at the standard 22% federal supplemental rate, and his new employer withheld on his salary and sign-on equity as if that job were his only income for the year. Neither payroll system knew about the other. Stacked together, AJ's combined 2026 income landed his family solidly in the 35% bracket — but he'd been withheld as though he were in the low-to-mid-20s on a large share of it. On paper his setup looked fine; underneath, he was heading toward a five-figure shortfall and a potential underpayment penalty he had no idea was coming.

What We Did

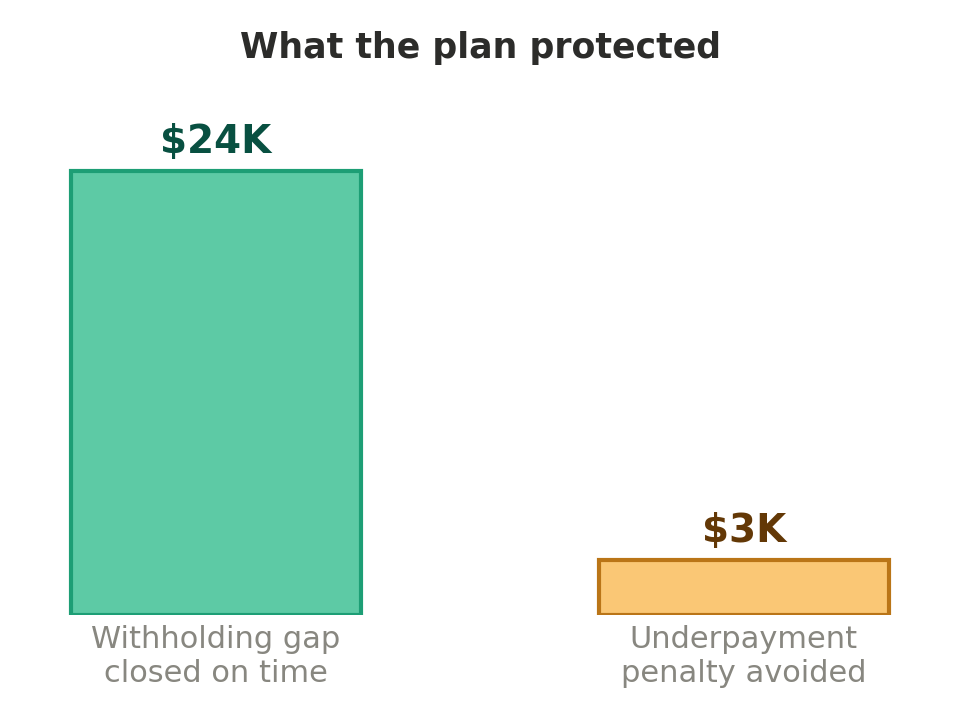

First, we got the whole year on one page. Our AI agents parsed both employers' payroll data — Google's through July and the startup's from July on — and reconciled taxes already paid against what his true blended rate would actually owe. That surfaced the exact gap: roughly $24,000 of under-withholding once both incomes and the vested GSUs were counted together. Rather than let it balloon into an April surprise plus a penalty, we scheduled a corrected Q3 and Q4 estimated payment so the IRS was made whole on time. The system now flags each quarterly deadline before it arrives, so this never sneaks up on him again.

Second, we handled the concentrated Google stock he'd been accumulating. His vested GSUs had grown into a position worth more than a quarter of the family's investable assets — a lot of risk tied to one former employer. Because shares sold right at vest carry little or no capital gain, we sold the freshly vested lots immediately and redirected the proceeds into a diversified, direct-indexed portfolio, using specific-lot identification to trim the older, lower-basis shares only where it was tax-efficient.

Third, we cleaned up the startup equity and benefits. We reviewed his new option grant and vesting schedule, set expectations on the illiquidity of private shares, re-pointed his 401(k) contributions so he wouldn't over- or under-fund after the mid-year switch, and updated beneficiary designations that still listed only his old Google accounts.

The Result

- Closed a ~$24,000 withholding gap on time and sidestepped an estimated-tax underpayment penalty of several thousand dollars.

- Cut single-stock concentration from over 25% of investable assets to under 10%, with minimal capital-gains cost.

- Turned a stressful job change into a coordinated plan — one team watching taxes, investments, and benefits at once.

- Gave AJ a standing quarterly-estimate system so a double-income year never catches him off guard again.

Why This Worked

AJ's CPA wasn't wrong and his old advisor wasn't careless — they simply never saw both halves of his year at the same time. The double-vest problem only appears when someone is looking at the full picture: two payrolls, a vesting schedule, and a bracket change, all at once. That's what an integrated, flat-fee, fiduciary team is built to do. No AUM fee nudging us toward one product; just a plan that connects the pieces. If a mid-year move or a big vest is on your horizon, we'd be glad to walk through it with you — request a callback.

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect