A Google engineer was 80% in GOOGL. Here's how we diversified without a tax shock.

The Situation

Soo-Jin, a 43-year-old staff software engineer, had spent eleven years at Google in Mountain View. Every year her GSUs vested, and every year she did the responsible thing: she held. She believed in the company, the stock had been good to her, and selling felt like a bet against her own employer. By the time she came to us, GOOGL made up roughly 80% of her investable net worth — about $1.6M of a $2M portfolio sitting in a single ticker.

She wasn't careless. She maxed her 401(k), had a solid CPA who filed a clean return every April, and kept a healthy cash cushion for her family of four. But no one had ever sat her down and asked the uncomfortable question: what happens to your retirement, your kids' college, and your home plans if this one stock has a bad three years?

The Gap We Found

The problem wasn't that Soo-Jin was doing anything wrong — it's that concentration risk lives in a blind spot no single advisor was watching. Her CPA saw her tax return but not her brokerage account. Her employer's stock plan portal showed her the shares but said nothing about risk. Nobody had connected the two facts that mattered most: she was dangerously overexposed to one company, and unwinding that position naively would have handed her a six-figure capital gains bill in a single year.

What We Did

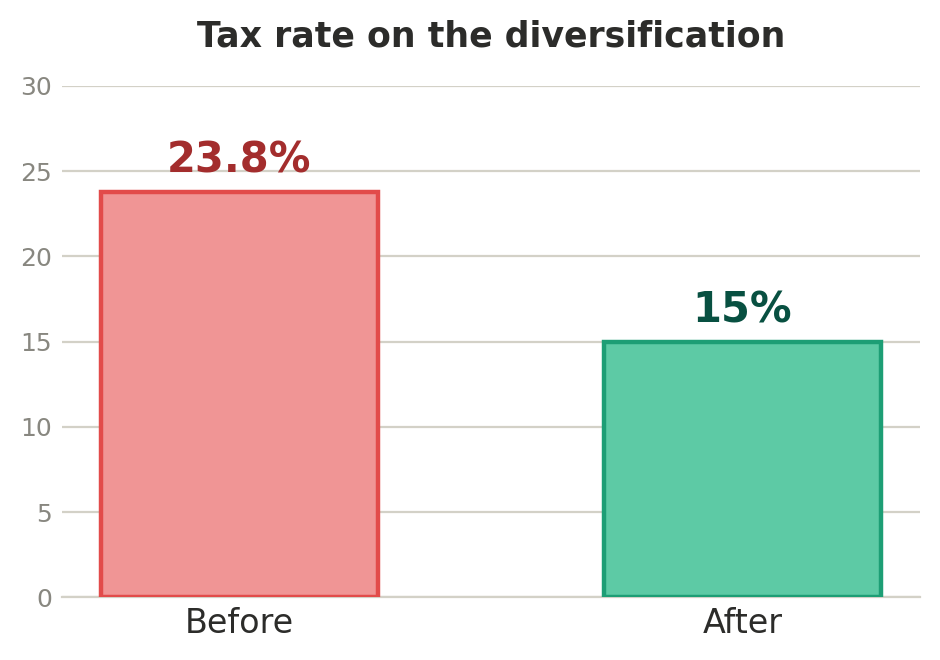

We built a multi-year diversification plan designed to bring GOOGL down to a target of about 20% of her portfolio without ever triggering a tax shock. The first move cost nothing: from that point forward, we sold each new GSU lot the moment it vested. Because shares are taxed as ordinary income at vest, selling immediately means $0 additional capital gains on that lot — so she could stop adding to the concentration for free while we worked down the existing pile.

For the shares she already held, we used specific-lot identification to sell her highest-cost-basis lots first, minimizing the gain realized on each sale, and we spread the selling across several tax years to keep her inside a lower capital gains bracket. Alongside that, we moved the proceeds into a direct indexing portfolio rather than a plain index fund. Direct indexing holds the underlying stocks individually, which let us harvest losses on the down positions each year and bank those losses to offset the gains from selling her GOOGL — so the diversification largely paid for its own tax bill.

The Result

- Reduced GOOGL from 80% to a target 20% of her portfolio over a planned three-year glide path — cutting her single-stock risk by roughly three-quarters.

- Kept every year's realized gains inside the 15% long-term capital gains bracket, avoiding the jump to 20% plus the 3.8% net investment income tax.

- Generated $9,000+ in harvested losses in year one through direct indexing, directly offsetting the gains from her GOOGL sales.

- Soo-Jin finally stopped losing sleep over a single earnings report deciding her family's future.

Why This Worked

None of these moves are exotic. They worked because someone was finally looking at the whole picture at once — the portfolio, the tax brackets, the vesting schedule, and the goals — instead of each piece in isolation. That's the difference integration makes: her CPA was never going to tell her to diversify, and her stock portal was never going to tell her about tax lots. Because Alphanso is a flat-fee fiduciary, we had no incentive to churn her account or sell her a product — just to get her out of a risky position as tax-efficiently as possible. If your net worth is riding on one ticker, it's worth a conversation: https://alphanso.ai/request-a-callback

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

.png)

Schedule demo with our advisors

What to expect