From Amazon RSU rollercoaster to FIRE at 47

The Situation

Yvonne is a 44-year-old principal engineer at Amazon in Seattle. Over fifteen years she'd climbed to L7, ridden AMZN through every peak and dip, and watched her net worth balloon largely on the back of company stock. She and her husband — who runs a small design studio — have two teenagers and one clear goal: Yvonne wants to walk away from the grind at 47 and never depend on a vesting schedule again.

She wasn't starting from zero on the fundamentals. She maxed her 401(k) every year, kept a CPA for her taxes, and had a brokerage advisor managing her index funds. On paper, she looked like someone who had it together. But every time a big vest landed, the same anxious question came back: is this actually enough to retire eighteen years before Medicare — and if it is, how do I get the money out without wrecking myself on taxes?

The Gap We Found

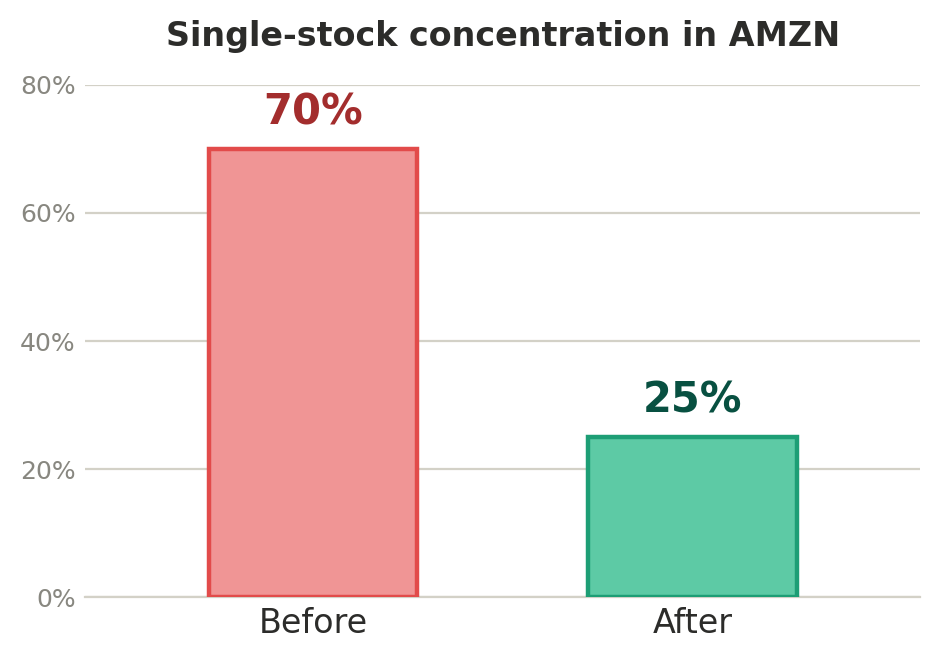

Nobody had modeled the mechanics of an early exit. Retiring at 47 means roughly twelve years before penalty-free 401(k) withdrawals at 59½, and eighteen years before Medicare at 65. That's a long, unfunded bridge — and none of Yvonne's advisors were looking at it, because none of them could see the whole board. Her CPA filed accurate returns but worked reactively, after the year was over. Her brokerage advisor managed the portfolio but had no view into her tax brackets or her withdrawal timeline. And her single biggest risk — nearly 70% of her liquid net worth sitting in AMZN — was quietly hiding in plain sight.

What We Did

First, we addressed concentration without triggering a tax shock. Instead of selling AMZN in one lump, we used specific-lot identification to trim the highest-basis shares first and moved the proceeds into a direct-indexing portfolio. That kept Yvonne's market exposure broadly intact while continuously harvesting losses she could bank against future gains. Over the plan horizon, that pulled her single-stock concentration from roughly 70% down toward 25%.

Then we built the bridge. We mapped a Roth conversion ladder that fires in the low-income years right after she leaves Amazon — converting a measured slice of her traditional 401(k)/IRA each year while her bracket is low, then drawing on those converted dollars penalty-free five years later. Alongside it, we sized a taxable brokerage "bridge account" and a cash buffer to cover the first stretch of retirement and blunt sequence-of-returns risk if markets fall early. Because Yvonne will be buying her own health insurance until 65, we tied the whole withdrawal plan to her ACA income — keeping her modified adjusted gross income in a band that preserves premium subsidies rather than accidentally spending them away.

Finally, while she's still working and still vesting, our AI agents watch each RSU event in advance, run the tax scenario before it lands, and flag the quarterly estimated payment so a windfall vest never turns into an April surprise or an underpayment penalty.

The Result

- Single-stock concentration cut from ~70% of liquid net worth to under 25%, with the diversification spread across several tax years to avoid a large one-time bill.

- An estimated $9,500+ per year in tax drag reduced through direct indexing and loss harvesting, plus a Roth ladder that moves retirement dollars at a far lower lifetime rate.

- A funded, year-by-year bridge to age 59½ — including a health-insurance plan that keeps ACA subsidies intact.

- A confirmed exit date: Yvonne now has a written plan that says 47 is realistic, not a hope.

Why This Worked

None of these moves were exotic. What was missing was someone looking at the investments, the taxes, the healthcare gap, and the retirement timeline as one connected system — which is exactly where an integrated, fiduciary, flat-fee advisor earns their keep. Yvonne's CPA and her old brokerage weren't doing anything wrong; they simply couldn't see past their own lane. When one team owns the full picture, an early retirement stops being a leap of faith and becomes a schedule. If you're staring at your own vesting screen wondering whether the number is real, let's talk it through.

Disclosure

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

.png)

Schedule demo with our advisors

What to expect