A Microsoft engineer had $700K riding on one stock

The Situation

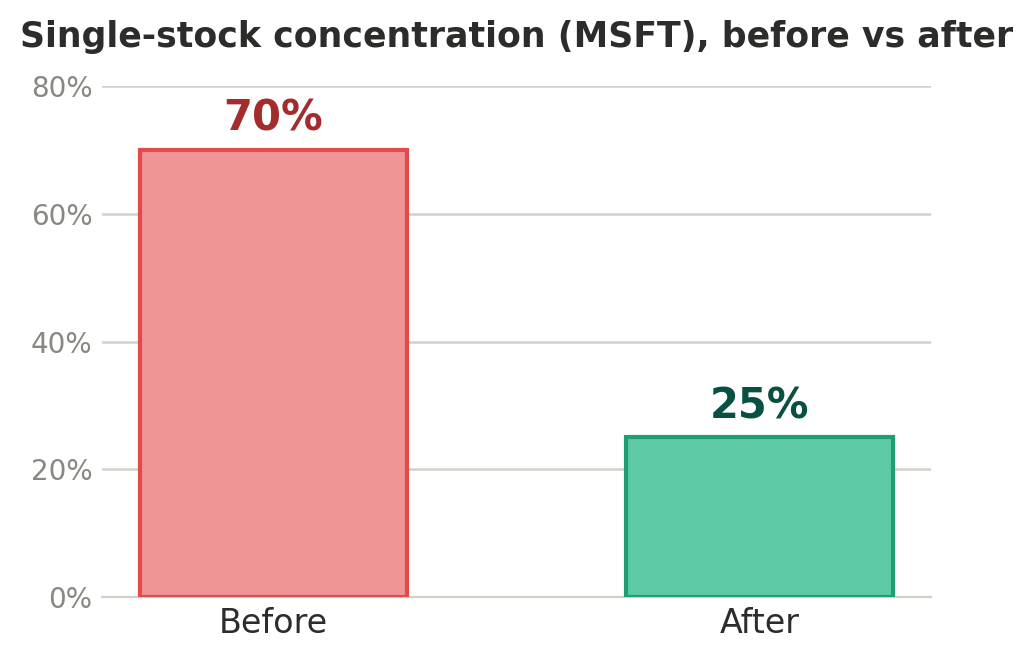

Soo-jin, 46, is a principal engineer at Microsoft in Redmond. Over fifteen years and several promotions, he'd done what a lot of long-tenured Microsoft employees do without ever quite deciding to: he let his RSUs pile up. Every vest, he meant to sell some — and never got around to it. By the time he came to us, roughly $700K of his liquid net worth, close to 70%, was sitting in a single position: MSFT.

He wasn't reckless. He maxed his 401(k), funded his two teenagers' 529 plans, and had a CPA who filed a clean return every year. On paper he was doing everything right. But the stock had quietly become the tail wagging the dog — one bad year for one company could reshape his family's entire financial future. Living in Washington, with no state income tax but no cushion either, didn't change the concentration math.

The Gap We Found

No one had ever told him that not selling was itself a decision worth planning. His CPA saw the tax return after the fact; his 401(k) provider saw only the 401(k). Nobody was looking at the whole picture and asking the obvious question: what happens to this family if MSFT drops 40%? The concentration was the risk — and unwinding it carelessly would have handed him a large, avoidable capital-gains bill all in one year.

What We Did

We built a multi-year diversification plan instead of a fire sale. First, we identified the specific tax lots — the exact share batches with the highest cost basis — so each sale triggered the smallest possible gain. Selling the right lots first let us raise real money while keeping the tax hit low.

Second, we set his future vests to sell automatically at vest. RSUs are taxed as ordinary income the day they vest, so selling immediately means little or no additional capital gain — the tax is already paid. Going forward, new shares would fund a diversified portfolio rather than deepen the concentration. Alphanso's AI agents track each upcoming vest and run the tax scenario in advance, so the plan is ready before the shares hit his account.

Third, we moved the proceeds into a direct-indexing portfolio. Rather than buying a single index fund, direct indexing holds the individual stocks that make up the index, which lets us harvest losses on the names that dip in any given year. Those harvested losses offset the gains from selling his MSFT — so the two strategies fund each other. His advisor sequenced the whole unwind across three tax years to keep every year in a comfortable bracket.

The Result

- Reduced his single-stock concentration from ~70% of liquid net worth to under 25% over an 18-month plan.

- Harvested losses offset roughly $60K of the capital gains generated by selling MSFT.

- His go-forward vests now diversify automatically — no willpower required.

- He stopped checking the stock price with his stomach in a knot.

Why This Worked

The concentration wasn't a mistake — it was the natural result of no one owning the full picture. Alphanso's flat fee meant we had no reason to rush the sale or churn the account; we were paid the same whether he held MSFT or diversified. Because we saw the taxes and the portfolio together, we could turn a nerve-wracking $700K position into an orderly, low-tax transition. If your net worth is riding on your employer's stock, you can see how we'd approach it — request a callback at alphanso.ai/request-a-callback.

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

.png)

Schedule demo with our advisors

What to expect