A Meta engineer diversified $2M in stock without the tax hit

The Situation

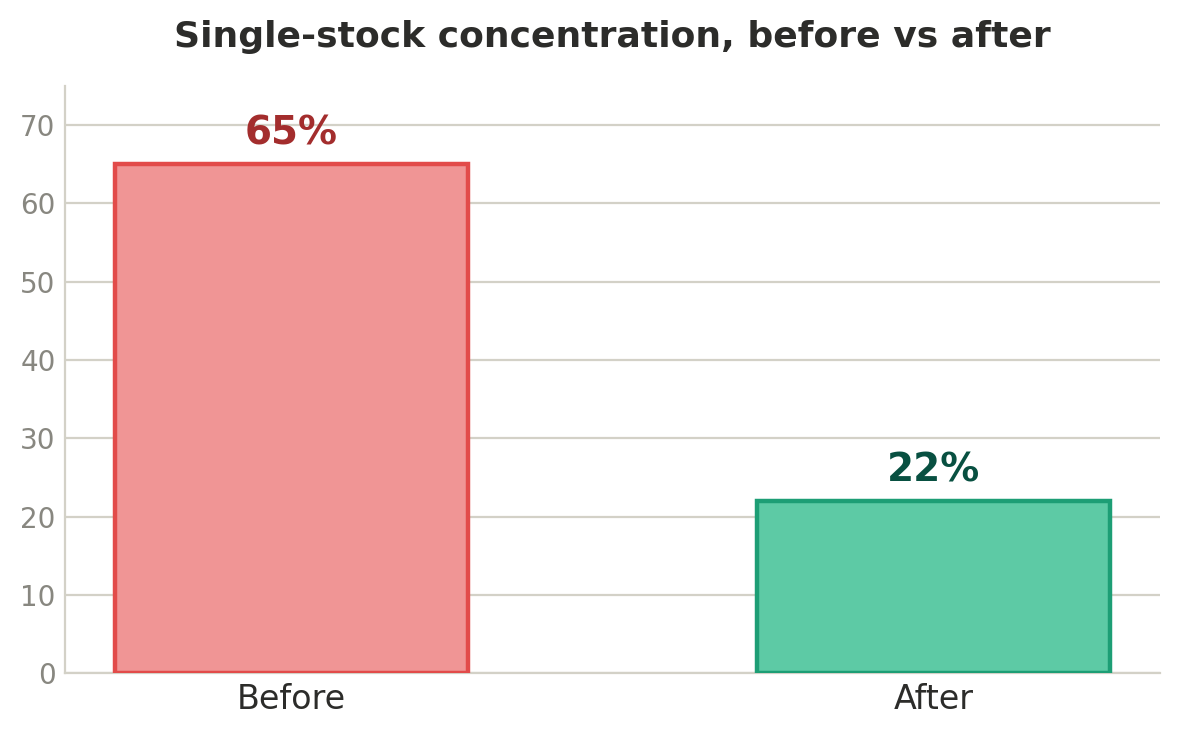

Daniel is a 38-year-old E6 engineer at Meta in the Bay Area. He's very good at his job, and for years the market has rewarded him for it — his RSUs vest every quarter, and he's diligently held onto nearly every share since 2024. When Meta ran up to record highs this month on the strength of its cloud-business pivot, his stock position didn't just grow, it swelled. By the time he came to us, a single stock — his employer's — made up about 65% of his net worth.

He'd done a lot right. He maxed his 401(k), kept a healthy emergency fund, and had a good CPA who filed a clean return every April. What he didn't have was a plan for the pile. Every vest added to it, and the rally made the position bigger and the reluctance to sell stronger. Selling felt like betting against a stock that kept going up. Not selling felt like standing under something that got heavier each quarter.

The Gap We Found

Nobody was looking at the concentration as a single, solvable problem. Daniel's CPA saw last year's tax return but not the embedded gains sitting in his brokerage account. His RSU withholding was happening at the standard 22% supplemental rate, well below his actual ~37% federal bracket plus California — so every vest quietly widened an under-withholding gap he'd only discover at tax time. And there was no framework at all for how to unwind a position with a large embedded gain without triggering a tax bill big enough to scare him back into inaction. The pieces existed. No one was holding them at once.

What We Did

First, we changed the default going forward. New RSUs now get sold at vest, automatically. Because a share's cost basis resets to its market value the moment it vests, selling right away means little or no capital gain on that lot — so future vests stop feeding the concentration instead of adding to it. That one change turned an ever-growing pile into a fixed problem we could actually size.

Then we tackled the legacy shares — the appreciated stock he'd been holding since 2024 — deliberately, over about 24 months rather than in one painful sale. Using specific-lot identification, we sold the highest-cost-basis shares first to keep the realized gain low, and we reinvested the proceeds into a direct-indexing portfolio: a diversified basket of stocks Daniel owns directly. That structure matters, because it harvests small losses automatically throughout the year, and we used those harvested losses to offset the gains from unwinding the Meta position. Diversification and tax management became the same move instead of competing ones.

Finally, we closed the withholding gap. Alphanso's AI agents parse Daniel's payroll and vesting data, calculate what he actually owes against what's already been withheld, and flag the right quarterly estimated payment before each deadline — so the RSU under-withholding stops turning into an April surprise and a potential underpayment penalty.

The Result

- Single-stock concentration reduced from 65% to roughly 22% over the planned unwind — the position went from his biggest risk to a normal holding.

- The tax cost of diversifying was cut to about a third of what a blind, all-at-once sale would have triggered, thanks to lot selection plus harvested losses from the direct-index portfolio.

- ~$8K in projected underpayment penalties avoided in year one, with quarterly estimates now handled proactively rather than reconstructed at tax time.

- Daniel stopped dreading his own vesting schedule. The quarterly vest is now a scheduled, boring event — which is exactly what he wanted.

Why This Worked

None of these moves were exotic. They worked because someone finally looked at the investment position, the embedded gains, and the tax withholding as one connected picture — the thing a CPA, a brokerage, and a payroll system will never do on their own. Because Alphanso charges a flat fee rather than a percentage of assets, our only incentive was to solve Daniel's problem, not to grow or protect the balance we manage. And because we're a fiduciary, "sell your employer's stock" was advice we could give freely when it was the right call. If you're watching one stock quietly take over your net worth and you're not sure how to unwind it without a giant tax bill, we'd love to walk you through it: https://alphanso.ai/request-a-callback

This case study is a composite illustration based on real Alphanso client scenarios. Names and identifying details have been changed for privacy. Results are not guaranteed and will vary based on individual circumstances. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Schedule demo with our advisors

What to expect