The 2026 AMT Trap: Why the Same ISO Exercise That Was Safe Last Year Could Cost You $20,000 More This Year

A lot of engineers at pre-IPO AI companies are modeling their ISO exercise timing right now. They're looking at what a colleague did in 2024 or 2025 — similar income, similar grant, similar exercise size — and using that as a reference point.

That reference point is broken. Two changes buried in the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, mean the same exercise that produced a manageable AMT bill last year may produce a significantly larger one in 2026. The changes are quiet, technical, and almost nobody in the financial press covered them. But if you hold ISOs at OpenAI, Anthropic, xAI, Databricks, or any other company approaching a liquidity event, they affect you directly.

How AMT Works on ISO Exercise — The Short Version

When you exercise an Incentive Stock Option (ISO), you don't owe regular income tax on the spread — that's the gap between your exercise price and the stock's current fair market value. That's the whole appeal of ISOs.

But the IRS has a second tax system called the Alternative Minimum Tax (AMT). Under AMT rules, that spread is counted as income — a "preference item" — even though you haven't sold anything and no cash has changed hands.

So you calculate your regular tax, then you calculate your AMT, and you pay whichever is higher.

The AMT has two rates: 26% on the first $220,700 of taxable AMTI (Alternative Minimum Taxable Income), and 28% above that.

What protects most people from AMT is the AMT exemption — a deduction that reduces your AMTI before the tax is calculated. In 2026, that exemption is $90,100 for a single filer.

Here's where the OBBBA matters.

Two Changes. Same Direction. Bigger Bill.

The OBBBA made two specific changes to how the AMT exemption works for 2026 onward:

Change #1: The phaseout threshold dropped significantly.

Under the 2025 tax rules, the AMT exemption didn't start shrinking until your AMTI crossed $626,350 (for single filers). In 2026, that threshold drops to $500,000 — a $126,350 decrease.

That means an engineer who was safely below the phaseout zone last year may now find themselves inside it — without exercising a single additional share.

Change #2: The phaseout rate doubled.

In 2025, you lost $0.25 of exemption for every $1 of AMTI above the threshold. In 2026, you lose $0.50 for every $1.

The practical effect: the exemption disappears twice as fast. Under 2026 rules, a single filer's $90,100 exemption is completely gone by the time AMTI reaches $680,200. Under 2025 rules, you'd need AMTI of $978,500 before the exemption was fully gone.

Both changes move in the same direction. Together, they create a materially narrower window for ISO exercise without triggering meaningful AMT.

The Math on a Real Example

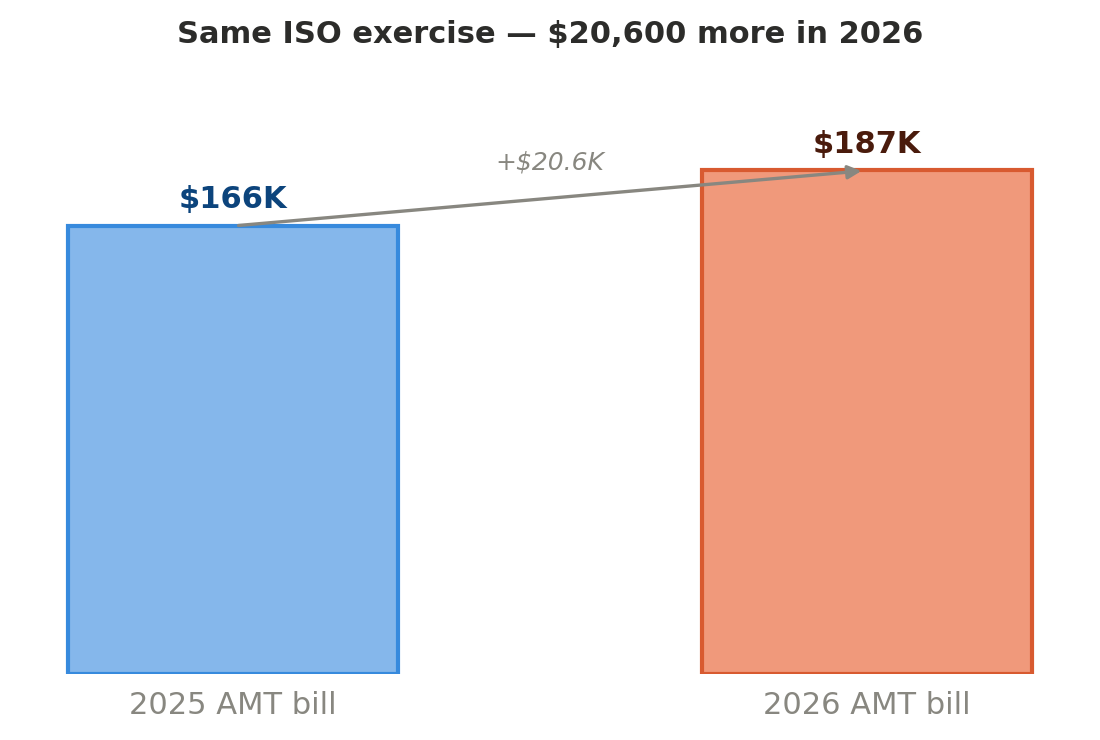

Jordan is a Senior ML Engineer at OpenAI, earning $220,000 in W-2 base salary, with 25,000 ISOs at a $2 strike price. The current 409A fair market value is $60/share.

Jordan is considering exercising 8,000 shares this year. The spread: 8,000 × ($60 - $2) = $464,000. Total AMTI: $220,000 + $464,000 = $684,000.

In 2025: Jordan is $57,650 above the threshold. At 25% phaseout, loses $14,412 of the $88,100 exemption. Net exemption: $73,688. AMT bill: approximately $166,500.

In 2026: Jordan is $184,000 above the new $500,000 threshold. At 50% phaseout, the entire $90,100 exemption is wiped out. AMT bill: approximately $187,100.

Same engineer. Same company. Same shares. $20,600 more AMT.

And when you're inside the phaseout zone, the effective marginal AMT rate isn't 28% — it's 42%, because every extra dollar of AMTI also costs you $0.50 of exemption, which is itself taxed at 28%.

What You Can Do About It

1. Calculate your safe exercise amount first. Your safe zone: $500,000 minus your regular taxable income. For Jordan, that's $280,000 of ISO spread before any phaseout — $126,350 less room than in 2025.

2. Spread the exercise over multiple years. Keeping AMTI near $500,000 each year preserves more of your exemption and avoids the 42% effective rate.

3. Understand the AMT credit. When you pay AMT, you earn a Minimum Tax Credit usable in future years when regular tax exceeds AMT. It doesn't expire — but you get it back later, not now. Build the recapture into your multi-year model.

4. Model a disqualifying disposition as a last resort. Exercising ISOs and selling in the same calendar year converts the spread to ordinary income, eliminating the AMT preference item entirely — but at the cost of long-term capital gains treatment.

5. If you're in lockup right now, use the window. The planning you do before a lockup ends determines whether you capture ISO gains efficiently or hand a disproportionate share to the IRS.

The Bottom Line

The OBBBA quietly made the AMT more expensive for exactly the people who hold ISOs at high-growth AI companies. The phaseout kicks in $126,350 earlier. It runs twice as fast. The effective marginal rate inside the phaseout zone is now 42%.

If you're modeling ISO exercise timing based on what you or a colleague did in 2025, recalibrate. The math changed on July 4, 2025, and it didn't change in your favor.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)