Tax Smart Charitable Donations in 2026

If you're in a big RSU year and you write checks to charity every December, the math you've been running in your head is now wrong. Two quiet rule changes took effect this year that shrink the value of every dollar you itemize — and they hit equity-comp households the hardest, because your income spikes are exactly what triggers them.

I've spent a lot of time this year walking high earners through this, and almost nobody saw it coming. Let me show you what changed, why it catches people, and what you can actually do about it before December.

What's Actually Happening

Two separate haircuts landed for the 2026 tax year, both courtesy of the 2025 law (the "One Big Beautiful Bill Act," or OBBBA).

Haircut #1 — the 35-cent cap. If you're in the top 37% federal bracket, your itemized deductions are now worth only 35 cents on the dollar, not 37. The IRS does this through what advisors are calling the "2/37 rule": your itemized deductions get reduced by 2/37 of the amount that lands in the top bracket. The practical effect is a flat 2% surtax on everything you itemize — charitable gifts, mortgage interest, state taxes, all of it. For 2026, the 37% bracket starts at $768,700 of taxable income for a married couple filing jointly ($640,600 single).

Haircut #2 — the 0.5% charitable floor. Starting this year, itemizers can only deduct charitable gifts to the extent they exceed 0.5% of adjusted gross income (AGI — your total income before deductions). So if your AGI is $800,000, the first $4,000 you give is no longer deductible at all. It's a deductible underneath which your generosity simply doesn't count.

Here's the concrete version. Say you're "Maya," a senior staff engineer at a chip company, married, with an $850,000 household income in 2026 thanks to a large vest. Your AGI is about $820,000. You and your spouse give $25,000 a year to causes you care about, and your total itemized deductions come to roughly $60,000.

- The 0.5% floor: 0.5% × $820,000 = $4,100. Only $20,900 of your $25,000 gift is deductible.

- The 35-cent cap: 2/37 × $60,000 ≈ $3,240 of your itemized deductions are disallowed. Deducted at 37%, that's about $1,200 of extra tax — the 2% surtax on $60,000.

Neither number is catastrophic on its own. But they stack, they repeat every single year, and they're invisible unless someone points them out.

Why This Catches People

Smart, financially literate people get blindsided here for one reason: the headline news in 2025 was all good. The brackets were made permanent. The SALT cap (the deduction for state and local taxes) jumped from $10,000 to $40,000. The standard deduction went up to $32,200 for married couples. Everyone read "tax cut" and stopped reading.

Buried under the good news were these two limitations, written specifically for high earners. And there's a cruel interaction nobody talks about: that generous new $40,000 SALT cap phases back down once your modified AGI clears about $505,000, dropping back toward $10,000 for households over roughly $600,000. So in your biggest RSU years — the years you assume you have the most deductions to work with — you actually have the fewest, and the ones you have are worth only 35 cents on the dollar.

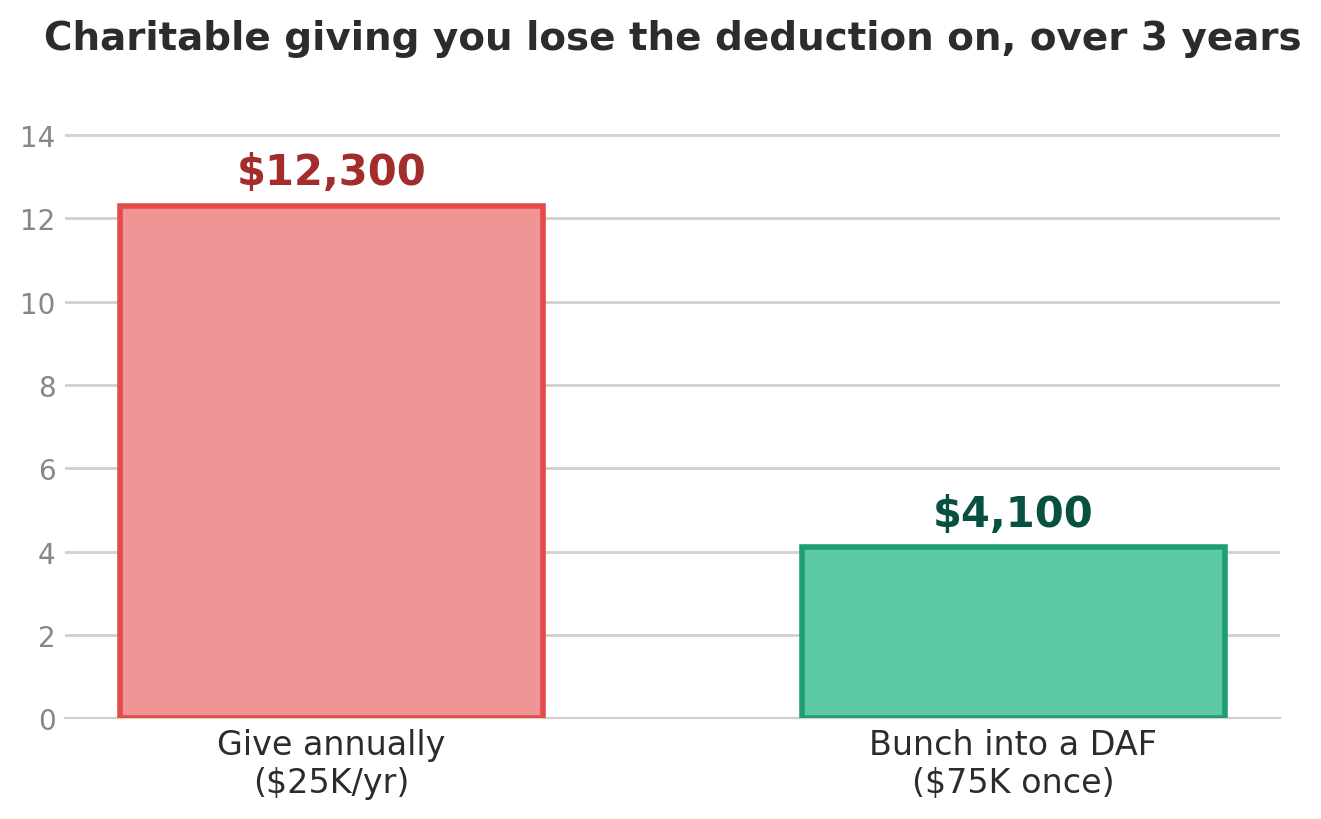

The other trap is timing. Most people give the same amount every year out of habit. Under the old rules that was fine. Under the 0.5% floor, giving steadily means you forfeit the deduction on 0.5% of your income every year, forever. Give $25,000 a year for three years and you've quietly thrown away the deduction on roughly $12,000 of giving across the cycle.

What You Can Do About It

You can't repeal the rules. But you can be deliberate about when and how you give. Three options, with the trade-offs:

- Bunch several years of giving into one, through a donor-advised fund (DAF). A DAF is a charitable account you fund in a lump sum, take the deduction now, and grant out to charities over the following years. If you bunch three years of giving — $75,000 — into a single 2026 contribution, you clear the 0.5% floor once instead of three times. That alone preserves the deduction on roughly $8,000 of giving versus spreading it out. Bunching also helps you leap over the $32,200 standard deduction in the year you give, so itemizing is actually worth it. Trade-off: your cash goes out the door now, and DAF grants can't fund things like raffle tickets or anything you get a benefit back from.

- Donate appreciated stock, not cash. This is the move most people miss, and in 2026 it matters more than ever. When you donate long-term appreciated shares — say, RSUs you've held more than a year, or old ESPP lots — you get the charitable deduction and you completely skip the capital-gains tax on the embedded gain. That capital-gains avoidance is not touched by the 35-cent cap. On $75,000 of stock with $50,000 of embedded gain, you sidestep about $11,900 in federal tax (the 23.8% top capital-gains rate, which includes the 3.8% Net Investment Income Tax that applies above $250,000 for joint filers). The deduction got worse this year — but giving stock instead of cash got relatively better, because the biggest benefit lives outside the new cap. If you're sitting on concentrated, appreciated company stock, this should be your default.

- Plan giving around your income, not the calendar. Every itemized dollar in a top-bracket year is worth only 35 cents. If you have a lighter income year coming — between vests, a sabbatical, a job change — that's often the better year to itemize large deductions, since the surtax only bites the portion of income taxed at 37%. The trade-off is patience: it only works if you have flexibility on timing.

For most equity-comp households, the highest-leverage combination is simple: fund a donor-advised fund with appreciated company stock, and bunch a few years of giving into it. You clear the 0.5% floor once, you dodge the capital-gains tax entirely, and you get the deduction in a year you can use it.

The Bottom Line

In 2026, a dollar of charitable deduction is worth 35 cents to a top-bracket earner, and the first 0.5% of your AGI in giving isn't deductible at all. Those two haircuts repeat every year and hit hardest in your biggest vest years. You can't change the rules — but by bunching your giving into a donor-advised fund and funding it with appreciated stock instead of cash, you keep the part of the benefit the new law never touched.

If any of this sounds like your situation — a big vest year, regular charitable giving, and a pile of appreciated company stock — we're happy to run your specific numbers. Start here →

This content is for educational purposes and does not constitute personalized financial or tax advice. Tax thresholds and rules cited reflect 2026 figures and may change.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)