Single-Trigger vs. Double-Trigger RSUs: Why SpaceX Employees and the Stripe/Figma Crowd Get Taxed Completely Differently

.png)

SpaceX goes public this Friday. And depending on how your RSUs were structured, the IPO either changes everything about your taxes — or it changed nothing, because you already paid years ago.

That's not a typo. Two employees, two different companies, the same job title, the same number of shares, can have completely opposite tax situations going into an IPO. The reason is one word buried in your grant documents: whether your RSUs are single-trigger or double-trigger. Most people have never been told which one they have. This week, that distinction is worth tens of thousands of dollars.

What "trigger" actually means

An RSU is taxed as ordinary income the moment it "settles" — the moment the shares are considered yours. A "trigger" is simply the condition that has to be met for that to happen.

Single-trigger RSUs have one condition: time. You hit your vesting date, the shares settle, and you owe ordinary income tax on their full fair-market value that year — whether or not you can actually sell them. At a private company, that's the catch. The shares are real, the tax bill is real, but there's no public market to sell into.

Double-trigger RSUs have two conditions, and both must be met before you owe a dime: (1) the time-based vesting, and (2) a liquidity event — usually an IPO or acquisition. You can hit your three-year vesting cliff at a private company and owe nothing, because the second trigger hasn't fired yet. The tax is deferred until the company goes public or gets bought.

Double-trigger is the standard for most venture-backed private companies precisely because it protects employees from getting taxed on shares they can't sell. Stripe, Figma, and Databricks use it. So does most of the 2025–26 IPO cohort — Chime, CoreWeave, Klarna, Navan. SpaceX is the notable outlier: it uses single-trigger RSUs that tax at vest.

Why this catches smart people off guard

Here's where it gets expensive, and it's not because anyone did anything wrong.

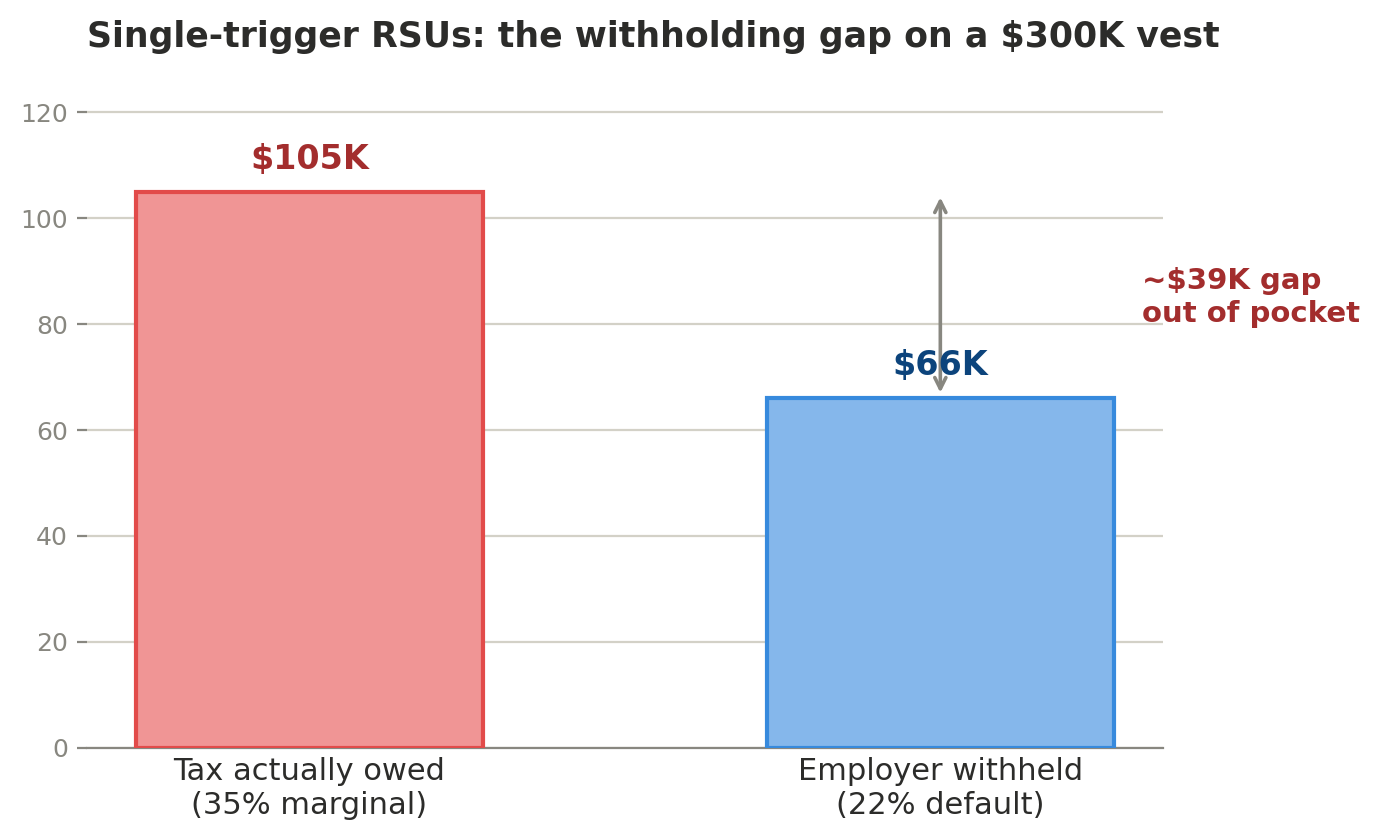

If you're a SpaceX engineer with single-trigger RSUs, you've potentially been paying ordinary income tax at every vest for years — on shares you couldn't touch. Say $300K vested last year at a 35% marginal rate. That's roughly $105K in tax owed on stock you couldn't sell to cover it. Your employer withheld the federal default of 22% — about $66K — leaving a gap of nearly $40K you had to cover out of pocket, from cash, because there was no market. Multiply that across several vesting years and you understand why single-trigger employees often feel the IPO is overdue, not exciting. The IPO isn't the tax event. It's finally the liquidity to match taxes you already paid.

If you're a double-trigger employee — Stripe, Figma, the rest — the IPO is the opposite. It's the moment the second trigger fires and a large slug of income lands all at once. Several years of vested-but-untaxed RSUs can settle in a single tax year, potentially stacking your income into the top 37% federal bracket, triggering the 3.8% Net Investment Income Tax (NIIT, the surtax that applies to investment income above $250K for married filers), and blowing well past the $1M mark where supplemental withholding jumps from 22% to 37%. And you usually can't sell during the post-IPO lockup (typically 90–180 days) to manage any of it.

The conflation of these two structures is the single most common equity-comp mistake I see going into an IPO. People read a generic "what an IPO means for your RSUs" article that describes double-trigger mechanics, assume it applies to them, and plan for the wrong tax year entirely.

What you can do about it

Your move depends entirely on which structure you have — so step one is to actually find out. Pull your grant agreement and look for the words "single-trigger" or "double-trigger" (sometimes "liquidity-based vesting condition").

If you have single-trigger RSUs (SpaceX):

- Reconcile what you've already paid. You've likely been carrying a withholding gap for years. Confirm the 22% withheld against your real marginal rate so you know whether you've been underpaying — and whether you owe an estimated-tax true-up.

- Treat the IPO as a diversification event, not an income event. The income already happened. The real question is how fast you trim a position that may be 70%+ of your net worth, and which lots to sell to control the capital-gains tax on any post-vest appreciation.

- Use specific-lot identification when you sell so you're realizing the gains you choose, not whatever your broker defaults to.

If you have double-trigger RSUs (Stripe, Figma, Databricks, and the IPO cohort):

- Plan for the income spike in the year the second trigger fires. Model whether a multi-year stack of RSUs pushes you into the 37% bracket and over the NIIT and $1M supplemental-withholding thresholds.

- Assume the 22% withholding is not enough. On income over $1M the right supplemental rate is 37%; the gap on a large settlement can be six figures. Set aside cash or make a quarterly estimated payment so April isn't a disaster.

- Map the lockup before you plan any sales. You generally can't sell for 90–180 days post-IPO, so your tax bill can be due before you have liquidity. Plan the cash for it now.

The thread running through both lists: the tax, the withholding, the estimated payments, and the diversification decision are not separate problems. They're one problem viewed from four angles. The employees who come through an IPO clean are the ones who had all four coordinated before the stock started trading — not the ones who called a CPA in April.

The Bottom Line

Single-trigger means you were taxed at vest, on illiquid shares, and the IPO is your first real liquidity. Double-trigger means the IPO is your tax event, often a big one, usually behind a lockup. Same job, same shares — opposite playbooks. Before Friday, find out which one you have. It changes everything else you do.

If you're heading into the SpaceX IPO — or any of the 2025–26 listings — and you're not sure which RSU structure you have or what it means for your tax year, we're happy to walk through your specific grant and build the plan around it. Start here →

This content is for educational purposes and does not constitute personalized financial or tax advice. Tax rules and thresholds referenced are based on 2026 figures and individual situations vary.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)