Sell-to-Cover Isn't Enough: The RSU Withholding Gap, and How to Close It Before April

Your RSUs vested, payroll sold a chunk of shares to "cover taxes," and you assumed the bill was handled. For most high earners in tech, it wasn't. There's a gap between what your employer withheld and what you actually owe — and it shows up as a five-figure surprise next April.

Here's the part nobody tells you at your first big vest: your company almost certainly under-withheld, on purpose, by following a rule that was never designed for your income.

What's Actually Happening

When your RSUs vest, the full fair-market value of those shares hits your W-2 as ordinary income that day. Not when you sell — at vest. If you vest $300,000 worth of NVIDIA stock, you have $300,000 of ordinary income, exactly as if it were salary.

Your employer is required to withhold federal tax on that income. The problem is the rate they use. RSU income counts as a "supplemental wage," and the default federal withholding rate on supplemental wages is 22% (it jumps to 37% only on amounts above $1 million from a single employer in one year). That 22% is a flat, one-size-fits-all number the IRS set for everyone from a $60K earner to a $600K earner.

If you're a senior engineer earning well into the six figures, your actual marginal tax rate isn't 22%. It's 32%, 35%, or 37%. So every dollar of RSU income gets taxed at your real rate in April, but only 22 cents on the dollar got withheld at vest. The difference is the withholding gap.

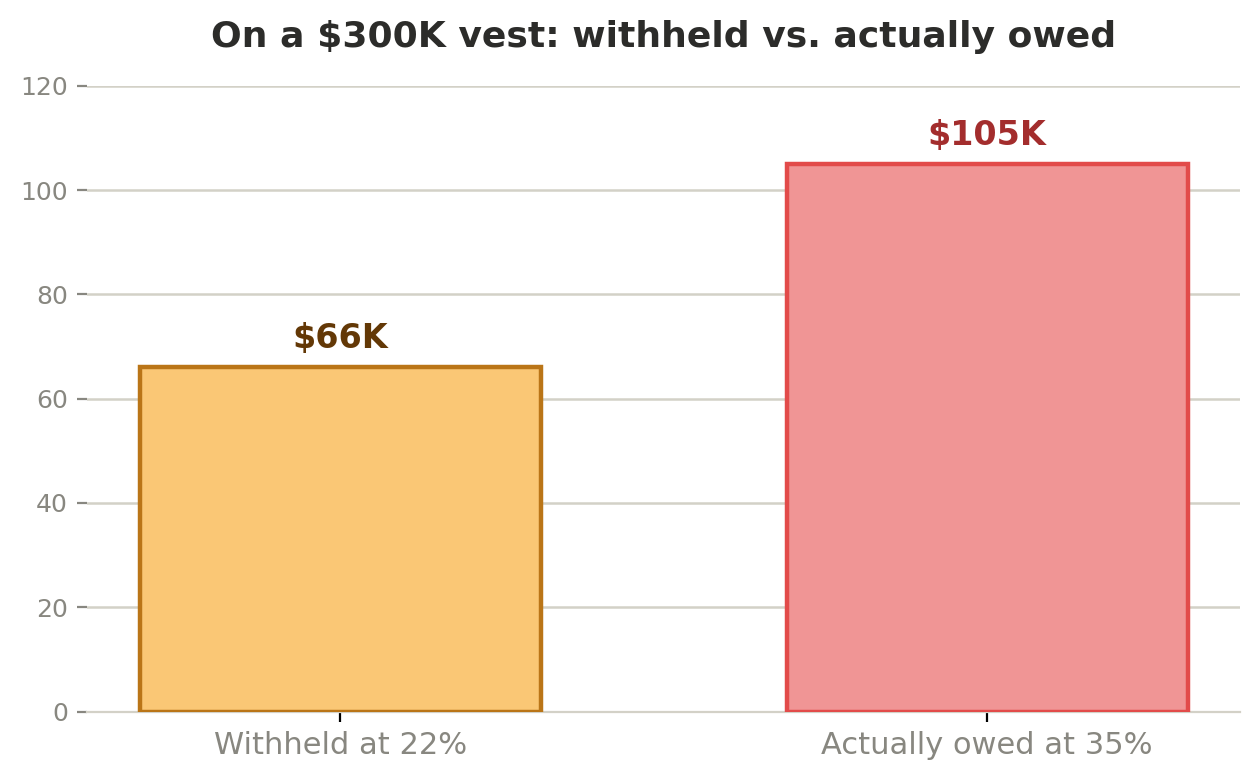

Let's walk the math on a $300,000 vest for a senior engineer whose income puts them in the 35% federal bracket:

- Tax actually owed on the vest: $300,000 × 35% = $105,000

- Tax withheld by payroll at 22%: $300,000 × 22% = $66,000

- The gap you owe in April: $39,000

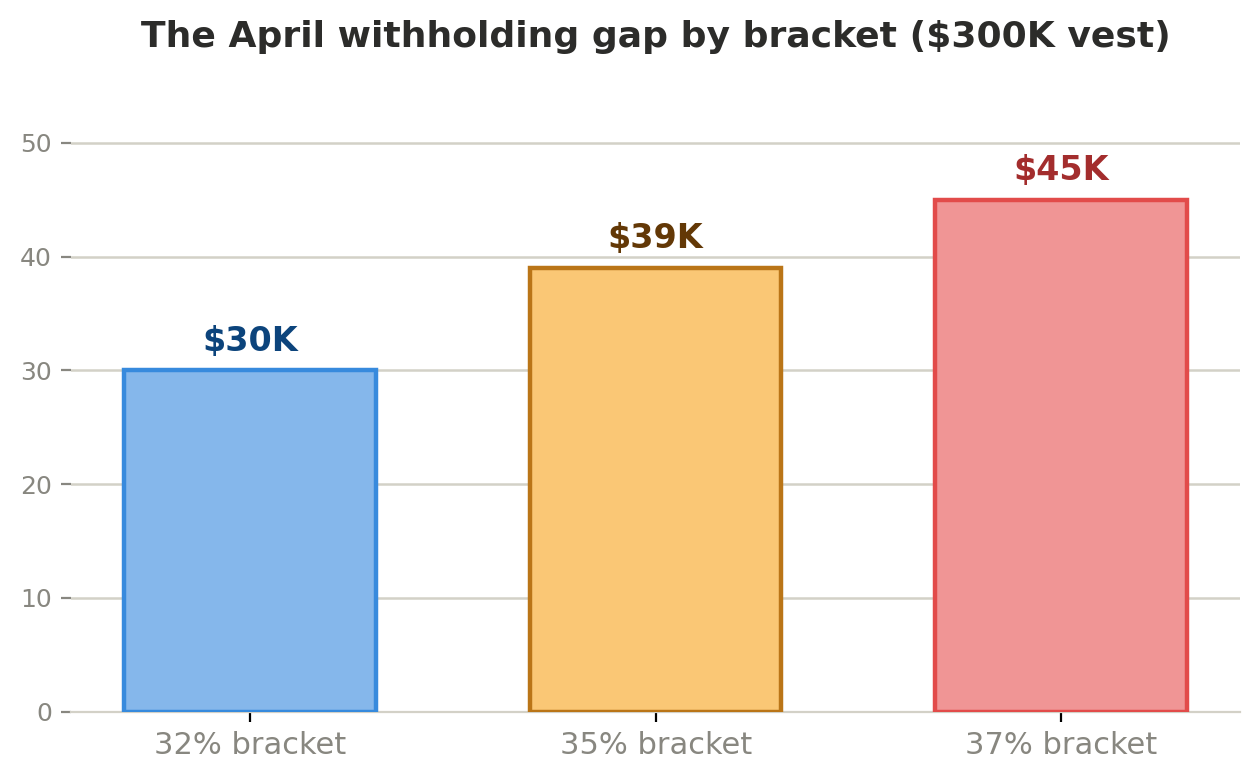

At the 32% bracket the gap on that same vest is about $30,000. At the top 37% bracket it's roughly $45,000. And that's federal only — if you're in California, Oregon, or New York, your state income tax widens the hole by tens of thousands more, because state withholding on supplemental wages is often set low too.

Sell-to-cover doesn't fix this. Sell-to-cover just means payroll sold enough shares to fund that 22% withholding. It funds the wrong number. The shares got sold; the gap is still there.

Why This Catches People

Almost everyone I talk to about this says the same thing: "I figured my employer handled it."

That's a reasonable assumption. Withholding on your salary is usually pretty accurate, so it's natural to assume RSU withholding works the same way. It doesn't. Payroll isn't being careless — they're following the 22% supplemental rule to the letter. The rule just wasn't built for people whose marginal rate is 13 to 15 points higher than the flat withholding rate.

This bites hardest in two situations. The first is your first big vest — a new grad cliff, a refresher stacking on top of your initial grant, or a promotion that pushed your total comp up a bracket. You've never seen a vest this size, so you've never seen a gap this size. The second is any year your comp jumped: a level bump, a market-rate adjustment, or a stock that ran up between grant and vest. Your withholding is still calibrated to last year's smaller number while your tax bill is calibrated to this year's bigger one.

There's a nastier version too. Say you sold-to-cover and then held the rest, and the stock dropped afterward. You might think a lower stock price lowers your tax. It doesn't. Your ordinary income was locked in at the fair-market value on the vest date. If NVIDIA was at $300K of value when it vested and fell to $220K by December, you still owe ordinary income tax on the full $300K. The drop becomes a capital loss on shares you held — a separate event that doesn't erase the income you already booked.

What You Can Do About It

The good news: it's July. This is the last clean window to close the gap before it becomes a penalty. You have real options, and they're choices with trade-offs — not a single mandate.

- Bump your W-4 withholding for the rest of the year. Use the "extra withholding" line (Step 4c) on Form W-4 to pull more from every remaining paycheck. The advantage: withholding is treated by the IRS as if it were paid evenly across the whole year, even if you add it all in Q4. That can retroactively cure an underpayment the estimated-payment route can't. The trade-off: it comes out of your salary cash flow.

- Make a quarterly estimated payment. Calculate the shortfall and send it to the IRS directly via Form 1040-ES. The next deadline is September 15, 2026, with a final one January 15, 2027. This is the cleaner path if you'd rather not touch your paycheck. The trade-off: estimated payments are credited when you make them, not spread evenly, so timing matters more.

- Aim for a safe harbor instead of the exact number. You don't actually have to nail your final tax to the dollar to avoid an underpayment penalty. You're protected if your total withholding and estimated payments hit either 90% of what you'll owe this year, or 110% of your total tax from last year (the 110% figure applies because your prior-year AGI is over $150,000; below that it's 100%). Hitting a safe harbor is usually the smarter target — it's a fixed, knowable number, and it means you can still owe a balance in April without owing a penalty on top of it.

- Do nothing — but do it on purpose. If you have the cash to write a big check in April and you'd rather hold onto it until then, that's a legitimate choice. Owing tax isn't a penalty. But make sure you've cleared a safe harbor, or the IRS adds an underpayment penalty to the bill.

The Bottom Line

Sell-to-cover funds 22%. Your real rate is probably 32% to 37%. That difference is the withholding gap, and on a $300,000 vest it runs $30,000 to $45,000 in federal tax alone — before your state takes its cut. Your employer didn't make a mistake; the flat 22% rule just wasn't built for your income. The fix is straightforward once you know the number, and July is the last quiet month to handle it before the Q3 deadline.

If any of this sounds familiar — a big vest this year, a comp jump, or just a nagging feeling that 22% wasn't enough — we're happy to run your actual numbers and map out which of these moves fits your situation. Start here → alphanso.ai/start

This content is for educational purposes and does not constitute personalized financial or tax advice. Tax figures reflect 2026 federal rules; your situation, state, and bracket will change the math.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)