The RSU Withholding Gap: Why 22% Is Almost Never Enough in 2026

By Rupesh Goyal, CFA Boston Chapter | Updated March 2026

Every April, thousands of tech employees open their tax software and see a number they weren't expecting. Not because they did anything wrong, but because of a structural mismatch built into how RSU income is withheld. If your company withholds 22% on your RSU vest and you're in the 37% federal bracket, the gap between those two numbers is your April surprise. For a $200,000 vest, that's $30,000 owed to the IRS with no warning until filing day.

How RSU Withholding Actually Works

When your RSUs vest, your employer is required to withhold taxes on the value of the shares at that moment. The IRS classifies RSU income as "supplemental wages," withheld at a flat rate of 22% federal (or 37% on amounts over $1 million in a single year).

That 22% sounds reasonable until you look at your actual marginal bracket. A senior FAANG engineer earning $350,000 in base salary is already in the 37% federal bracket before a single RSU vests. Your effective rate on additional income is 37%, not 22%.

Add state income tax. In California, that's another 13.3%. In New York, 10.9%. When your employer withholds 22% federal on a $150,000 RSU vest and your actual liability is closer to 50%, you're looking at a $42,000+ shortfall from that one vest alone.

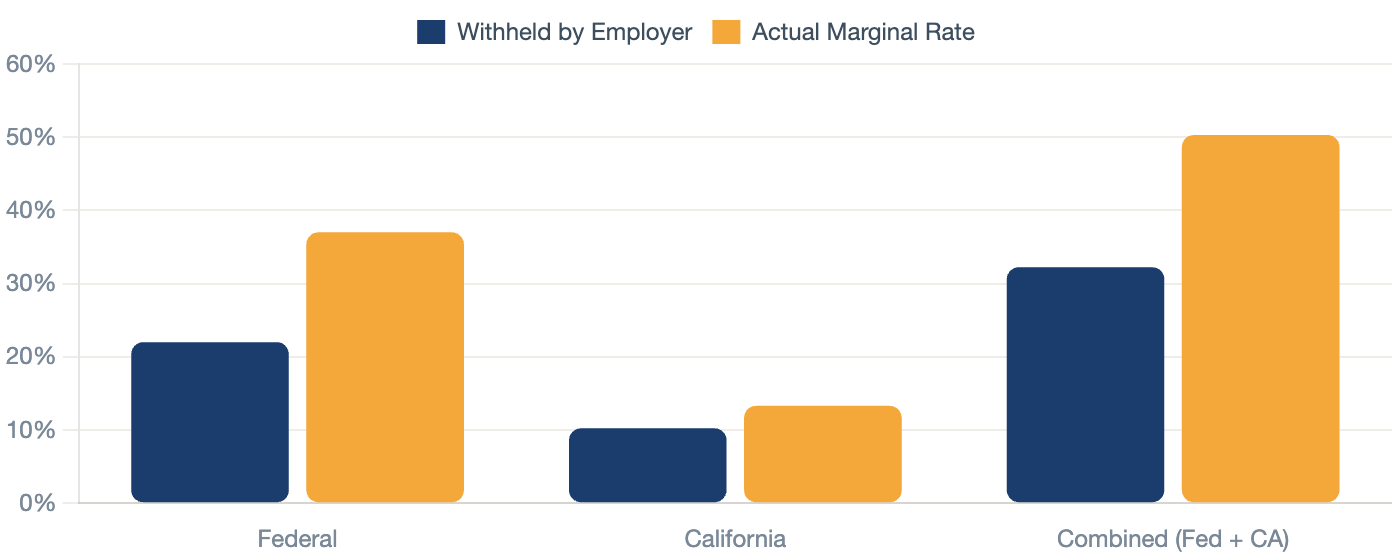

The Math on a Real Example

Here's how this plays out for a typical profile:

- Role: L6 Software Engineer, Google

- Base salary: $280,000

- RSU vests in 2025: $180,000 across four tranches

- Filing status: Married, filing jointly

- State: California

Federal: 22% withheld vs. 37% actual marginal rate, a gap of 15 cents per dollar.

California: 10.23% withheld vs. 13.3% actual, a gap of 3 cents per dollar.

On $180,000 in RSU income, the federal gap alone is $27,000. Add California and you're at $32,400 owed in April, with underpayment penalties if quarterly estimates weren't made during the year. This isn't a bug in the tax code. The supplemental withholding rate exists because employers don't always have full visibility into your marginal bracket. But the burden of getting it right falls on you, and most employees don't know there's a problem until they file.

What Your Options Actually Look Like

You have a few levers here. Each has trade-offs, and the right combination depends on your income, timing, and how much cash you have available.

- Adjust your W-4 to withhold more from your salary. You can instruct your employer to withhold additional federal tax each pay period. Lowest friction, no quarterly deadlines. The downside: you're reducing take-home pay throughout the year and giving the IRS an interest-free loan.

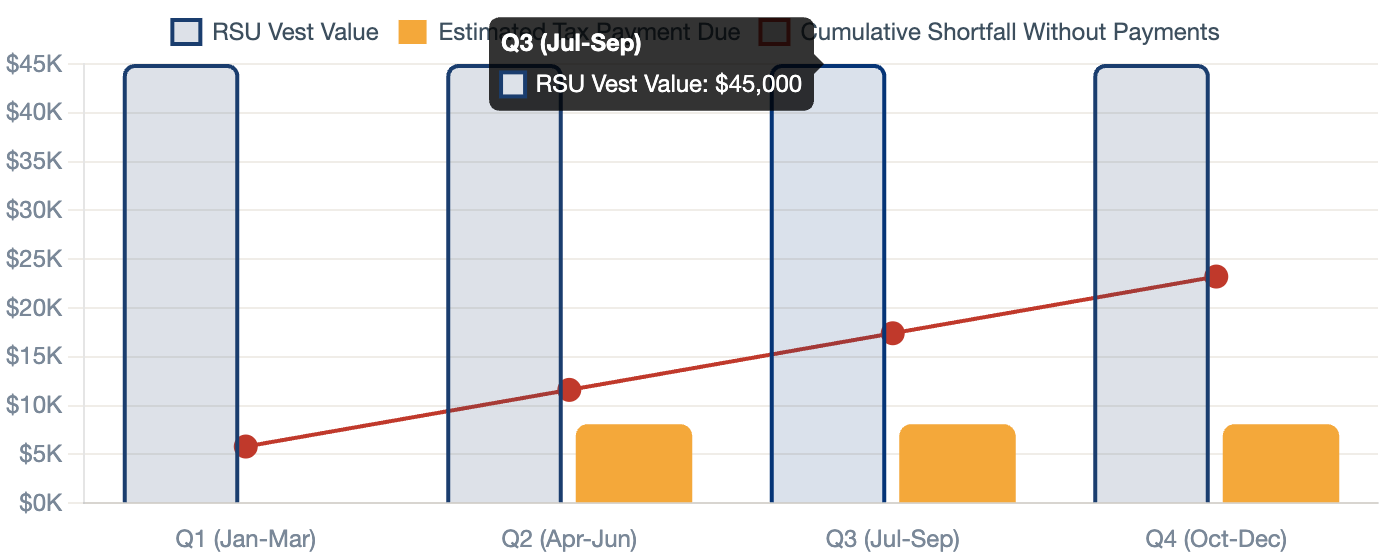

- Make quarterly estimated tax payments. The IRS expects high earners to pay as they go. Underpayment penalties apply if you don't pay at least 90% of your current-year liability (or 100% of last year's tax, 110% if your prior AGI exceeded $150K). Payments are due April 15, June 16, September 15, and January 15.

- Sell RSUs at vest and set aside the full tax liability. Some employees sell a portion immediately and park the proceeds in a money market or T-bill until filing time. Clean and explicit, though it means recognizing income on the sale date.

- Review your ESPP cost basis. The second-most-common source of surprise tax bills for tech employees. Many brokerages list only the purchase price as cost basis on your 1099-B, ignoring the discount already taxed on your W-2. Without an adjustment, you pay tax on the same income twice.

Still Time: The Backdoor Roth Window

If you haven't maxed your retirement contributions for 2025, the window is open until April 15. A few moves still available:

- Backdoor Roth IRA: No income cap on conversions. Contribute to a non-deductible traditional IRA, then convert. 2025 limit: $7,000 ($8,000 if 50+).

- HSA: If you're on a high-deductible health plan, you can still contribute for 2025 until April 15.

- OBBBA catch-up: If you're 60-63, you're eligible for an enhanced 401k catch-up of $11,250 this year.

These don't erase the RSU gap, but they reduce your taxable income before the window closes on the same day your return is due.

When It Makes Sense to Work with an Advisor

For most tech employees, the RSU withholding gap resets every year. Variables shift: different vest schedules, bonus timing, stock price at vest, state residency changes, life events. At some point, tracking this yourself costs more than it saves, not from a single bad decision, but from the cumulative hours calculating, second-guessing, and still being unsure you got it right.

Alphanso's advisors model your annual tax picture in January, before the first vest hits. They calculate your estimated payment schedule, flag ESPP cost basis issues, and update the plan when something changes. You make the calls; they handle the complexity.

Flat fee: $2,400/year. No asset transfer required. No AUM fee that compounds with your portfolio. Start a 14-day free trial, no commitment, no account transfers, just a clear picture of where you stand.

Frequently Asked Questions

Why does my employer only withhold 22% on my RSUs?

The IRS mandates supplemental wage withholding at a flat 22% rate. It doesn't adjust for your actual marginal bracket. Closing the gap is your responsibility through W-4 adjustments or quarterly estimated payments.

Will I face a penalty if I underpay?

Possibly. The IRS charges roughly 8% annualized on underpayment if you don't meet the 90%/100% safe harbor thresholds. Large vest tranches can create a meaningful gap quickly.

Can I change my withholding mid-year?

Yes. Submit a new W-4 to your employer at any time; changes typically take effect within a pay cycle. If your vest schedule is uneven, you can raise withholding in heavy-vest months and lower it afterward.

What's the ESPP cost basis issue?

Your brokerage may list only your purchase price as cost basis on the 1099-B, ignoring the discount already taxed as ordinary income on your W-2. Without adjusting for this, you pay tax on the same income twice.

Is a backdoor Roth still an option for me?

Likely yes, if you have earned income. The contribution window for 2025 closes April 15, 2026. There's no income cap on Roth conversions, only on direct contributions.

Does Alphanso require me to move my accounts?

No. You keep everything at your existing brokerage. Alphanso advises at the planning layer; you execute at your own custodian.

How is Alphanso different from a traditional financial advisor?

Most AUM advisors charge 1% of assets under management, a fee that grows as your equity does regardless of planning complexity. Alphanso charges a flat $2,400/year and is a registered fiduciary, legally required to act in your interest.

Alphanso Wealth Management is a registered investment advisor. This article is for educational purposes and does not constitute personalized investment or tax advice. Consult a tax professional regarding your specific situation.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)