The Mega Backdoor Roth: How to Put $72,000 Into Tax-Free Retirement Accounts in 2026

Most tech workers max out their 401(k) at $24,500 and assume they've exhausted their tax-advantaged retirement space. They haven't. If your employer's plan allows after-tax contributions — and most large tech companies' plans do — you may have access to an additional $36,000–$47,500 of space that converts to tax-free Roth dollars. This is the Mega Backdoor Roth, and it's one of the most underused strategies in equity compensation planning.

How the Math Actually Works

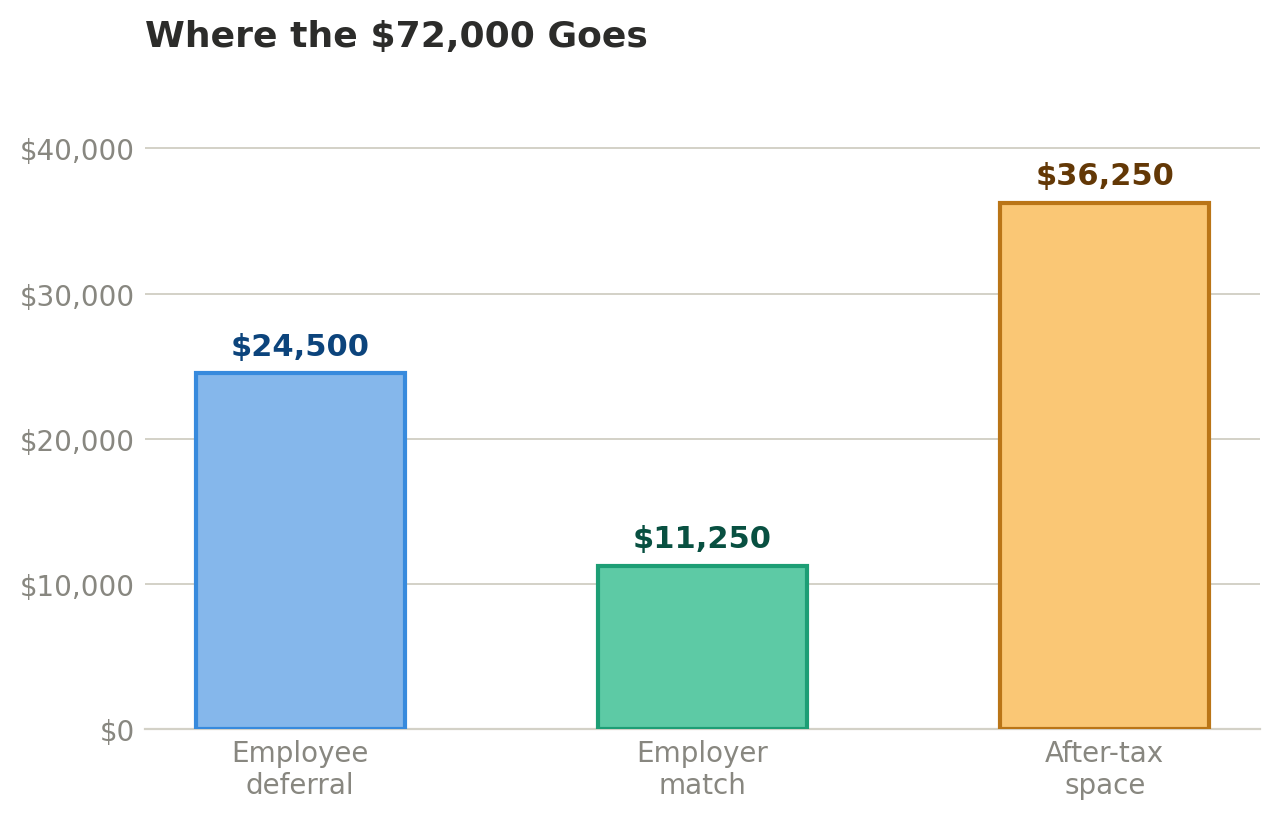

The IRS sets a total contribution limit for all money flowing into your 401(k) each year. For 2026, that limit is $72,000 under Section 415(c). If you're 50 or older, add another $7,500.

Here's how that $72,000 breaks down:

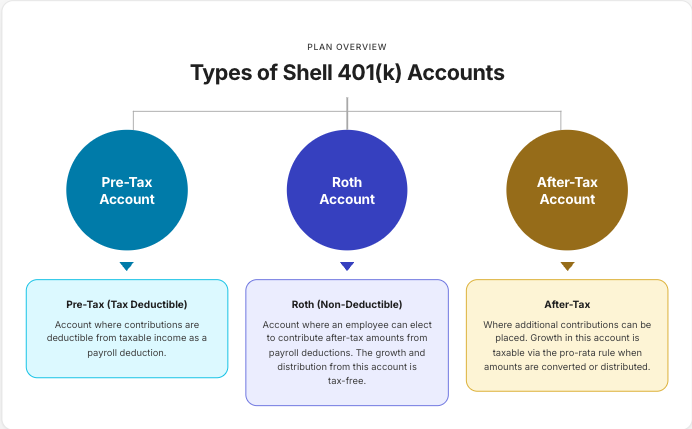

Your employee deferral — the Roth or pre-tax 401(k) contribution you elect from your paycheck — is capped at $24,500. That's the number most people know. Then your employer match fills in more. Let's say you're a senior engineer at Google earning $250,000 in base salary, and Google matches 50% of your contributions up to a certain cap. That adds roughly $11,250.

So you've used $35,750 of your $72,000 limit. Where does the rest go?

The remaining $36,250 is your after-tax contribution space. If your plan allows it — and Google's does, as do Meta's, Microsoft's, Amazon's, Dell's, and Snowflake's plans — you can contribute after-tax dollars up to the $72,000 ceiling. Then, and this is the key step, you convert those after-tax dollars to Roth either through an in-plan Roth conversion or a rollover to a Roth IRA.

The result: $72,000 of total contributions, with roughly $60,750 ending up in Roth accounts (your $24,500 Roth deferral plus the $36,250 after-tax conversion). All of it grows tax-free. Forever.

Why This Catches Smart People Off Guard

Three reasons.

First, it's not obvious in your benefits portal. The after-tax contribution option — if your plan offers it — is usually buried in the enrollment settings, often listed separately from your Roth or pre-tax election. Most people never scroll down to it because they assume the $24,500 deferral is the whole story.

Second, the conversion step isn't automatic at every company. Some plans offer automatic in-plan Roth conversions (sometimes called "auto-sweep"), which convert your after-tax balance to Roth daily or weekly. Others require you to manually initiate the rollover. If you contribute after-tax dollars but never convert them, the growth on those dollars is taxable — which defeats the purpose. The timing matters: convert the same week the after-tax contribution lands. Waiting a year means any growth on the balance becomes taxable at conversion.

Third, the name is misleading. "Mega Backdoor Roth" sounds like a tax loophole or a gray-area maneuver. It isn't. It's a completely legitimate use of after-tax 401(k) contributions followed by a Roth conversion, both of which are explicitly allowed under the tax code. But the name makes people assume it's too good to be true, so they never look into it.

A Concrete Example: What This Looks Like Over 6 Years

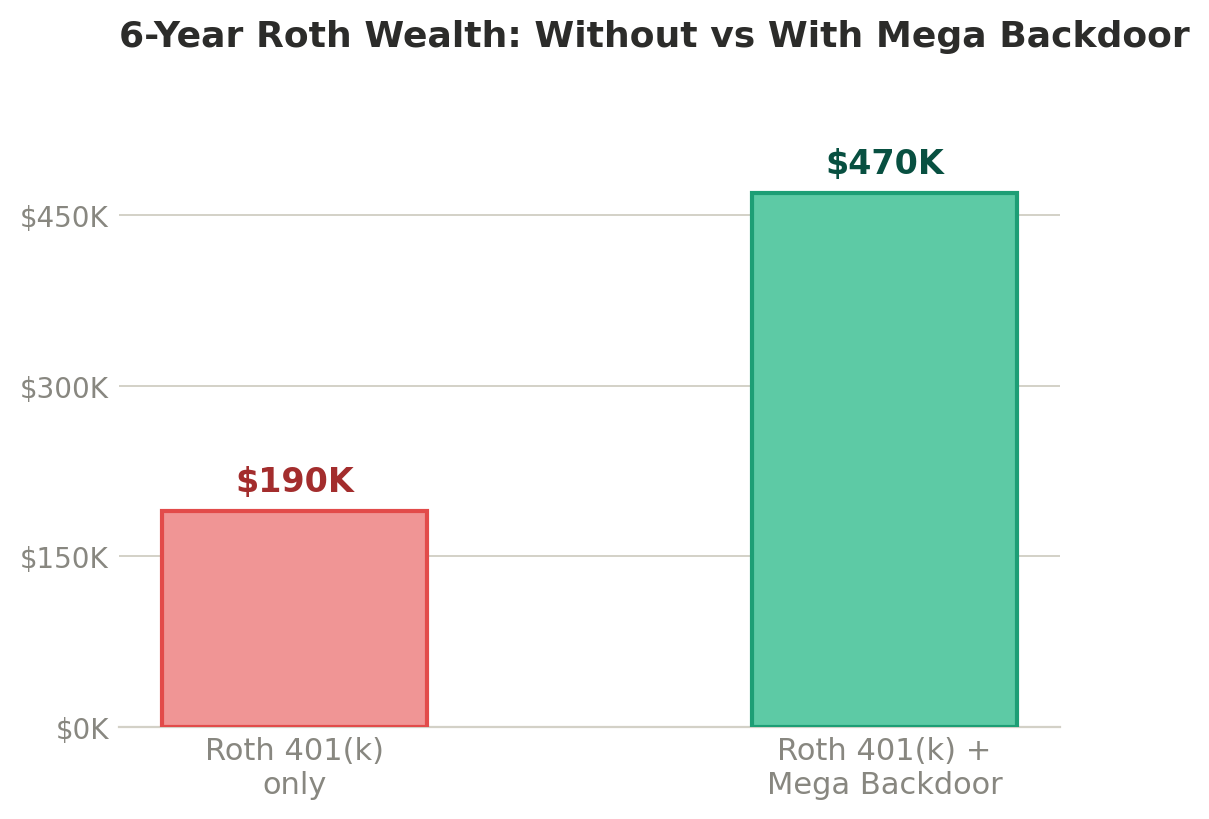

Let's say you're a Level 5 software engineer at Microsoft earning $220,000 in base salary with $180,000 in RSUs. You've been maxing out your Roth 401(k) at $24,500 per year but doing nothing with the remaining after-tax space.

If you start contributing an additional $36,250 per year in after-tax dollars and convert them to Roth immediately, here's what happens assuming an average 8% annual return:

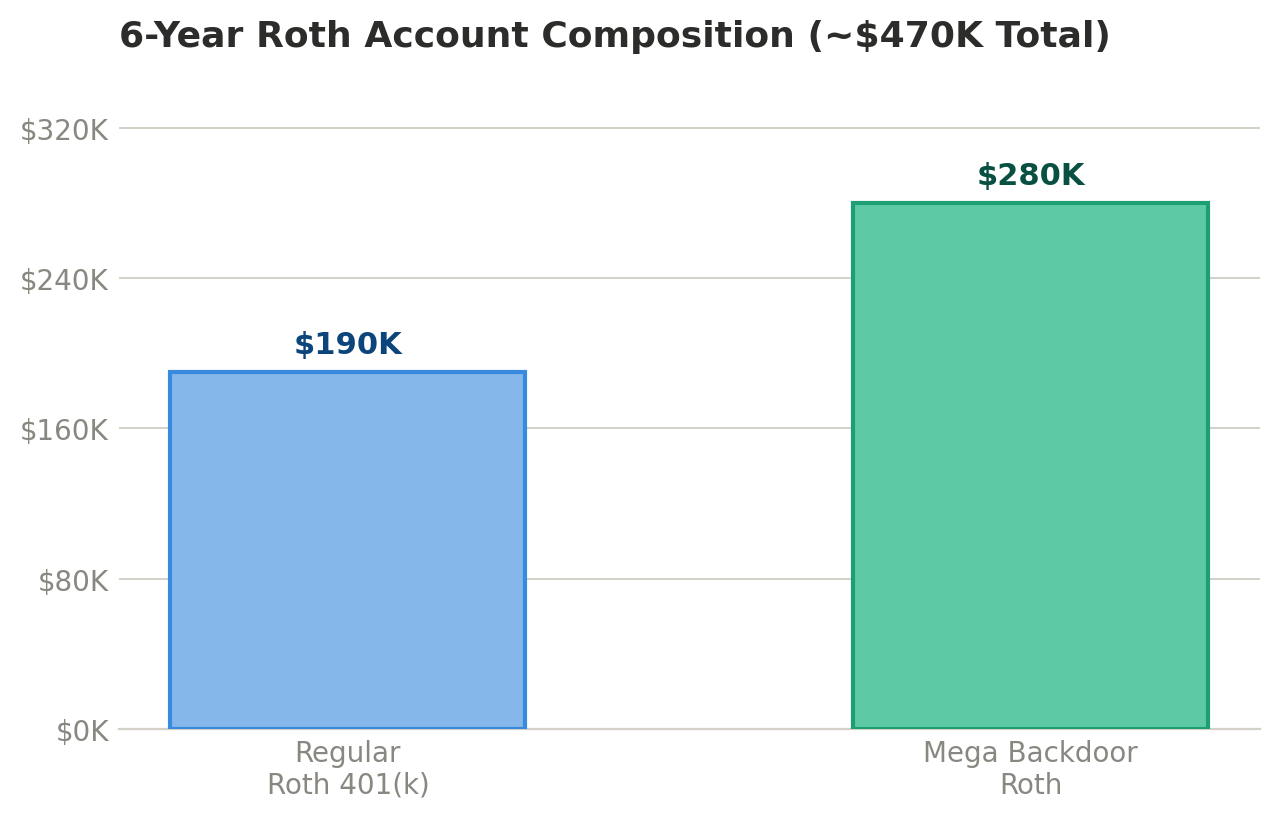

After 6 years, your Mega Backdoor Roth contributions alone total $217,500. With compounding, that balance grows to roughly $280,000. Combined with your regular Roth 401(k) contributions ($147,000 in deferrals, growing to approximately $190,000), you're sitting on roughly $470,000 in Roth accounts — all of which grows and can be withdrawn tax-free in retirement.

A tech worker recently profiled by 24/7 Wall Street built $750,000 in Roth wealth in six years using this exact approach. The math is real.

What You Should Check — Today

Step 1: Log into your 401(k) provider (Fidelity, Vanguard, Schwab — wherever your plan is). Look for "after-tax contributions" in your contribution settings. If the option exists, your plan allows it. If it doesn't appear, call your benefits team to confirm.

Step 2: Check whether your plan offers automatic in-plan Roth conversions. If it does, enable the auto-sweep. If it doesn't, set a calendar reminder to manually initiate a rollover within a week of each after-tax contribution.

Step 3: Calculate your available space. Take $72,000, subtract your employee deferral ($24,500), subtract your employer match (check your benefits statement), and the remainder is your after-tax ceiling.

Step 4: Make sure you're not over-contributing. If your employer match plus your deferrals plus after-tax contributions exceed $72,000, the excess creates a tax mess. An advisor can help you model this precisely.

The Bottom Line

The $24,500 Roth 401(k) limit is the beginning of your tax-free retirement strategy, not the end. If you work at a large tech company, there's a good chance you have access to an additional $36,000–$47,500 of annual Roth conversion space that you're not using. Over a career, that gap compounds into hundreds of thousands of dollars of tax-free wealth you left on the table.

The Mega Backdoor Roth isn't complicated. It's just invisible until someone points it out.

If you want help figuring out whether your plan supports this and how much space you have, we're happy to walk through the math with you. Book a conversation →

This content is for educational purposes and does not constitute personalized financial or tax advice. Contribution limits are based on 2026 IRS guidelines and may change. All investing involves risk, including the possible loss of principal. Alphanso LLC is a registered investment adviser.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)