Financial Planning for Google Employees: RSUs, GSUs & Beyond (2026)

You've worked hard to land a role at Google - and now your compensation package includes base salary, bonuses, and a stream of Google Stock Units (GSUs) that vest on a schedule you probably had to read three times to understand. The financial upside is real. But so is the complexity: overlapping vesting schedules, a withholding gap that surprises people every April, concentration risk that builds quietly, and a benefits ecosystem that rewards you more the better you understand it.

This guide breaks down exactly how Google's equity compensation works, where the planning gets tricky, and what your options look like at each decision point.

How Google Stock Units (GSUs) Actually Work

Google's RSUs are called GSUs - Google Stock Units - and each unit equals one share of Alphabet (GOOGL) stock. When your GSUs vest, you receive actual shares, and the fair market value on that date counts as ordinary income on your W-2.

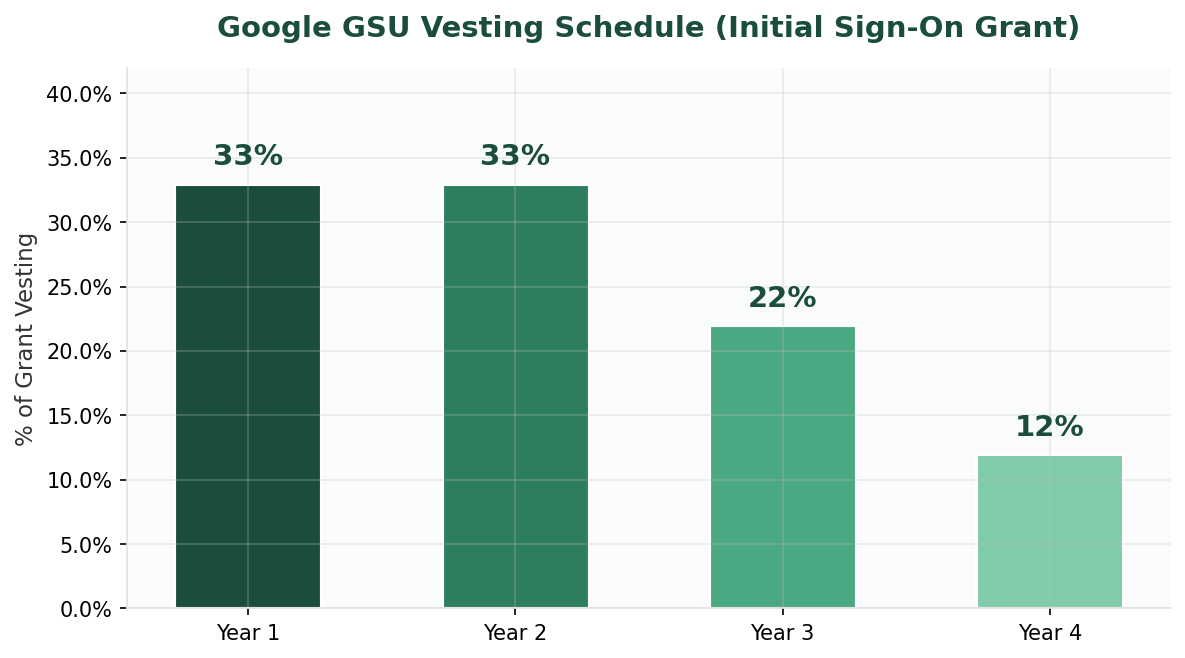

Here's what catches people off guard: the vesting schedule is front-loaded. For initial sign-on grants, the standard structure is 33% in year one, 33% in year two, 22% in year three, and 12% in year four. That means your biggest vesting events happen early, when you may not yet have a plan in place for the tax hit.

On top of your initial grant, Google issues annual refresher grants that typically vest evenly - 25% per year over four years. After your second or third year at Google, you'll likely have multiple overlapping vesting schedules running simultaneously, which can make any single quarter's vesting amount surprisingly large.

Vesting frequency also depends on your grant size: employees with fewer than 32 GSUs vesting annually receive shares semi-annually, 32-63 GSUs vest semi-annually, 64-159 quarterly, and 160+ monthly. Most mid-to-senior engineers and managers land in the quarterly or monthly bucket.

Practical takeaway: Pull up your Schwab equity account and map out your vesting schedule for the next 12 months. Knowing exactly when and how much is vesting lets you plan your tax payments and selling strategy ahead of time rather than reacting after the fact.

The Withholding Gap: Why Your Tax Bill Might Be Higher Than You Expect

This is the single most common financial surprise for Google employees, and it's entirely structural - not a mistake on your part.

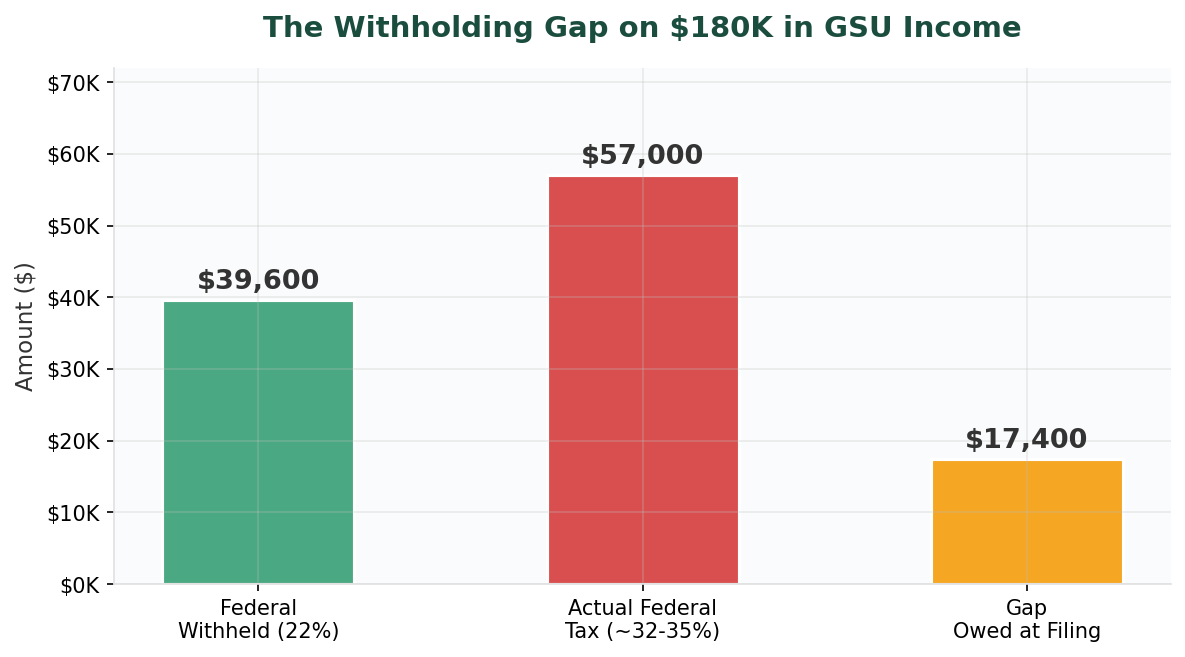

When your GSUs vest, Google withholds federal taxes at the flat supplemental rate of 22%. If your vesting exceeds $1 million in a calendar year, the rate bumps to 37% on the excess. But here's the problem: if your total income (base salary + bonus + vested GSUs) puts you in the 32%, 35%, or 37% marginal bracket, that 22% withholding doesn't come close to covering your actual tax liability.

A quick example: Say you earn $220,000 in base salary and $180,000 in GSUs vest during the year. Your total income is $400,000, which puts a single filer in the 35% federal bracket on a portion of that income. Google withheld 22% on those GSUs - roughly $39,600. But your actual federal tax on that RSU income, at your marginal rate, could be closer to $54,000-$63,000. That's a gap of $15,000-$23,000 you'll owe when you file.

Add California income tax (up to 13.3% with no special treatment for supplemental wages) or other high-tax states, and the gap widens further.

What most Google employees in this situation consider: First, quarterly estimated tax payments (Form 1040-ES) - calculate your expected shortfall and pay it quarterly to the IRS to avoid underpayment penalties. Second, adjusting W-4 withholding - increase your regular paycheck withholding to compensate for the GSU gap, which is often simpler than quarterly estimates. Third, setting aside a cash reserve - some employees earmark 10-15% of each vesting event in a high-yield savings account specifically for the tax bill.

Concentration Risk: When Alphabet Becomes Too Much of Your Portfolio

After a few years at Google with initial grants, refreshers, and maybe an ESPP purchase or two, it's common to look at your portfolio and realize 40%, 50%, or even 70% of your net worth is in a single stock. That's not inherently wrong - Alphabet has been a phenomenal performer - but it does mean your financial future is disproportionately tied to one company's stock price.

The question isn't whether Google is a good company. It's whether you'd choose to invest that percentage of your savings into any single stock if you were starting from cash today. For most people, the honest answer is no.

How Google employees typically think about the sell/hold decision: The sell-at-vest approach means selling 50-100% of shares immediately when they vest, treating GSUs as cash compensation and removing concentration risk entirely. The threshold-based approach means setting a target - say, "I'll keep no more than 15% of my portfolio in Alphabet" - and selling shares whenever vesting pushes you above that threshold. Gradual diversification means selling a fixed percentage (e.g., 25-50%) at each vest, reducing concentration over time while maintaining some upside exposure.

None of these is the "right" answer. The right answer depends on your overall net worth, your other income sources, your risk tolerance, your time horizon, and whether you'd lose sleep if GOOGL dropped 30% in a quarter (as it has before).

Practical takeaway: Calculate your current Alphabet concentration as a percentage of your total investable assets. If the number surprises you, that's useful information. A target between 5-15% of total portfolio is where most diversified investors feel comfortable, but your number is yours to choose.

Maximizing Google's Benefits Beyond Equity

Google's benefits package extends well beyond GSUs, and some of the most valuable planning opportunities are the ones people overlook.

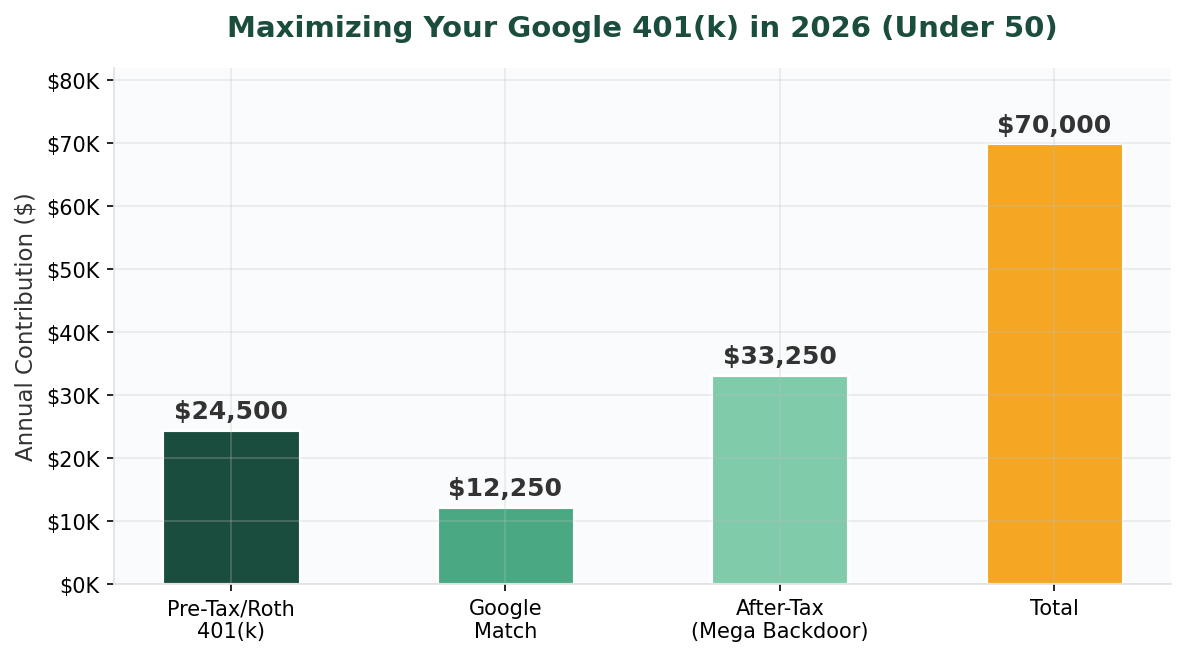

401(k) with employer match: Google offers a dollar-for-dollar match up to $3,000, or a 50% match up to the IRS maximum ($24,500 in 2026 for employees under 50). The 50% match path gives you up to $12,250 in free money - but only if you're contributing enough to capture the full match. At a minimum, contribute enough to max the match. Ideally, max the full $24,500.

Mega Backdoor Roth: Google's 401(k) plan allows after-tax contributions with in-plan Roth conversions - the so-called Mega Backdoor Roth. In 2026, the total 401(k) contribution limit (employee + employer + after-tax) is $70,000 for those under 50. After your pre-tax or Roth contributions and Google's match, you could potentially contribute an additional $33,000+ in after-tax dollars and immediately convert them to Roth. Over a career, this can build a significant tax-free retirement balance.

ESPP (Employee Stock Purchase Plan): Google's ESPP lets you buy Alphabet stock at a discount through payroll deductions. The typical structure offers a 15% discount with a lookback provision. For employees who plan to sell immediately after purchase, this is essentially a guaranteed return on the discount - one of the few "free lunch" opportunities in personal finance.

Practical takeaway: If you're not yet maxing your 401(k) and taking advantage of the Mega Backdoor Roth, run the numbers. For a Google employee in a high tax bracket, the long-term tax savings from maximizing these accounts can be worth hundreds of thousands of dollars over a career.

Tax-Smart Strategies for Google Equity Compensation

Managing taxes on Google equity isn't about avoidance - it's about timing and structure. Here are the strategies most relevant to Google employees.

First, tax-loss harvesting in your brokerage account. If you've diversified out of Alphabet into a broad portfolio, harvest losses in down markets to offset gains from GSU sales. This doesn't change your investment exposure (you can buy a similar-but-not-identical fund) but reduces your current-year tax bill.

Second, charitable giving with appreciated shares. If you're charitably inclined, donating appreciated Alphabet shares (held longer than one year) to a donor-advised fund lets you deduct the full market value while avoiding capital gains tax entirely. This is significantly more tax-efficient than donating cash.

Third, Roth conversion strategy. In years where your income dips - perhaps you took a sabbatical, switched roles, or have a gap between companies - consider converting traditional IRA or 401(k) funds to Roth at a lower tax rate.

Fourth, state tax planning. If you're considering a move from a high-tax state (California, New York) to a no-income-tax state (Washington, Texas, Nevada), the timing of that move relative to your vesting dates matters enormously. GSU income is generally taxed in the state where you're resident when the shares vest.

Fifth, AMT awareness for ISOs. While Google primarily grants RSUs/GSUs, some employees - particularly those who joined through acquisitions - may hold ISOs from pre-acquisition grants. ISO exercises can trigger Alternative Minimum Tax (AMT), which requires separate planning.

Practical takeaway: Pull your most recent pay stub and your prior year's tax return side by side. Compare what was withheld on your GSUs versus your actual marginal rate. If there's a gap, you have time to course-correct for 2026.

When It Makes Sense to Work with an Advisor

Most Google employees are more than capable of understanding their own finances - that's rarely the issue. The issue is time and complexity.

When you have a single GSU grant on a straightforward vesting schedule, managing it yourself is totally reasonable. But there's a complexity threshold where the planning starts consuming real hours: maybe you have four overlapping vesting schedules, your household income crosses into AMT territory, you're evaluating a transfer to a different Alphabet entity, you want to optimize charitable giving alongside RSU sales, or you're simply tired of spending weekends on spreadsheets when you'd rather be doing literally anything else.

That's the point where having someone working alongside you starts saving more time and money than it costs. Not someone who tells you what to do - someone who runs the scenarios, lays out the trade-offs clearly, and lets you make the call with full confidence.

If you've hit that point where the decisions are real and the stakes feel high, Alphanso's advisors work alongside you to model the scenarios, explain the trade-offs, and help you move forward with clarity. You stay in the driver's seat - they handle the complexity. The flat fee is $2,400/year (no percentage of your assets, no requirement to transfer accounts), and you can start with a 14-day free trial to see if it's a good fit. No asset transfer, no commitment.

Frequently Asked Questions

How are Google RSUs (GSUs) taxed when they vest? GSUs are taxed as ordinary income at the fair market value on the vesting date. Google withholds federal taxes at the supplemental rate (22%, or 37% on amounts exceeding $1 million), plus applicable state taxes and FICA. The withholding often falls short of your actual tax liability if your marginal rate exceeds 22%, so planning for the gap is essential.

What is the Google RSU vesting schedule for new hires? Google's standard sign-on grant vests over four years with a front-loaded schedule: 33% in year one, 33% in year two, 22% in year three, and 12% in year four. Refresher grants typically vest evenly at 25% per year. Vesting frequency (monthly, quarterly, or semi-annually) depends on the number of shares in your grant.

Should I sell my Google stock as soon as it vests? There's no universal answer, but the key reframing is this: once your GSUs vest, holding them is a new investment decision. You're choosing to keep that money in Alphabet stock rather than diversifying. Most financial planners suggest keeping single-stock concentration below 10-15% of your total portfolio, but the right threshold depends on your overall financial picture, risk tolerance, and goals.

How much should Google employees contribute to their 401(k)? At minimum, contribute enough to capture Google's full employer match (up to $12,250 in 2026 with the 50% match on the full IRS limit). Ideally, max out the $24,500 employee contribution and explore the Mega Backdoor Roth strategy for additional tax-advantaged savings of $33,000+ per year.

What is the Mega Backdoor Roth, and does Google's plan support it? Yes, Google's 401(k) allows after-tax contributions with in-plan Roth conversions. This lets you contribute beyond the standard $24,500 limit (up to $70,000 total including employer contributions for those under 50) and convert those after-tax dollars to Roth, where they grow tax-free. It's one of the most powerful wealth-building tools available to high-income Google employees.

Do I need a financial advisor if I work at Google? Not necessarily - many Google employees manage their finances effectively on their own. An advisor becomes most valuable when the complexity compounds: multiple vesting schedules, cross-state tax considerations, large charitable giving plans, or simply not wanting to spend hours researching optimal strategies. The question is whether the time and money saved exceeds the cost of the advisor.

Can I keep my existing brokerage account if I work with Alphanso? Yes. Alphanso doesn't require you to transfer your assets. You keep your Schwab, Fidelity, or E-Trade accounts exactly where they are. Alphanso provides the planning, analysis, and recommendations - you maintain full control of your accounts and the final say on every decision.

Alphanso Wealth Management is a registered investment advisor. This article is for educational purposes and does not constitute personalized investment or tax advice. Talk to our advisory team for help in understanding these strategies or implementing them for your portfolio.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)