Financial Planning for Meta Employees: RSUs, Taxes & Wealth

Most Meta employees are building wealth faster than they realize. Many are also building it in a way that is more fragile than they realize - and the two facts are directly connected.

The Concentration Trap No One Warns You About

Here is a question worth sitting with: how much of your financial life is riding on Meta?

Your salary comes from Meta. Your bonus comes from Meta. Your RSUs - which vest quarterly and often represent 40-60% of your total comp - are Meta stock. For a senior engineer at L6 or above, it is entirely possible to have $500K-$1.5M in unvested equity sitting in a single ticker.

That is not a complaint. It is how Meta compensates top talent, and it is genuinely wealth-building. The problem is not the RSUs themselves - it is what happens when your career income and your investable net worth are both correlated to the same company's performance. If Meta has a bad year - a regulatory headwind, an ad revenue slowdown, a market rotation out of tech - you could face reduced refreshers and a falling portfolio at exactly the same moment. That is concentration risk in its most uncomfortable form.

This is the financial planning challenge specific to Meta employees, and the one most generic advisors are not equipped to address directly.

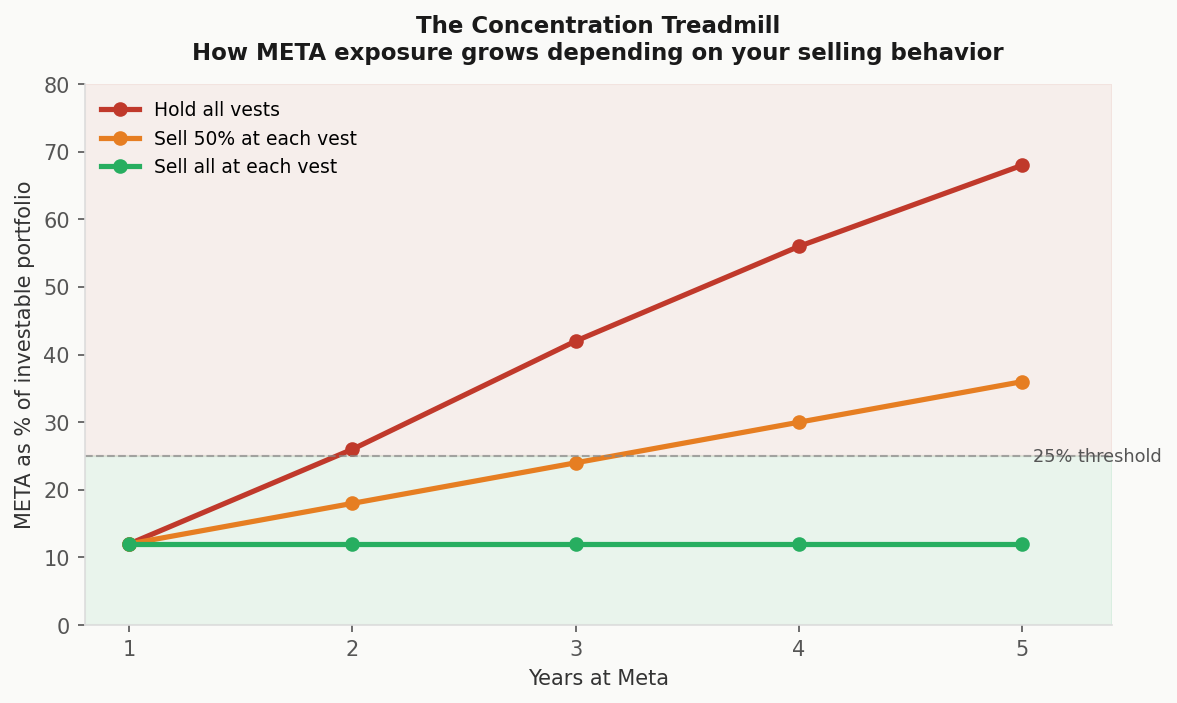

The Refresher Treadmill

Meta's refresher grant system rewards high performers with additional equity every year - but it creates a dynamic worth naming clearly: the longer you stay and the better you perform, the more concentrated you become.

An engineer who joined Meta in 2021 and has received above-target refreshers every year since could be sitting on three or four overlapping vesting schedules simultaneously. Each quarterly vest adds shares to a portfolio that is already heavily weighted toward META. If they have also been holding rather than selling - waiting for long-term capital gains treatment, or just not getting around to it - that concentration compounds year over year.

The treadmill feeling is real: you keep earning equity, but selling it feels like giving something up, and not selling it means your financial exposure to one company just keeps growing. Having a deliberate policy around how much Meta exposure you want in your portfolio - and sticking to it regardless of your conviction about the stock - is one of the highest-leverage financial decisions a Meta employee can make.

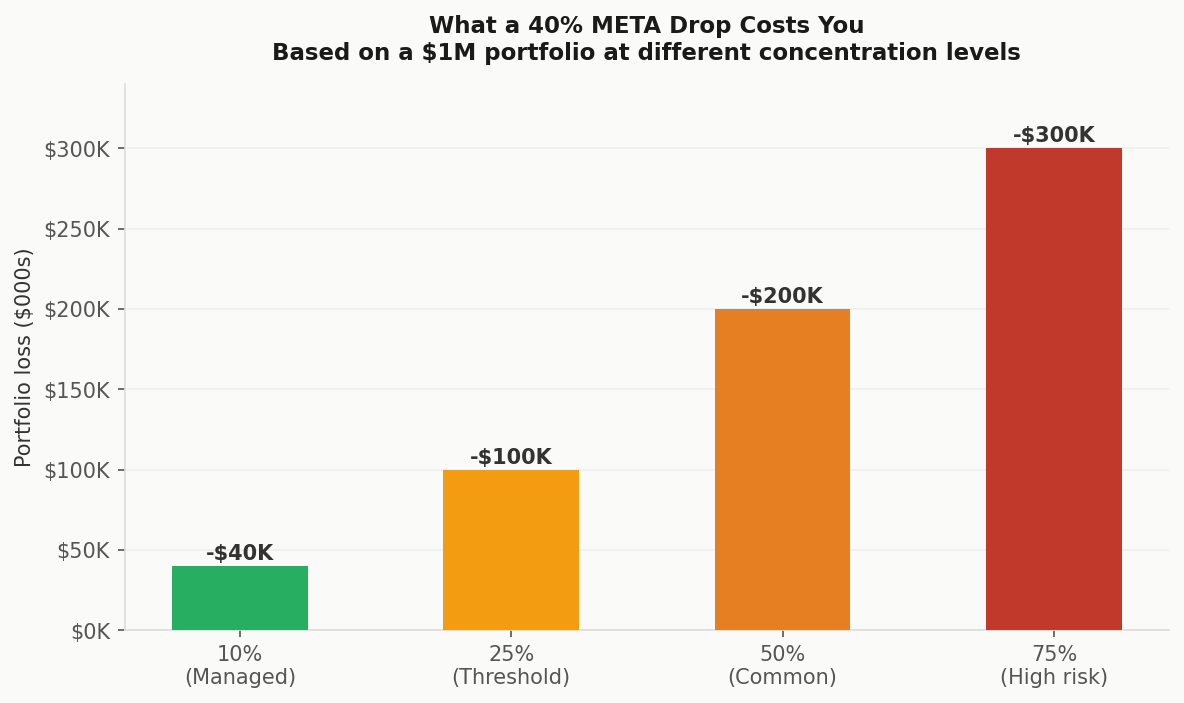

How Much Concentration Is Too Much?

There is no universal answer, but there is a useful mental model: if someone handed you a check equal to the current value of your Meta stock today, would you immediately invest 100% of it back into Meta? For most people, the answer is no - they would diversify. The question is why the math changes when the asset is labeled "my RSUs."

Most financial planners who work with tech employees suggest keeping any single stock at 15-25% of your total investable assets. Below that threshold, holding some Meta makes sense. Above it, you are taking on idiosyncratic risk that a diversified portfolio would eliminate without meaningfully reducing your expected returns.

For many senior Meta employees, getting to 15-25% META exposure requires selling aggressively at each vest for several years - not because the stock is bad, but because the math of diversification eventually wins over long time horizons.

The Question Every Meta Employee Eventually Faces: What If You Leave?

When you leave Meta - voluntarily, as part of a reorg, or after a long career - your salary stops, your unvested equity disappears, and what remains is whatever you have built outside the Meta ecosystem.

For many employees, that calculation is sobering. The salary was high but spending adjusted to match. The RSUs were large but most were held rather than systematically diversified. The result: a significant portion of net worth still in META stock, with no future income and no vesting events ahead.

The employees who navigate this best treated each vest as a scheduled opportunity to rebalance a financial plan being built in parallel to their Meta career, not instead of it.

A Practical Framework for Managing RSU Wealth

Rather than making ad hoc decisions at each vest, the clearest approach is a written policy set in advance. Three questions structure most of these decisions:

First, what is your target META exposure? Pick a percentage of your total portfolio and treat it as a ceiling. When vesting pushes you above it, sell to rebalance.

Second, what is your time horizon for each tranche? Selling immediately avoids stock-specific risk. Holding 12+ months gets long-term capital gains rates - but at the cost of concentration risk during the holding period.

Third, where are the proceeds going? Selling META and parking in cash is not a plan. Pair the selling policy with a target allocation: broad index funds, bonds, real estate, or whatever fits your timeline.

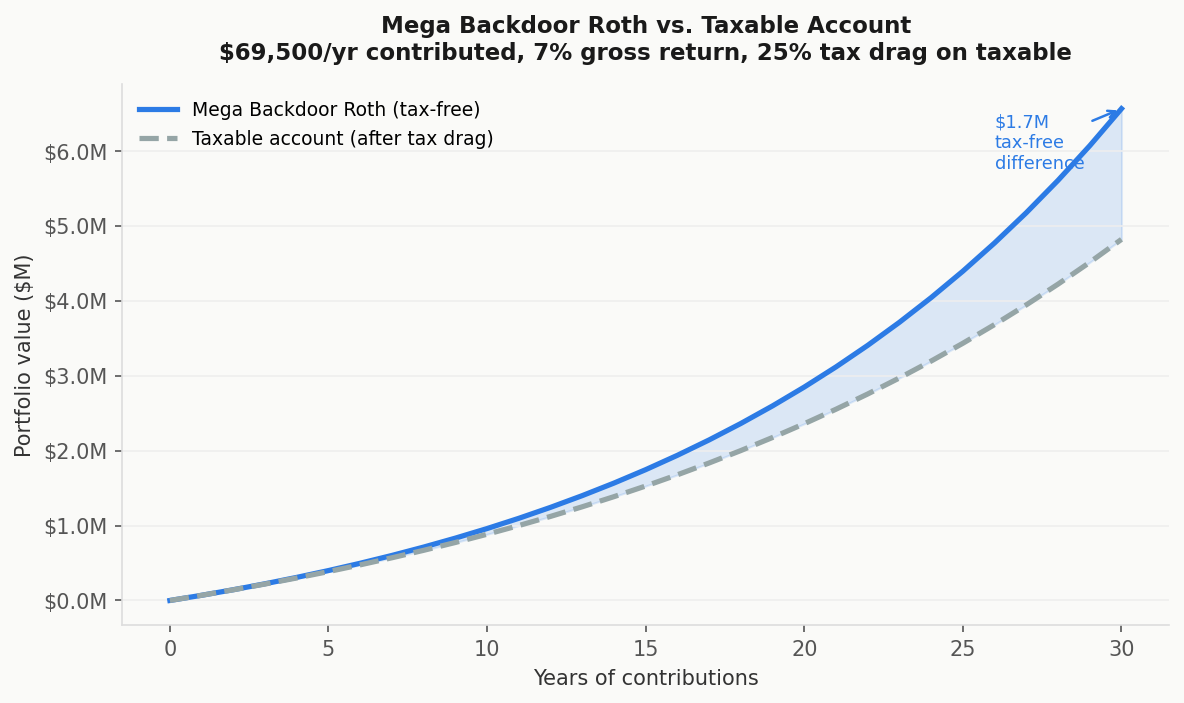

Building Wealth That Does Not Depend on META

The Mega Backdoor Roth is the most impactful starting point. After maxing the standard pre-tax 401(k) limit of $23,500 in 2026, Meta employees can contribute up to $46,000 more in after-tax dollars and convert to Roth - $69,500 per year compounding tax-free, completely uncorrelated to META.

An HSA adds another $4,300 (individual) or $8,550 (family) annually in triple-tax-advantaged savings. A taxable brokerage account funded systematically from RSU proceeds creates the kind of diversified wealth that makes a career transition survivable rather than devastating.

The common thread: these accounts need to be funded intentionally. The RSU income creates the capacity; the plan determines whether that becomes durable wealth or just a larger Meta position.

When It Makes Sense to Work with an Advisor

The mechanics of any one vest are not complicated. What gets genuinely complex is the interaction between multiple overlapping grants, tax-efficient selling strategies, reinvestment decisions, and long-term planning goals - especially when life events enter the picture.

If you are at the stage where the decisions feel real and the numbers are meaningful, Alphanso's advisors work alongside you on exactly this kind of planning. The flat fee is $2,400/year regardless of your portfolio size, no asset transfer required, and there is a 14-day free trial if you want to see how it works in practice.

Frequently Asked Questions

What is the best financial advisor for Meta employees?

Look for a fiduciary advisor who specializes in equity compensation and charges a flat fee. AUM-based fees mean your advisor earns more as your stock grows, even if the planning complexity stays the same.

How do Meta RSUs vest?

Quarterly on February 15, May 15, August 15, and November 15. Schedule A vests 1/16th per quarter over four years; Schedules B and C front-load or back-load distributions.

How much Meta stock should I hold?

Most planners suggest keeping any single employer stock below 15-25% of total investable assets. Above that level, one company's performance starts to dominate your long-term outcomes.

Should I hold Meta RSUs for long-term capital gains?

Holding 12+ months converts gains to long-term rates. Whether that tax savings justifies the concentration risk depends on your overall META exposure - if you are already heavily concentrated, the benefit rarely outweighs the risk.

What is the Mega Backdoor Roth and does Meta support it?

Yes. After the $23,500 pre-tax limit, contribute up to $46,000 more in after-tax dollars and convert to Roth - $69,500 total annually in tax-free growth.

What happens to my RSUs if I leave Meta?

Unvested RSUs are forfeited. Vested shares are yours. Systematic selling at vest improves your financial resilience if your plans change.

Do I need to move my brokerage account to work with Alphanso?

No. Keep your existing Fidelity, Schwab, or E-Trade account. Alphanso is planning-focused, not custody-focused.

Alphanso Wealth Management is a registered investment advisor. This article is for educational purposes and does not constitute personalized investment or tax advice.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)