Financial Planning for Amazon Employees: Master the 5-15-40-40

Most Amazon employees don't realize they have a six-figure tax problem until Year 3. That's when the back-loaded RSU vesting schedule kicks in — and suddenly 40% of your equity grant hits your W-2 in a single year. If you're not ready for it, the IRS will be.

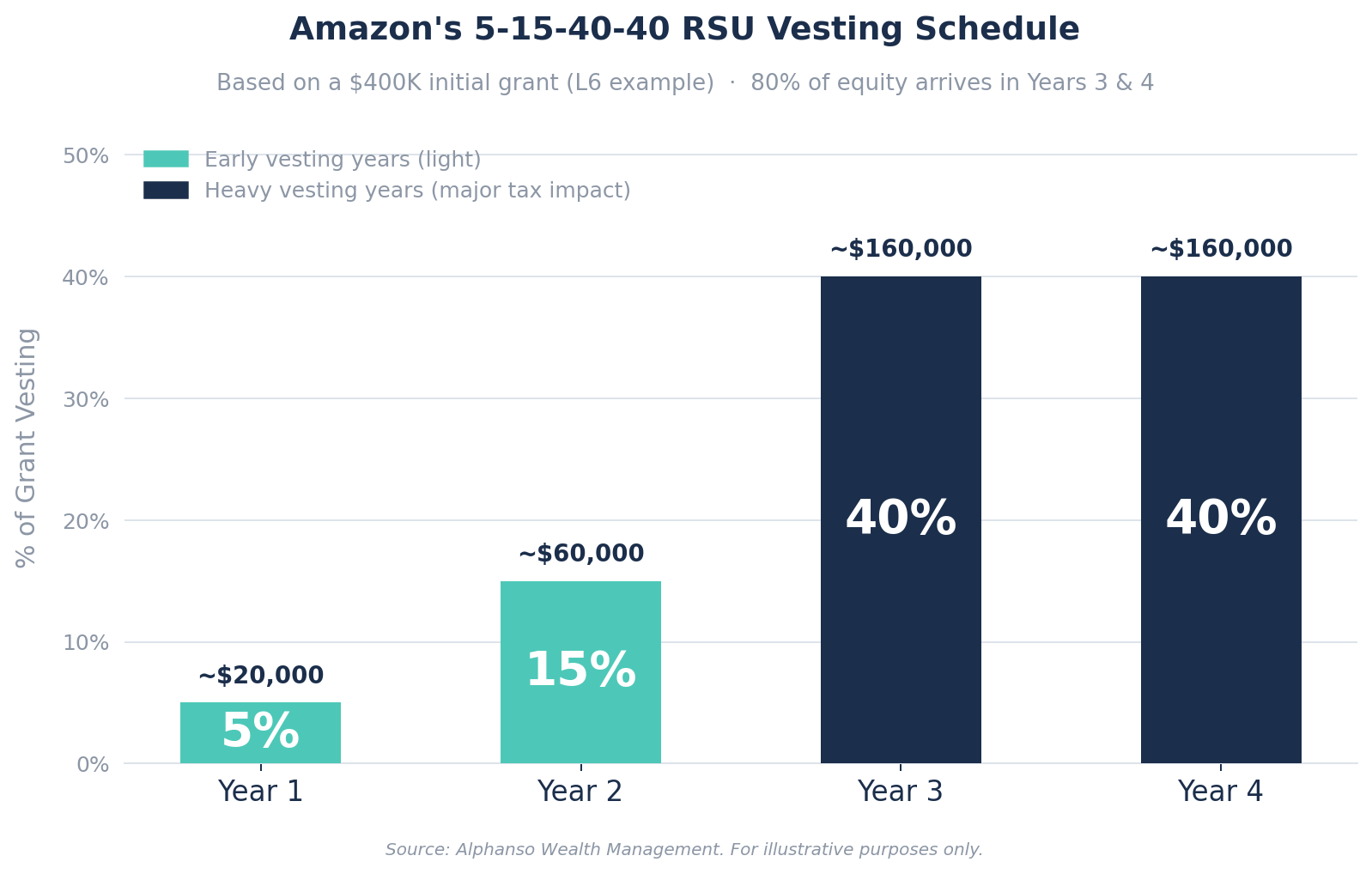

How Amazon's 5-15-40-40 RSU Vesting Schedule Actually Works

Amazon's RSU vesting schedule is unlike any other major tech company. Where Google, Meta, and Apple vest equity on a roughly even quarterly schedule, Amazon back-loads yours.

For an L6 engineer who receives a $400,000 RSU grant at hire, that means roughly $20,000 vests in Year 1, $60,000 in Year 2 — and then $160,000 hits in each of Years 3 and 4. At levels L4 through L7, vesting occurs quarterly in May, August, November, and February, which at least spreads the income across the tax year. But the dollar amounts in the back half still catch people off guard.

Why this matters for planning: Amazon compensates for the light early years with a signing bonus (typically paid in Years 1 and 2). So your total cash compensation stays relatively stable — but the composition shifts dramatically. In Year 1, your paycheck is mostly salary plus signing bonus. By Year 3, a huge portion is RSU income. That shift changes your tax picture entirely.

Practical takeaway: Map out your total compensation year by year, including signing bonus runoff and RSU vesting ramp-up. The transition from Year 2 to Year 3 is where most Amazon employees need a plan — and most don't have one.

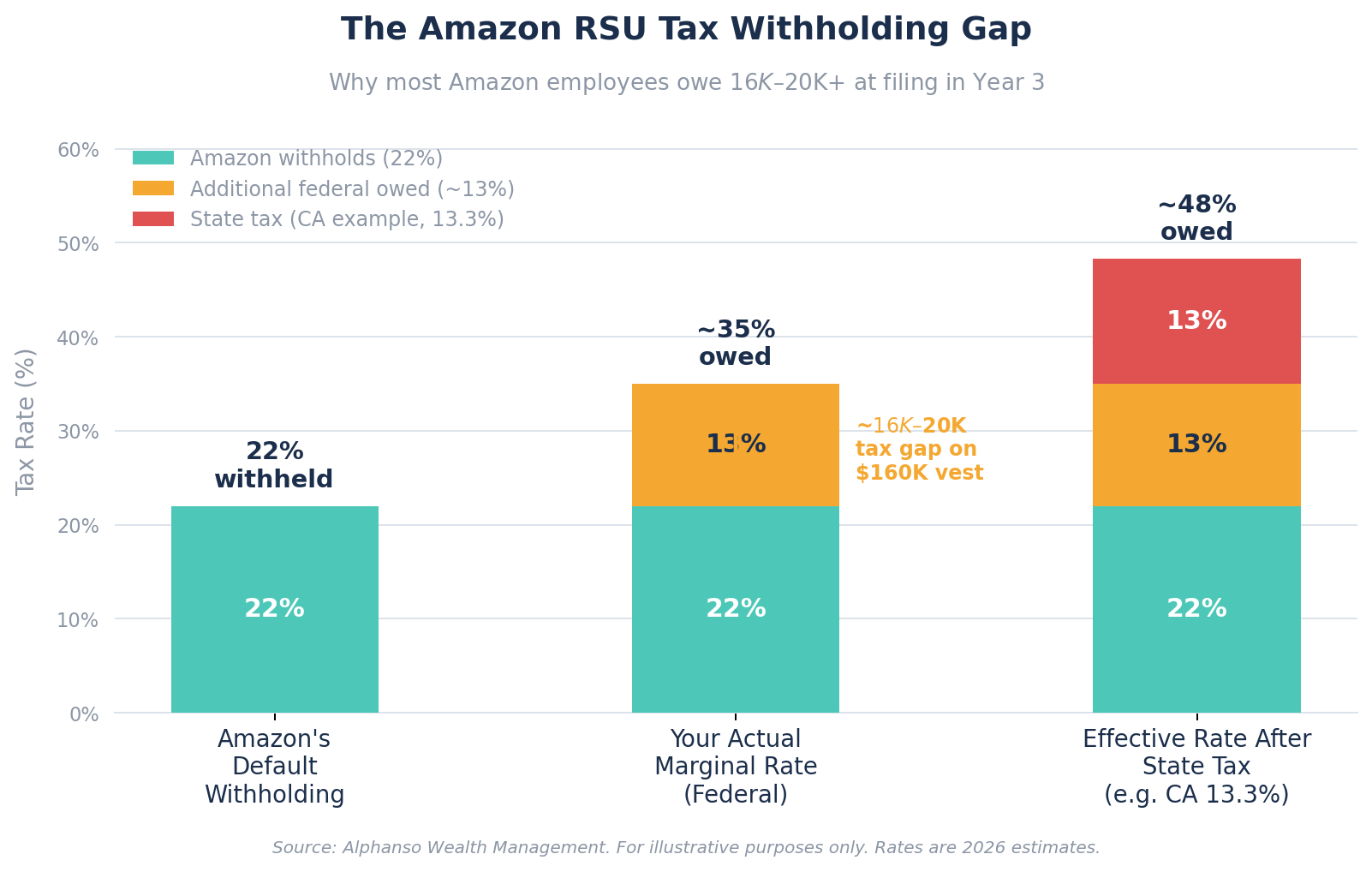

The Year 3 Tax Cliff: What $160,000 in RSU Income Does to Your Return

When $160,000 in RSU income lands on top of a $185,000+ base salary, the math gets uncomfortable fast. Here's what typically happens:

Federal taxes jump brackets. A married-filing-jointly Amazon employee earning $185,000 in base salary is already in the 24% federal bracket. Add $160,000 in RSU income and a meaningful portion of that new income gets taxed at 32% — and potentially 35%. That's before state taxes.

Default withholding falls short. Amazon withholds federal taxes on RSU vesting at a supplemental rate — typically 22%. But if your marginal rate is 32–35%, that 22% withholding leaves a gap of $16,000–$20,000 or more that you'll owe when you file. Many employees don't discover this until April of the following year.

NIIT may apply. If your modified adjusted gross income exceeds $250,000 (married filing jointly), the 3.8% Net Investment Income Tax kicks in on investment gains. With RSU income pushing you well past that threshold, capital gains from selling vested shares get an extra 3.8% surcharge.

Practical takeaway: Run a tax projection in Q1 of your Year 3. If your withholding is going to fall short — and it almost certainly will — set up quarterly estimated tax payments (Form 1040-ES) to avoid underpayment penalties. The penalty itself isn't devastating, but the surprise $18,000 bill in April is the kind of thing that derails financial plans.

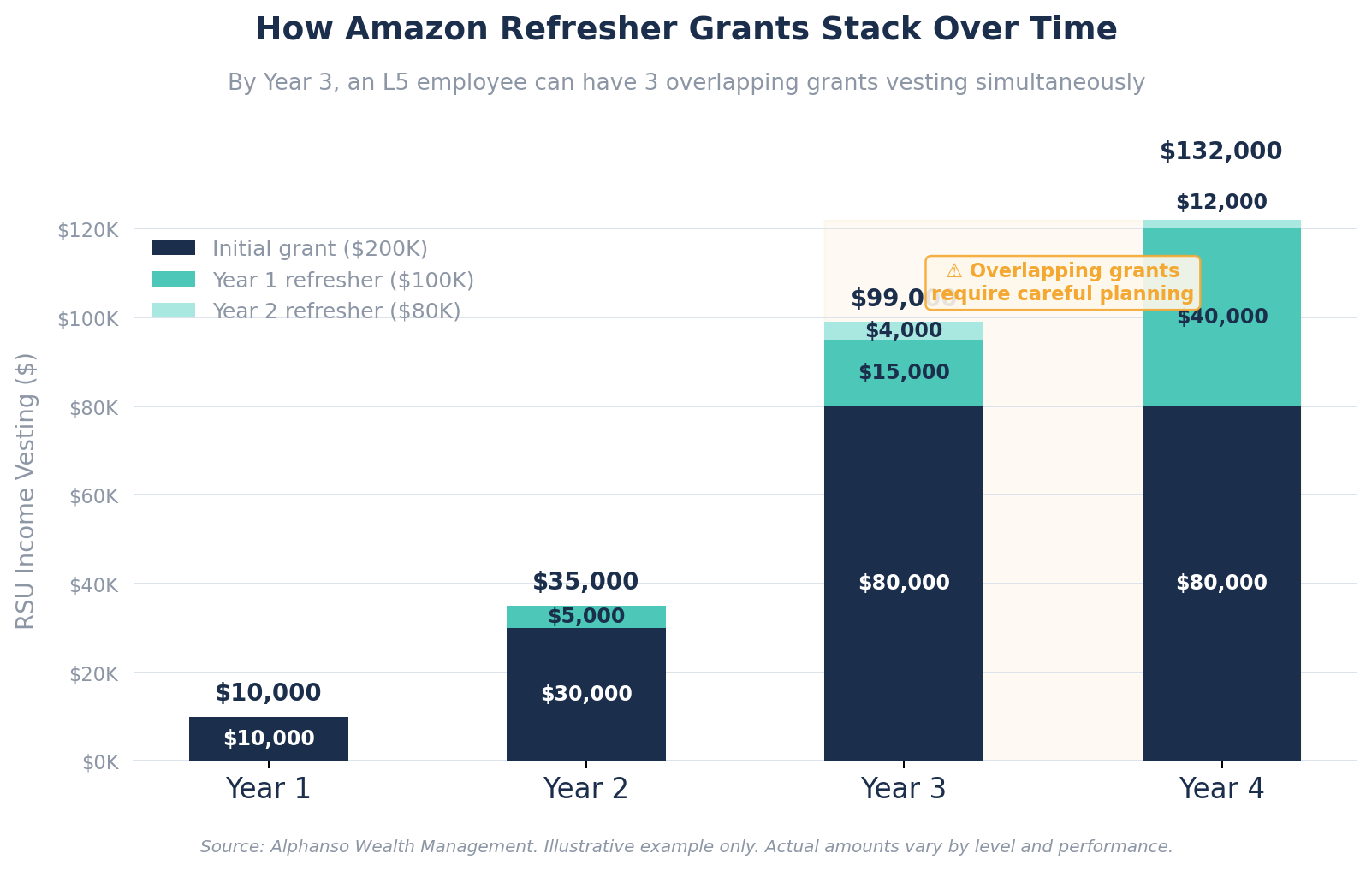

Refresher Grants Stack — And That's Where It Gets Interesting

Amazon issues refresher RSU grants annually based on performance, and they follow the same 5-15-40-40 vesting schedule. After your second year at Amazon, you'll have your original grant and your first refresher grant vesting simultaneously. By Year 4, you could have three overlapping grants.

This creates a compounding effect. An L5 who received a $200,000 initial grant and a $100,000 Year 1 refresher will have roughly $80,000 + $5,000 = $85,000 vesting in Year 3 from those two grants alone — plus any Year 2 refresher kicking in. The overlapping vesting schedules make income volatile and hard to predict without a spreadsheet (or an advisor who builds one for you).

Practical takeaway: Build a multi-year vesting calendar that layers all your grants. This is the single most useful planning tool for any Amazon employee, and it takes about 30 minutes to set up. Once you can see the full picture, you can plan tax strategies, diversification timing, and cash flow with actual numbers instead of guesses.

Five Tax-Smart Strategies for Amazon's Vesting Schedule

1. Max Out Tax-Deferred Accounts in High-Vesting Years

In 2026, you can contribute up to $23,500 to your 401(k) — and if you're over 50, an additional $7,500 in catch-up contributions. Every dollar you contribute reduces your taxable income dollar-for-dollar in the year it matters most. If you also have access to a Mega Backdoor Roth (Amazon's 401(k) plan allows after-tax contributions), you can shelter up to $70,000 total.

2. Use Charitable Giving Strategically with Donor-Advised Funds

If you're charitably inclined, donating appreciated Amazon shares to a Donor-Advised Fund (DAF) in a high-vesting year gives you a double benefit: a tax deduction at the full market value of the shares, and no capital gains tax on the appreciation. You can then distribute the funds to charities over multiple years. Bunching two or three years of charitable giving into one high-income year can push you above the standard deduction threshold and make itemizing worthwhile.

3. Evaluate the RSU-to-Cash Program

Amazon's RSU-to-cash pilot allows eligible employees (L4–L8 with at least 16 RSUs vesting) to convert 25% of vesting shares to cash at Amazon's preset planning price. This provides immediate liquidity and automatic diversification without you having to decide when to sell. The trade-off: you lock in a fixed price rather than the market price at vesting. Whether this makes sense depends on your view of Amazon's stock trajectory and your liquidity needs.

4. Consider Geographic Tax Planning Before Major Vesting Events

RSUs are taxed based on where you live when they vest, not when they were granted. If you're considering a move from a high-tax state (California at 13.3%, New York at 10.9%) to a no-income-tax state (Washington, Texas, Florida), timing that move before Year 3 vesting can save $15,000–$25,000 or more in state taxes on a single year's vesting. Amazon's largest offices are in Washington state — which has no income tax — so this is a real option for many employees.

5. Build a Systematic Diversification Plan

Holding concentrated positions in a single stock carries meaningful risk, regardless of how much you believe in Amazon's long-term trajectory. A common approach: set a rule (e.g., sell 50–75% of each RSU vest within 30 days) and invest the proceeds in a diversified portfolio. This isn't a bet against Amazon — it's an acknowledgment that your salary, bonuses, refresher grants, and career trajectory are already tied to the company. Your investment portfolio doesn't need to be, too.

When It Makes Sense to Work with an Advisor

For the first year or two at Amazon, the financial planning is relatively straightforward — you have a base salary, a signing bonus, and a small amount of RSU income. A spreadsheet and some smart Googling can get you pretty far.

The inflection point tends to come when you're approaching Year 3 vesting, you have multiple overlapping RSU grants, and you're trying to coordinate tax withholding, diversification timing, charitable giving strategy, and retirement contributions all at once. That's the point where the planning gets genuinely complex — not because any single piece is hard, but because the interactions between the pieces create trade-offs that are hard to see without modeling them.

If you've hit that point where the decisions are real and the stakes feel high, Alphanso's advisors work alongside you to model the scenarios, explain the trade-offs, and help you move forward with clarity. You stay in the driver's seat — they handle the complexity. The fee is $3,400/year — flat, regardless of your portfolio size — and there's no asset transfer required. Start a 14-day free trial; no commitment.

Frequently Asked Questions

How are Amazon RSUs taxed when they vest?

Amazon RSUs are taxed as ordinary income at the fair market value on the vesting date. The value is added to your W-2 income and taxed at your marginal federal and state income tax rates. Amazon withholds taxes at vesting, but the default supplemental withholding rate of 22% often falls short for employees in the 32–35% bracket, leaving a gap that results in a tax bill when you file.

Why does Amazon use a 5-15-40-40 vesting schedule instead of equal vesting?

Amazon's back-loaded vesting schedule is designed to incentivize long-term retention. By concentrating 80% of the equity grant in Years 3 and 4, Amazon encourages employees to stay through the most productive years of their tenure. The signing bonus in Years 1 and 2 compensates for the lighter equity vesting during that period.

Should I sell my Amazon RSUs as soon as they vest?

This depends on your overall financial situation, risk tolerance, and existing exposure to Amazon. Holding vested RSUs is economically identical to buying Amazon stock with cash — so the question is whether you'd buy Amazon stock today with that amount of money. Many financial planners suggest selling a significant portion at vesting and diversifying, particularly if your career income is already tied to Amazon's performance.

What is Amazon's RSU-to-cash pilot program?

Amazon's RSU-to-cash program allows eligible employees (L4–L8 with at least 16 RSUs vesting) to convert up to 25% of their vesting RSUs into cash at a preset planning price. The cash is paid quarterly. This provides automatic diversification and immediate liquidity, though you give up any upside above the preset price on those converted shares.

How much should I contribute to my 401(k) during high-vesting years?

In high-vesting years, maximizing your 401(k) contribution ($23,500 in 2026, plus $7,500 catch-up if over 50) is one of the most straightforward ways to reduce your taxable income. If your Amazon plan supports after-tax contributions with in-plan Roth conversions (Mega Backdoor Roth), you can shelter significantly more.

Do I need to make estimated tax payments on my Amazon RSU income?

If Amazon's default withholding doesn't cover your actual tax liability — which is common in Year 3 and beyond — you may need to make quarterly estimated payments to avoid underpayment penalties. Run a tax projection early in the year using your expected total compensation, including all RSU vesting events, to determine if a gap exists.

Alphanso Wealth Management is a registered investment advisor. This article is for educational purposes and does not constitute personalized investment or tax advice. Consult a qualified tax professional for advice specific to your situation.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)