Microsoft's First-Ever Voluntary Buyout: What 8,750 Employees Need to Know Before June 8

You just got a notification that could reshape your retirement. For the first time in 51 years, Microsoft is offering a voluntary buyout - and the decision window is narrower than you think.

What's Actually in the Microsoft Voluntary Retirement Package

The program targets employees whose age plus years of service equals 70 or more, at the senior director level (Level 67) and below. Employees on sales incentive plans are excluded. The deadline to accept is June 8, 2026, with a last day of July 1.

The offer has three components.

Cash severance scales by level and tenure. Level 64 and below receive one week of base pay for every six months of service. Levels 65 through 67 receive two weeks of base pay for every six months of service. Both tiers have a floor of 8 weeks and a ceiling of 39 weeks. For a Level 65 engineer with 15 years of tenure, that formula produces 60 weeks of base pay - though the 39-week cap brings the actual payout down to roughly 9 months of base salary.

Healthcare coverage continues for up to five years. The first year is subsidized by Microsoft at your existing coverage level. Years two through five, you pay a monthly premium but maintain access to Microsoft's medical, dental, vision, and wellbeing plans. Coverage may end sooner if you become eligible for Medicare.

RSU vesting continues after your departure date. Employees with fewer than 24 years of service receive six months of continued vesting. Employees with 24 or more years of service receive a full 12 months. Any unvested awards granted more than one year before your termination date will continue to vest on their normal schedule.

Microsoft's CFO has said the program will cost the company roughly $900 million. That number tells you something about the scale of what's being offered.

On paper, this looks generous. But the real financial complexity starts after you sign.

The 401(k) Rollover Trap Most Employees Don't See Coming

This is the single most expensive mistake eligible employees are at risk of making, and it's one that feels like responsible financial hygiene.

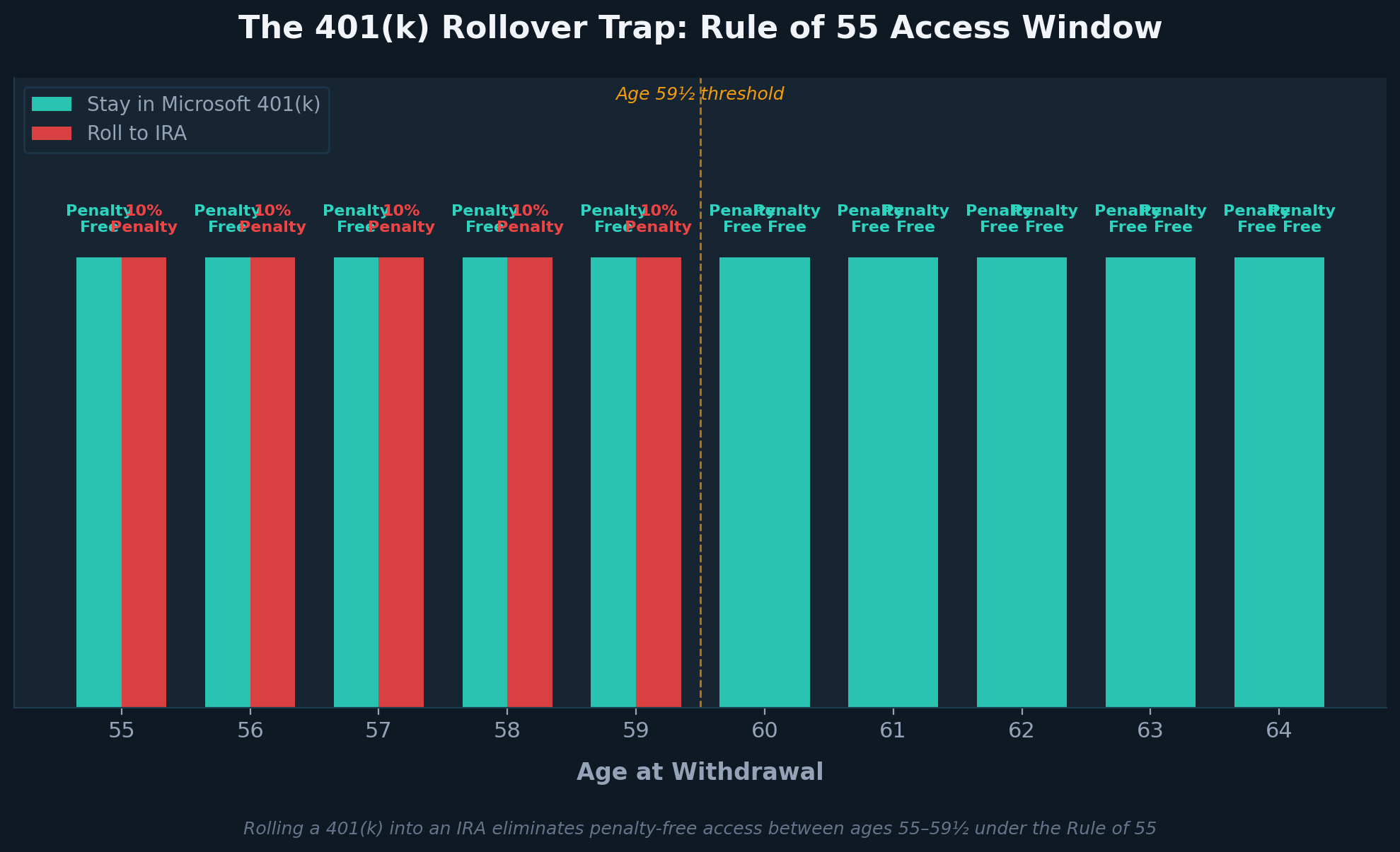

The IRS Rule of 55 allows penalty-free withdrawals from an employer-sponsored 401(k) if you separate from service during or after the calendar year you turn 55. Given that the Rule of 70 eligibility requirement means most eligible Microsoft employees are in their mid-50s to early 60s, a significant number qualify.

Here's where it goes wrong: the moment you roll that 401(k) balance into a traditional IRA, the Rule of 55 no longer applies. It evaporates. IRAs follow the standard age 59-1/2 rule, and every dollar withdrawn before that threshold gets hit with a 10% early withdrawal penalty on top of ordinary income tax.

Consider an employee who is 56 years old, separating from Microsoft with $1.2 million in their 401(k). If they leave the money in Microsoft's plan, they can take penalty-free distributions immediately to bridge the gap until Social Security and other income streams kick in. If they roll it into an IRA - which is what most financial content on the internet tells you to do - they lock themselves out of that access for three and a half years. A $200,000 withdrawal during that period would carry a $20,000 penalty that didn't need to exist.

The instinct to consolidate accounts after leaving an employer is strong, and it's often the right move. But when you're between 55 and 59-1/2, the order of operations matters enormously. You can always roll over later. You can't roll back.

One thing worth confirming before making any decisions: whether your plan allows partial withdrawals after separation, or whether it requires a full lump-sum distribution. Some plans restrict withdrawal frequency or impose administrative delays. That detail alone can change the entire strategy.

The RSU Withholding Gap Doesn't Pause for Buyouts

Continued RSU vesting is one of the most valuable parts of this package. It's also one of the most likely to create a tax surprise.

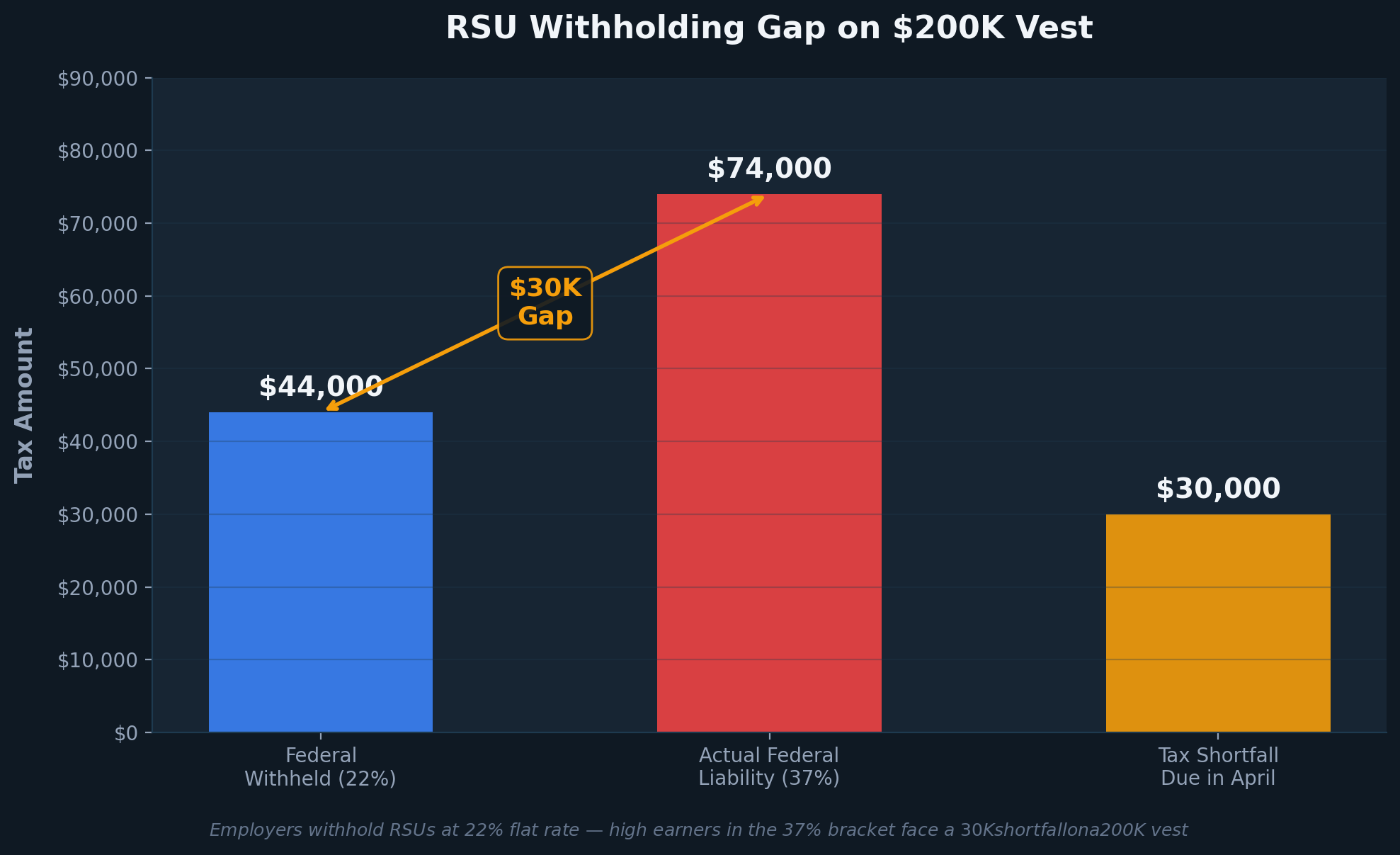

Here's the mechanic: when RSUs vest, employers withhold federal income tax at a flat 22% supplemental wage rate. That's the IRS default for supplemental income. But the employees eligible for this buyout - experienced, long-tenured, likely earning $200,000 or more in total compensation - are almost certainly in the 32% or 37% federal bracket.

That gap between withholding and actual tax liability is quiet all year. Then it shows up on your return.

On $200,000 of RSU vesting over a six-month post-separation window, the math looks like this:

- Federal tax withheld at 22%: $44,000

- Actual federal liability at 37%: $74,000

- Shortfall due in April: $30,000

Add state income tax (California alone adds up to 13.3%, and Washington state employees dodge this entirely), and the delta can widen further. For employees in high-tax states, the total underwithholding on a $200,000 vest can approach $40,000 to $50,000.

This isn't a planning failure. It's a structural mismatch built into how the IRS handles supplemental wages. But it means that the continued vesting benefit requires its own tax plan - specifically, adjusting estimated quarterly payments or pre-paying into the IRS before April 15 to avoid underpayment penalties.

The employees most exposed are the ones who assume their tax picture is settled because their employer is still handling withholding. The withholding is happening. It's just not happening at the right rate.

The Hidden Cost of Staying

Most of the conversation around this buyout focuses on whether the package is generous enough to leave. Less attention goes to the financial cost of staying.

For employees over 55 who are already close to their planned retirement date, every additional year inside Microsoft has trade-offs that don't show up in a comp review.

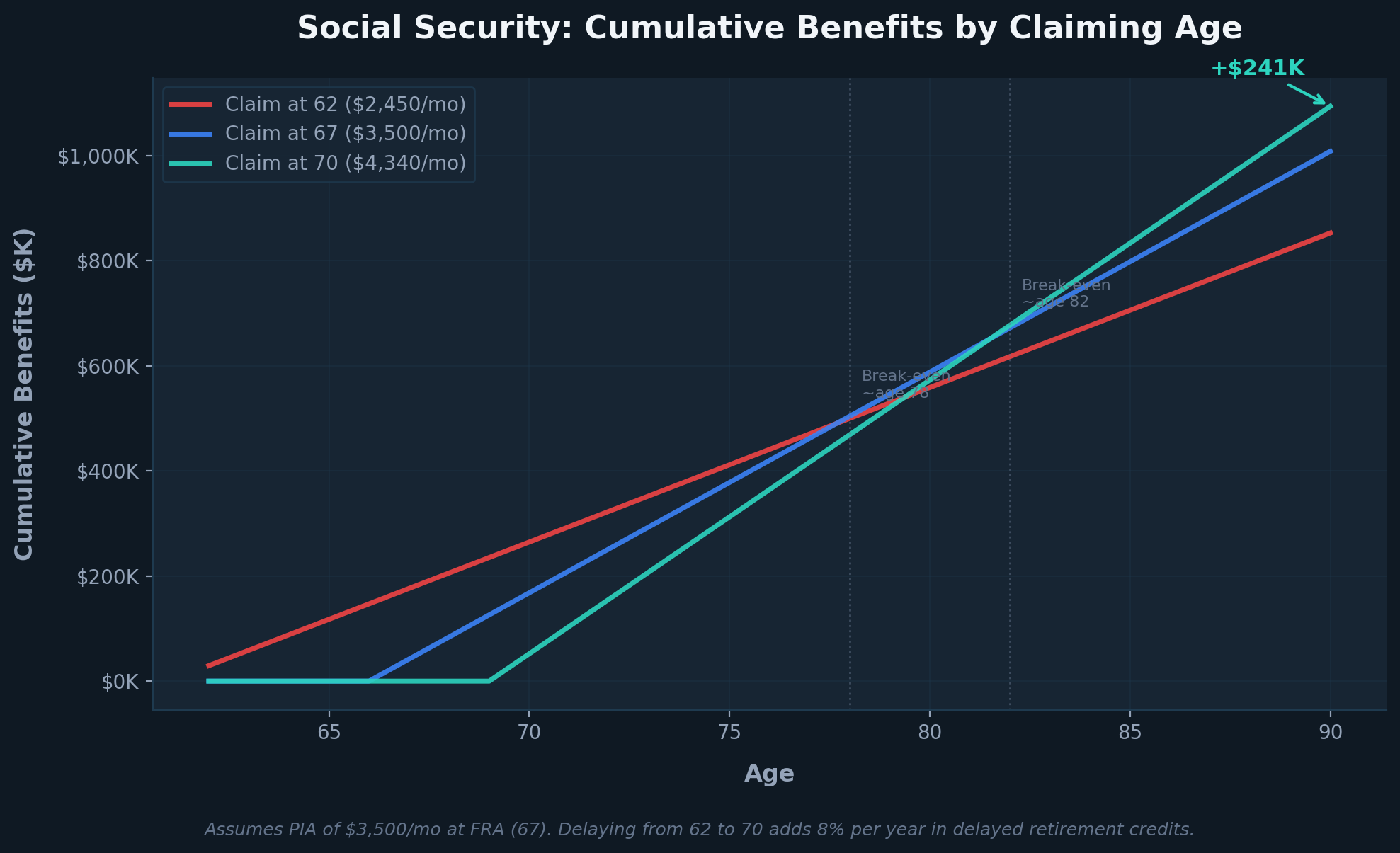

Social Security timing. Delayed retirement credits increase Social Security benefits by 8% per year between ages 62 and 70. An employee who takes the buyout at 56, uses 401(k) bridge distributions (penalty-free under Rule of 55), and delays claiming until 67 or 70 can mean tens of thousands of dollars in additional lifetime benefits.

Healthcare negotiated from a position of strength. The buyout offers five years of healthcare access. At 56, that bridges you to 61 - close to Medicare eligibility at 65, with ACA marketplace options to fill the remaining gap.

New RSU grants taxed at peak income. Every annual refresh grant you receive while employed vests as ordinary income at your current marginal rate. An employee in the 37% bracket who receives a $150,000 RSU refresh is keeping roughly $94,500 after federal tax. That same vesting event in a retirement year at the 22% bracket saves over $22,000 in tax on the same grant.

Three Moves to Make Before June 8

1. Map your 401(k) access window. If you're between 55 and 59-1/2, confirm whether Microsoft's plan allows partial post-separation withdrawals.

2. Run the RSU withholding math. Calculate the federal and state tax liability at your actual marginal rate - not the 22% supplemental rate.

3. Model the Social Security scenarios. Compare claiming early at 62, at full retirement age, and at 70. The difference can be $200,000 or more in cumulative lifetime benefits.

When It Makes Sense to Work with an Advisor

If you've hit that point where the decisions are real and the stakes feel high, Alphanso's advisors work alongside you to model the scenarios, explain the trade-offs, and help you move forward with clarity. You stay in the driver's seat - they handle the complexity. Start a 14-day free trial; no asset transfer, no commitment.

Frequently Asked Questions

What is Microsoft's Rule of 70 for the voluntary buyout?

If your age plus your years of service at Microsoft equals 70 or more, you qualify. The program is open to employees at Level 67 and below. Employees on sales incentive plans are excluded.

How much severance does Microsoft's buyout offer?

Level 64 and below receive one week of base pay per six months of service. Levels 65 to 67 receive two weeks per six months. Both tiers have a minimum of 8 weeks and a maximum of 39 weeks.

What happens to my Microsoft RSUs if I take the buyout?

Unvested awards granted more than one year before your termination date continue to vest for six months after departure. Employees with 24+ years of service receive 12 months of continued vesting.

Should I roll my Microsoft 401(k) into an IRA after the buyout?

If you're between 55 and 59-1/2, rolling into an IRA eliminates penalty-free withdrawals under the Rule of 55. Leaving the balance in Microsoft's plan preserves that access.

How does Microsoft's buyout healthcare coverage work?

One year of fully subsidized coverage, then up to four additional years at a monthly premium. Coverage may end earlier if you qualify for Medicare.

What is the deadline?

June 8, 2026. Last day of employment is July 1, 2026. Microsoft has stated it does not plan to offer another voluntary retirement program.

How does the buyout affect Social Security?

The buyout itself doesn't change your benefit calculation. However, it changes your claiming strategy options and may create an opportunity to delay claiming and earn 8% per year in delayed retirement credits.

Alphanso Wealth Management is a registered investment advisor. This article is for educational purposes and does not constitute personalized investment or tax advice.

Plan with an expert

What to expect

.png)

.jpg)

.png)

.png)